|

市場調査レポート

商品コード

1445419

バイオベースポリマー: 市場シェア分析、業界動向と統計、成長予測(2024~2029年)Bio-based Polymers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| バイオベースポリマー: 市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

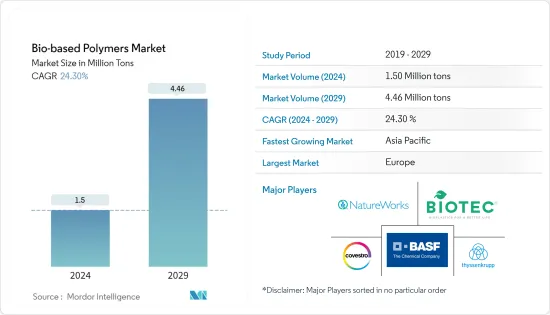

バイオベースポリマー市場規模は、2024年に150万トンと推定され、2029年までに446万トンに達すると予測されており、予測期間(2024年から2029年)中に24.30%のCAGRで成長します。

COVID-19は、バイオベースポリマー市場の成長に影響を与えました。しかし、パンデミック中およびパンデミック後の包装食品とオンライン食品配達の需要の増加により、包装コーティングの消費が促進され、その結果、バイオベースポリマーの消費が発生しました。

短期的には、持続可能なプラスチックに対する需要の増加が、市場の需要を牽引する主要な要因の1つです。

その一方で、バイオプラスチックの性能の問題と、石油ベースのポリマーと比較してバイオベースのポリマーに関連する価格の高さが、調査対象の市場の成長を妨げると予想されます。

生分解性プラスチックの用途の増加は、将来的にチャンスとなる可能性があります。

さらに、包装業界は市場を独占しており、予測期間中に成長すると予想されます。

欧州は世界中の市場を独占しており、最大の消費国はフランスや英国などです。

バイオベースポリマー市場動向

包装業界からの需要の増加

- 包装は、バイオベースポリマーの最大の市場の1つです。これらのポリマーは、優れた透明性と光沢、食品油脂に対する耐性、および芳香バリアを示します。さらに、パッケージに剛性、ねじれ保持力、印刷適性も与えます。

- バイオベースのポリマーは主に、スーパーマーケットの果物や野菜の包装、パンの袋やベーカリーの箱、ボトル、封筒、陳列用のカートンの窓、ショッピングバッグやキャリーバッグなどに使用されています。たとえば、インド商務省によると、2022年度のインドからの生鮮野菜の輸出額は約8億200万米ドルに達しました。加工野菜の場合、同年の輸出額は約4億2,500万米ドルに達しました。これは、2020年と比較して、生鮮野菜部門で10.87%、加工野菜で0.21%の増加を示しています。したがって、生鮮野菜と加工野菜の輸出増加により、国内でのバイオベースポリマーの需要が創出されると予想されます。

- 包装用バイオベースポリマー市場は、欧州および北米地域で急速に成長しています。食品の安全性に関するFDAおよび関連機関の介入の増加により、飲料およびスナックの消費における生分解性および食品グレードのプラスチックの使用が主に促進されています。

- レストランチェーンや食品加工業界では、食品包装に生分解性素材を採用するケースが増えています。一部のプラスチックには発がん性があることが証明されているため、特に新興国では食品の安全性に対する消費者の意識も急速に高まっています。

- アジア太平洋、南米、中東の発展途上地域の成長は、さまざまな食品安全機関の食品包装基準の向上により、近い将来さらに増加すると予想されています。

- さらに、生分解性ポリマーは廃棄が容易であるため、包装業界からの需要がさらに高まっています。

欧州地域が市場を独占

- 欧州はバイオベースポリマーの最大のシェアを保持し、世界市場を独占しています。

- この地域における国民の意識と政府の取り組みにより、特にキャリーバッグ、食品包装、食品サービス(カトラリーなど)、有機廃棄物キャディライナーなどでの生分解性ポリマーの使用が支持されてきました。

- この地域のさまざまな国は、より環境に優しい包装の提供に注力しています。これにより、包装分野におけるポリ乳酸の需要が増加しました。

- 英国は欧州の主要国の一つであり、バイオベースポリマー包装材の需要が高まっています。包装製品の持続可能性要素に対する意識の高まりと、最近の政府の取り組みにより、調査対象となっている国内の市場の成長に好ましい市場シナリオが生まれています。

- 使い捨てプラスチックの禁止は、バイオベースポリマー包装製品の需要に直接影響を与える主な要因の一つです。例えば、英国政府は2021年、プラスチック汚染対策として英国国内で使い捨てプラスチック製のカトラリー、皿、ポリスチレンカップを禁止する計画を発表しました。

- パッケージング業界で活動する新興企業だけでなく、既存のベンダー数社も、国内でのバイオベースポリマーパッケージングの推進に率先して取り組んでいます。たとえば、2022年 6月、英国に本拠を置く企業マジカルマッシュルームカンパニーは、植物ベースの持続可能なパッケージングのために340万ユーロ(331万米ドル)の資金を確保しました。

- 現在、英国の包装部門の年間売上高は110億ポンドで、従業員数は85,000人を超えています。

- 欧州連合(EU)は、2050年の実質ゼロ排出目標に向けて取り組み、欧州グリーンディールを実施することで増大する環境と持続可能性の危機に取り組んでいます。より持続可能な社会への傾向は、欧州経済のプラスチックの生産、使用、廃棄と絡み合っています。

- 小型包装のニーズの高まりとライフスタイルの変化に伴う消費習慣の拡大により、予測期間中にバイオベースポリマーの需要が高まると予想されます。

バイオベースポリマー業界の概要

バイオベースポリマー市場は本質的に部分的に統合されています。市場の主要企業には(順不同)、BASF SE、Covestro AG、BIOTEC Biologische Naturverpackungen GmbH &Co. KG.、thyssenkrupp AG、NatureWorks LLCなどが含まれます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 環境保全のために環境に優しいポリマーを選択

- 多くの国における非分解性ポリマーに関する規制

- 先進国と発展途上国における消費者の意識の向上

- 生分解性ポリマーの非毒性の性質

- 抑制要因

- 石油ベースのポリマーと比較して価格が高い

- 低所得国における意識の低さ

- 業界のバリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替製品やサービスの脅威

- 競合の程度

第5章 市場セグメンテーション

- タイプ

- でんぷん系プラスチック

- ポリ乳酸(PLA)

- ポリヒドロキシアルカノエート(PHA)

- ポリエステル(PBS、PBAT、PCL)

- セルロース誘導体

- 用途

- 農業

- 繊維

- エレクトロニクス

- 包装

- ヘルスケア

- その他の用途

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- その他欧州

- 世界のその他の地域

- ブラジル

- サウジアラビア

- 世界のその他の地域

- アジア太平洋

第6章 競合情勢

- 合併と買収、合弁事業、コラボレーション、および契約

- 市場シェア(%)**/ランキング分析

- 有力企業が採用した戦略

- 企業プロファイル

- BASF SE

- Biologische Naturverpackungen GmbH &Co. KG.

- Cardia Bioplastics

- Covestro AG

- Corbion

- Cortec Group Management Services, LLC

- DuPont de Nemours, Inc.

- FKuR

- FP International

- Innovia Films

- Merck KGaA

- YIELD10 BIOSCIENCE, INC.(Metabolix Inc.)

- NatureWorks LLC

- Novamont SpA

- Rodenburg Biopolymers

- SHOWA DENKO KK

- thyssenkrupp AG

第7章 市場機会と将来の動向

- 生分解性プラスチックの用途拡大

- ドラッグデリバリーにおける調査の増加

- 新興国における規制強化

The Bio-based Polymers Market size is estimated at 1.5 Million tons in 2024, and is expected to reach 4.46 Million tons by 2029, growing at a CAGR of 24.30% during the forecast period (2024-2029).

COVID-19 impacted the bio-based polymer market's growth. However, the increased demand for packaged food and online food deliveries during the pandemic and post-pandemic propelled the consumption of packaging coatings, which resulted in the consumption of bio-based polymers.

Over the short term, increasing demand for sustainable plastics is one of the major factors driving market demand.

On the flip side, the performance issue with bioplastics and the high prices associated with bio-based polymers compared to petroleum-based polymers are expected to hinder the growth of the market studied.

The increasing applications of biodegradable plastics are likely to present an opportunity in the future.

Moreover, the packaging industry dominates the market and is expected to grow during the forecast period.

Europe dominated the market across the world, with the largest consumption coming from countries such as France and the United Kingdom.

Bio-based Polymers Market Trends

Increasing Demand from Packaging Industry

- Packaging is one of the largest markets for bio-based polymers. These polymers exhibit excellent clarity and gloss, resistance to food fats and oils, and an aroma barrier. Additionally, they also provide stiffness, twist retention, and printability to the packaging.

- Bio-based polymers are mostly used in fruit and vegetable packaging in supermarkets, for bread bags and bakery boxes, bottles, envelopes, display carton windows, and shopping or carrier bags, among others. For instance, according to the Department of Commerce (India), the export value of fresh vegetables from India amounted to about USD 802 million in the fiscal year 2022. For processed vegetables, the value stood at nearly USD 425 million in the same year, which shows an increase of 10.87% from the fresh vegetable segment and 0.21% from processed vegetables compared with 2020. Therefore, an increase in the exports of fresh and processed vegetables is expected to create demand for bio-based polymers in the country.

- The bio-based polymer market for packaging is growing rapidly in the European and North American regions. The increasing intervention of the FDA and related organizations in terms of food safety is largely promoting the usage of biodegradable and food-grade plastics for beverage and snack consumption.

- The restaurant chains and food processing industries are increasingly adapting biodegradable materials for food packaging. Consumer awareness is also rising rapidly, especially in emerging economies, in terms of food safety, as some plastics are proven carcinogenic.

- The growth in developing regions, like Asia-Pacific, South America, and the Middle East, is expected to increase in the near future due to the improving food packaging standards of various food and safety organizations.

- Moreover, the higher ease of disposing of biodegradable polymers has further added to their growing demand from the packaging industry.

Europe Region to Dominate the Market

- Europe holds the largest share of bio-based polymers and dominates the global market.

- Public awareness and government initiatives in the region have supported the use of biodegradable polymers in carrier bags, food packaging, food services (cutlery, etc.), and organic waste caddy liners, among others.

- Various countries in the region have been focusing on offering more eco-friendly packaging. This has increased the demand for polylactic acid in the packaging sector.

- The United Kingdom (UK) is among the leading countries in Europe, where the demand for bio-based polymer packaging has been increasing. The higher awareness about the sustainability factors of packaging products, along with recent government initiatives, are creating a favorable market scenario for the growth of the studied market in the country.

- The ban on single-use plastics is among the primary factors that will directly impact the demand for bio-based polymer packaging products. For instance, in 2021, the UK government announced plans to ban single-use plastic cutlery, plates, and polystyrene cups in England to tackle plastic pollution.

- Several existing vendors, as well as startups operating in the packaging industry, are also taking the initiative to promote bio-based polymer packaging in the country. For instance, in June 2022, Magical Mushroom Company, a UK-based company, secured funding of EUR 3.4 million (USD 3.31 million) for its plant-based sustainable packaging.

- Currently, the packaging sector in the United Kingdom has annual sales of GBP 11 billion, and it employs more than 85,000 people.

- The European Union (EU) is working towards the 2050 net-zero emissions goal and tackling the increasing environmental and sustainability crises by implementing the European Green Deal. The inclination towards a more sustainable society is intertwined with the European economy's production, use, and disposal of plastic.

- The growing need for small-size packaging and the growing consumption habits associated with the change in lifestyles are anticipated to propel the demand for bio-based polymers over the forecast period.

Bio-based Polymers Industry Overview

The bio-based polymer market is partially consolidated by nature. Some of the major players in the market (not in any particular order) include BASF SE, Covestro AG, BIOTEC Biologische Naturverpackungen GmbH & Co. KG., thyssenkrupp AG, and NatureWorks LLC, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Preference toward Eco-friendly Polymers to Preserve Environment

- 4.1.2 Regulation on Non-degradable Polymers in Many Countries

- 4.1.3 Increasing Consumer Awareness in Developed and Developing Nations

- 4.1.4 Non-toxic Nature of Biodegradable Polymers

- 4.2 Restraints

- 4.2.1 Higher Price Compared to Petroleum-based polymers

- 4.2.2 Low Awareness in Low Income Countries

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Starch-based Plastics

- 5.1.2 Poly Lactic Acid (PLA)

- 5.1.3 PolyHydroxy Alkanoates (PHA)

- 5.1.4 Polyesters (PBS, PBAT, and PCL)

- 5.1.5 Cellulose Derivatives

- 5.2 Application

- 5.2.1 Agriculture

- 5.2.2 Textile

- 5.2.3 Electronics

- 5.2.4 Packaging

- 5.2.5 Healthcare

- 5.2.6 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 Rest of World

- 5.3.4.1 Brazil

- 5.3.4.2 Saudi Arabia

- 5.3.4.3 Rest of the World

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 BASF SE

- 6.4.2 Biologische Naturverpackungen GmbH & Co. KG.

- 6.4.3 Cardia Bioplastics

- 6.4.4 Covestro AG

- 6.4.5 Corbion

- 6.4.6 Cortec Group Management Services, LLC

- 6.4.7 DuPont de Nemours, Inc.

- 6.4.8 FKuR

- 6.4.9 FP International

- 6.4.10 Innovia Films

- 6.4.11 Merck KGaA

- 6.4.12 YIELD10 BIOSCIENCE, INC. (Metabolix Inc.)

- 6.4.13 NatureWorks LLC

- 6.4.14 Novamont SpA

- 6.4.15 Rodenburg Biopolymers

- 6.4.16 SHOWA DENKO K.K.

- 6.4.17 thyssenkrupp AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Applications of Bio-degradable Plastics

- 7.2 Increasing Research in Drug Delivery

- 7.3 Rising Regulations in Emerging Countries