|

市場調査レポート

商品コード

1438446

ターボプロップ航空機:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Turboprop Aircraft - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ターボプロップ航空機:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 102 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

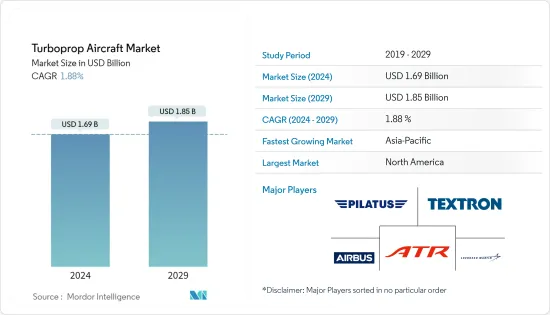

ターボプロップ航空機の市場規模は、2024年に16億9,000万米ドルと推定され、2029年までに18億5,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に1.88%のCAGRで成長します。

新型コロナウイルス感染症(COVID-19)のパンデミックはターボプロップ航空機市場に大きな影響を与え、2020年は商業および一般航空部門への納入が減少しました。しかし、商業および一般航空部門がパンデミックから回復したため、2021年の納入は増加しました。

ターボプロップ航空機は、短距離および低空飛行で非常に収益性が高くなります。この利点により、これらの航空機は地域の航空旅客輸送に対応するのに好まれており、新しい地域路線のイントロダクション伴い需要が高まっています。航空機事業者のこのような路線ネットワーク拡大計画は、今後数年間で市場の成長を推進すると予想されます。

軍事分野では、さまざまな軍隊が老朽化した輸送機や訓練機を新世代の航空機に置き換えることにより、航空機の近代化に投資しています。これにより、予測期間中に市場の成長が加速すると予想されます。

ターボプロップ航空機の市場動向

軍事部門が2021年に最高の市場シェアを獲得

2021年には軍事部門が主要な市場シェアを占めたが、これは主にA400MやC-130J航空機などの大型ターボプロップ航空機の納入によるものです。エアバス A400Mアトラスは、トランオールC-160やロッキード C-130ハーキュリーズのような欧州地域の古い輸送機を置き換えるためにエアバスによって開発された4発エンジンのターボプロップ輸送機です。 2021年には8機のA400M航空機が納入され、2013年以来合計105機が顧客に納入されました。また、各国の空軍はロッキード・マーティンC-130Jスーパーハーキュリーズやエアバスを発注し、輸送機の保有を拡大しています。 C295型機。輸送機に加えて、ターボプロップ機の一部のモデルも幅広い戦闘および非戦闘目的に配備されています。たとえば、2021年 9月にナイジェリア空軍(NAF)はA-29スーパートゥカーノ航空機を配備しました。この航空機は、2018年に12機のA-29スーパートゥカーノ航空機を調達する5億米ドル相当の注文の一環としてNAFに引き渡されました。この航空機は、飛行および戦闘訓練、近接航空支援作戦、反乱鎮圧、非正規戦、諜報・監視・偵察(ISR)を含む幅広い任務を支援することになります。軍隊による同様の調達プログラムにより、艦隊の近代化と航空能力の強化が市場の成長を促進すると予想されます。

2021年に北米が最高の市場シェアを記録

現在、北米が市場を独占しており、主に米国の商業、軍事、および一般航空分野におけるターボプロップ機の需要の高まりにより、予測期間中も市場の優位性が続くと予想されています。旅客輸送用に運航されているターボプロップ機は比較的少ないにもかかわらず、民間航空機の運航者は貨物輸送用に新しいターボプロップ機を導入しています。たとえば、エンパイア航空は2021年6月、フェデックスとのCMI契約に基づき、同社初の新造ATR72-600F航空機を導入したと発表しました。エンパイア航空は、米国におけるATR72-600F航空機のローンチカスタマーです。これに加えて、米国国防総省(DoD)は現在、航空機の近代化プログラムの一環として新しいC-130J航空機を取得しています。 2020年、ロッキード・マーティンは、最大50機のC-130Jスーパーハーキュリーを米国空軍(USAF)、米国海兵隊(USMC)、米国沿岸警備隊に納入する30億米ドルの複数年契約を獲得しました。国防総省は、21機のC-130Jの最初のトランシェに15億米ドルを付与しました。同社は合計で、24機のHC-130JとMC-130Jをアメリカ空軍に、20機のKC-130をアメリカ海兵隊に納入する契約を結んでいるが、米国沿岸警備隊には6機のHC-130Jを購入するオプションがあります。納入は2021年から2025年の間に行われる予定です。このような発展により、今後数年間で市場の成長が加速すると予想されます。

ターボプロップ航空機産業の概要

ターボプロップ航空機市場は細分化されており、いくつかのプレーヤーが大きな市場シェアを占めています。調査対象となっている市場の著名なプレーヤーには、ATR(エアバスとレオナルドの共同パートナーシップ)、エアバス SE、テキストロンアビエーション、ピラタスエアクラフト社、ロッキードマーチン社などがあります。 ATRは、COVID-19感染症のパンデミックにより最も大きな影響を受けた航空機OEM企業の1つです。 2020年の航空機納入と発注は、2019年の納入68機と発注79機に比べ、それぞれ10機と3機に減少しました。しかし、民間航空が回復し始めたため、2021年には航空機納入と発注はそれぞれ31機と35機に増加しました。新しい航空機モデルのイントロダクションは、航空機OEMの市場シェア拡大を支援すると予想されます。西安飛機工業公司は現在、双発の中距離ターボプロップ機「MA700」の開発に取り組んでいます。この航空機の座席定員は約70人で、2022年までに就航する予定です。中国航空工業総公司(AVIC)によると、この航空機は285機発注されています。新しい市場プレーヤーのイントロダクション、予測期間中に既存のOEM間の競合が激化する可能性があります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

- USDの通貨換算レート

第2章 調査手法

第3章 エグゼクティブサマリー

- 市場規模と予測、世界、2018~2027年

- 用途別の市場シェア、2021年

- 地域別市場シェア、2021年

- 市場の構造と主要参入企業

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- 業界の魅力- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション(金額別の市場規模と予測、2018~2027年)

- 用途

- 軍用航空

- 商用航空

- 一般航空

- 地域

- 北米

- 米国

- カナダ

- 欧州

- 英国

- フランス

- ドイツ

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- その他ラテンアメリカ

- 中東とアフリカ

- アラブ首長国連邦

- サウジアラビア

- エジプト

- その他の中東およびアフリカ

- 北米

第6章 競合情勢

- ベンダーの市場シェア

- 企業プロファイル

- Air Tractor

- Daher

- Piaggio Aerospace

- Pilatus

- Piper Aircraft Inc.

- Textron Aviation

- Thrush Aircraft LLC

- ATR

- Airbus SE

- Lockheed Martin Corporation

- Viking Air Ltd

- Northrop Grumman Corporation

- Embrear SA

第7章 市場機会と将来の動向

The Turboprop Aircraft Market size is estimated at USD 1.69 billion in 2024, and is expected to reach USD 1.85 billion by 2029, growing at a CAGR of 1.88% during the forecast period (2024-2029).

The COVID-19 pandemic significantly impacted the turboprop aircraft market, with deliveries for commercial and general aviation sectors decreasing in 2020. However, deliveries in 2021 increased as the commercial and general aviation sectors recovered from the pandemic.

Turboprop aircraft are highly profitable for short-distance and low altitude flying. Due to this advantage, these aircraft are preferred to cater to regional air passenger traffic, and their demand is growing with the introduction of new regional routes. Such route network expansion plans of aircraft operators are expected to propel the market's growth over the coming years.

In the military sector, various armed forces are investing in fleet modernization by replacing their aging transport and training aircraft fleet with new generation aircraft. This is anticipated to accelerate the market's growth during the forecast period.

Turboprop Aircraft Market Trends

Military Segment Held the Highest Market Share in 2021

The military segment accounted for a major market share in 2021, primarily due to the deliveries of large turboprop aircraft like A400M and C-130J aircraft. Airbus A400M Atlas is a four-engine turboprop transport aircraft developed by Airbus to replace older transport aircraft in the European region, like the Transall C-160 and the Lockheed C-130 Hercules. In 2021, eight A400M aircraft were delivered, and a total of 105 aircraft have been delivered to customers since 2013. Also, various countries' air forces have been expanding their fleet of transport aircraft with orders for Lockheed Martin C-130J Super Hercules and Airbus C295 aircraft. In addition to the transport aircraft, some models of turboprop aircraft are also deployed for a wide range of combat and non-combat purposes. For instance, in September 2021, the Nigerian Air Force (NAF) inducted the A-29 Super Tucano aircraft into service. The aircraft was delivered to NAF as part of an order placed in 2018 worth USD 500 million for the procurement of 12 A-29 Super Tucano aircraft. The aircraft will support a wide range of missions, including flight and combat training, close air support operations, counterinsurgency, irregular warfare, and intelligence, surveillance, and reconnaissance (ISR). Similar procurement programs by the armed forces to modernize their fleet and enhance their aerial capabilities are anticipated to propel the market's growth.

North America Recorded the Highest Market Share in 2021

North America currently dominates the market and is expected to continue its market dominance over the forecast period primarily due to the growing demand for turboprop fleets in the United States for the commercial, military, and general aviation sectors. Despite the relatively fewer turboprop aircraft in service for passenger transport, commercial aircraft operators are acquiring new turboprop aircraft for cargo transportation. For instance, Empire Airlines, in June 2021, announced that the airline had taken its first new-build ATR72-600F aircraft under a CMI agreement with FedEx. Empire Airlines is the launch customer of ATR72-600F aircraft in the United States. In addition to this, the US Department of Defense (DoD) is currently acquiring new C-130J aircraft as a part of its fleet modernization program. In 2020, Lockheed Martin won a USD 3 billion multiyear contract to deliver up to 50 C-130J Super Hercules to the US Air Force (USAF), US Marine Corps (USMC), and US Coast Guard. The DoD awarded USD 1.5 billion for the first tranche of 21 C-130Js. In total, the company is contracted to deliver a mix of 24 HC-130Js and MC-130Js to the USAF, and 20 KC-130s to the USMC, while the US Coast Guard has an option to buy six HC-130Js. The deliveries will take place between 2021 and 2025. Such developments are anticipated to accelerate the market's growth over the coming years.

Turboprop Aircraft Industry Overview

The turboprop aircraft market is fragmented, with several players accounting for a significant market share. Some of the prominent players in the market studied are ATR (a joint partnership between Airbus and Leonardo), Airbus SE, Textron Aviation, Pilatus Aircraft Ltd, and Lockheed Martin Corporation. ATR was one of the most affected aircraft OEMs due to the COVID-19 pandemic. In 2020, its aircraft deliveries and orders decreased to 10 and three, respectively, compared to 68 aircraft deliveries and 79 orders in 2019. However, as commercial aviation began recovering, aircraft deliveries and orders increased to 31 and 35, respectively, in 2021. The introduction of a new aircraft model is expected to support aircraft OEMs in increasing their share in the market. Xi'an Aircraft Industry Corporation is currently working on developing the MA700, a twin-engine medium-range turboprop aircraft. The aircraft has a seating capacity of about 70 passengers and is expected to enter service by 2022. According to the Aviation Industry Corporation of China (AVIC), the aircraft has 285 aircraft orders. The introduction of new market players may increase the competition among the existing OEMs during the forecast period.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

- 1.3 Currency Conversion Rates for USD

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

- 3.1 Market Size and Forecast, Global, 2018-2027

- 3.2 Market Share by Application, 2021

- 3.3 Market Share by Geography, 2021

- 3.4 Structure of the Market and Key Participants

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size and Forecast by Value - USD million, 2018-2027)

- 5.1 Application

- 5.1.1 Military Aviation

- 5.1.2 Commercial Aviation

- 5.1.3 General Aviation

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.2 Europe

- 5.2.2.1 United Kingdom

- 5.2.2.2 France

- 5.2.2.3 Germany

- 5.2.2.4 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Japan

- 5.2.3.4 South Korea

- 5.2.3.5 Rest of Asia-Pacific

- 5.2.4 Latin America

- 5.2.4.1 Brazil

- 5.2.4.2 Rest of Latin America

- 5.2.5 Middle-East and Africa

- 5.2.5.1 United Arab Emirates

- 5.2.5.2 Saudi Arabia

- 5.2.5.3 Egypt

- 5.2.5.4 Rest of Middle-East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Air Tractor

- 6.2.2 Daher

- 6.2.3 Piaggio Aerospace

- 6.2.4 Pilatus

- 6.2.5 Piper Aircraft Inc.

- 6.2.6 Textron Aviation

- 6.2.7 Thrush Aircraft LLC

- 6.2.8 ATR

- 6.2.9 Airbus SE

- 6.2.10 Lockheed Martin Corporation

- 6.2.11 Viking Air Ltd

- 6.2.12 Northrop Grumman Corporation

- 6.2.13 Embrear SA