|

市場調査レポート

商品コード

1851032

軍用無人地上車両:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Military Unmanned Ground Vehicle - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 軍用無人地上車両:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月19日

発行: Mordor Intelligence

ページ情報: 英文 125 Pages

納期: 2~3営業日

|

概要

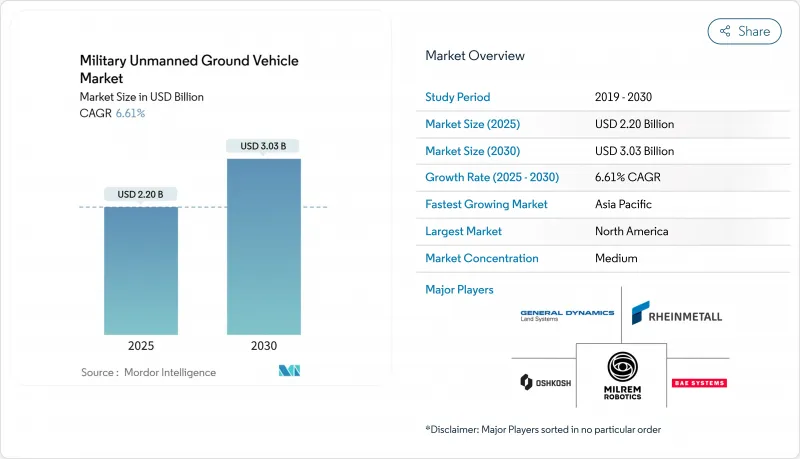

軍用無人地上車両の市場規模は2025年に22億米ドルと推定され、2030年には30億3,000万米ドルに達し、CAGR 6.61%で拡大すると予測されています。

拡大には、NATO諸国やインド太平洋諸国における防衛予算の着実な増加、リスクの高い作業をロボットに任せることで兵士を保護する必要性の高まり、GPSが使えない環境でも自律航行を可能にする人工知能の急速な進歩が関係しています。同時に、軍は見出しを飾る目新しさよりも、実績のある信頼性、サイバーセキュアなコマンドリンク、安定したロジスティクスを優先するため、採用ペースは爆発的というよりはむしろ統制されたままです。戦闘任務が引き続き需要の大半を占めているが、無人維持と両用配備の戦略的価値を軍が認識しているため、ロジスティクスと災害対応の役割が急速に台頭しています。プライム・コントラクターが既存の車両ファミリーを活用する一方、ロボット専業企業が脚式またはハイブリッド・モビリティ・コンセプトによってニッチを切り開くため、競合の激しさは中程度です。

世界の軍用無人地上車両市場の動向と洞察

NATO諸国とインド太平洋諸国の防衛予算の拡大

連合国の支出増は産業界に明確な需要シグナルを送っています。日本は2025年度に1,032億円(7億1,400万米ドル)を無人資産の防衛能力に確保し、米国は同じ会計サイクルで無人システムに101億米ドルを割り当てた。欧州は2024年度に軍事費を17%増額し、欧州防衛基金の一部を自律型地上プラットフォームに投入しました。こうした複数年にわたる予算増額は長期的な生産計画を下支えし、軍用無人地上車両市場が破壊的な好不況を繰り返すことなく拡大することを可能にしています。

兵士の安全を重視した自律型戦闘・兵站プラットフォーム

現代のドクトリンでは、無人システムは最前線に配置されます。ウクライナが負傷者避難のためにMilrem Robotics THeMISを実地で使用したことで、危険地帯から部隊を排除するというコンセプトが検証されました。米国陸軍の自律型輸送車両システムは、日常的な補給をロボットに委ねることで、持続可能性のスループットを50%向上させようとしています。この安全性の要請は、特に兵站と爆発性投射物の役割のために、重量クラス全般にわたる調達の原動力となっています。

C2リンクのサイバー/ジャミング脆弱性

ニアピアの敵は、制御チャンネルを妨害したり、なりすましたりすることができる強力な電子戦スーツを使用しており、無人ビークルをハイジャックやミッション失敗の危険にさらしています。米国空軍は現在、自律型プラットフォームを管理するあらゆるシステムにゼロ・トラスト原則を義務付けており、コストと設計の複雑さを高める暗号化と継続的認証のレイヤーを追加しています。したがってベンダーは、リンクの中断を緩和するために、冗長通信とオンボード自律性に多額の投資をしなければならないです。

セグメント分析

戦闘用プラットフォームは、2024年の軍用無人地上車両市場の54.65%を占めました。これは、兵士を守りながら殺傷能力を発揮することが必須であることを反映しています。米国陸軍のゼネラル・ダイナミクス社とテキストロン社のロボット戦闘車のプロトタイプは、2028年までに編隊レベルの試験が予定されています。ロジスティクスUGVは、最速のCAGR見通し7.87%を記録しました。これは、指揮官が輸送隊の露出を減らすために自動補給を目標としているためです。

永続的な情報・監視・偵察ミッションは、UGVの耐久性と低音響シグネチャを利用する一方、爆発物処理は共通ロボットシステムシリーズの下で成熟した調達ラインのままです。また、地雷や障害物を除去する工兵車両や経路整理車両、部隊の準備を支援する訓練ユニットやおとりユニットもあります。任務の拡大は、軍用無人地上車両市場の継続的な拡大を支えています。

遠隔操作ユニットが2024年の売上高の65.12%を占めるのは、国防総省指令3000.09が依然として殺傷判断に人間の判断を必要としているからです。それでも、重要な承認だけをオペレーターに求める半自律航法が急増しています。完全自律型ビークルは、センサー融合のブレークスルーにより中断のないデータリンクの必要性が減少するため、軍用無人地上車両市場内で最速のCAGR 10.24%で成長すると予測されています。

ハイブリッド制御モードにより、乗組員は妨害電波や地形の状況に応じて手動と自律行動を切り替えることができます。米国陸軍のxTechOverwatchコンペティションは、このような柔軟な操作コンセプトをネイティブにサポートするAIモジュールを提供する小規模企業にインセンティブを与えています。

地域分析

北米は、2024年の軍用無人地上車両市場で39.14%のシェアを維持し、乗員なしのシステムに対する国防総省の101億米ドルの資金と、超小型クラスから大型クラスまで広がる複数サービスの実験に支えられています。カナダの北極物流試験には、極寒プラットフォームに対するニッチな要件が追加されます。

アジア太平洋は、日本の1,032億円(~7億2,000万米ドル)の無人資産の項目と、自律システムのための共同AI研究を強調するインドのINDUS-Xイニシアチブによって牽引され、最高のCAGR 7.32%を記録すると予測されます。中国は軍民融合の下で開発を加速させ、韓国の多目的地上ロボットとオーストラリアのオプション乗員付き車両は、インド太平洋の緊張の中でサプライチェーンの確保を目指しています。

欧州は2024年の支出を17%増の6,930億米ドルに拡大し、欧州防衛基金はNATOの抑止力を強化するために自律型プラットフォームに助成金を投入します。ドイツがAeroVironment社に41台の先進EOD UGVを発注したことは、即座の運用需要を示しています。中東では、UAEを拠点とするEDGEとサウジアラビアのVision 2030を通じて固有のプログラムを追求し、アフリカでは国境警備ロボットを探求しており、これらは控えめながら安定した機会プールに貢献しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- NATOおよびインド太平洋諸国の防衛予算拡大

- 兵士の安全を重視する自律型戦闘/ロジスティクス・プラットフォーム

- AIを活用したセンサー融合と自律航行のブレークスルー

- マルチドメイン作戦における有人・無人チーム編成ドクトリン

- 耐EW地上中継ノードの需要

- 兼用需要を生み出す気候災害工学ミッション

- 市場抑制要因

- C2リンクのサイバー/ジャミング脆弱性

- 有人車両に比べて高い取得コストとライフサイクルコスト

- 致死的自律性をめぐる軍備管理の曖昧さ

- 相互運用規格の欠如

- バリューチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 用途別

- 戦闘

- 情報・監視・偵察(ISR)

- 爆発物処理(EOD)

- 物流と補給

- エンジニアリングとルート確保

- トレーニングとおとり

- モビリティプラットフォーム別

- 装輪

- 装軌

- 脚付き

- ハイブリッド

- 操作モード別

- 遠隔操作

- 自律型

- 半自律型

- 完全自律型

- 重量クラス別

- マイクロ(25kg未満)

- 小型(25~200kg)

- 中型(200~1,000kg)

- 重重量(1,000kg以上)

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- その他アジア太平洋地域

- 南米

- ブラジル

- その他南米

- 中東・アフリカ

- 中東

- サウジアラビア

- イスラエル

- アラブ首長国連邦

- その他中東

- アフリカ

- 南アフリカ

- その他アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- General Dynamics Land Systems(General Dynamics Corporation)

- Rheinmetall AG

- KNDS N.V.

- Oshkosh Defense, LLC

- L3Harris Technologies, Inc.

- ASELSAN A.S.

- QinetiQ Group

- Milrem Robotics(Milrem AS)

- Robo-Team Ltd.

- Teledyne Technologies Incorporated

- Israel Aerospace Industries Ltd.

- BAE Systems plc

- Textron Systems Corporation(Textron, Inc.)

- HDT Global

- Elbit Systems Ltd.

- Kongsberg Defence & Aerospace(Kongsberg Gruppen ASA)

- Hanwha Aerospace(Hanwha Corporation)

- Singapore Technologies Engineering Ltd.

- FNSS Savunma Sistemleri A.S.

- Hyundai Rotem Company

- Iveco Defence Vehicles(Iveco Group N.V.)