|

市場調査レポート

商品コード

1432968

航空機用ブレーキ:市場シェア分析、産業動向、成長予測(2024~2029年)Aircraft Brakes - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 航空機用ブレーキ:市場シェア分析、産業動向、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 102 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

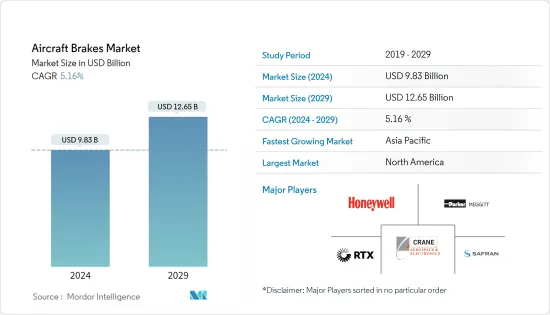

航空機用ブレーキ市場規模は2024年に98億3,000万米ドルと推定・予測され、2029年には126億5,000万米ドルに達し、予測期間(2024-2029年)のCAGRは5.16%で成長すると予測されます。

主なハイライト

- 航空部門はCOVID-19パンデミックにより比類なき課題に直面。パンデミックによってもたらされたサプライチェーンの混乱と労働力不足は、パンデミック期間中の市場成長を阻害しました。また、エアバスやボーイングのような主要な航空機OEMは、従業員の安全への懸念や政府規制により生産を停止し、市場の成長を阻害しました。2021年以降は、新型航空機の需要増と先進的な航空機ブレーキへの支出増により、市場は力強い回復を見せた。

- 民間および軍事分野における新世代航空機の調達は、航空機用ブレーキ市場開拓の主な理由の1つです。航空機の軽量化が重視されるようになり、航空機の電動化が進む中、(電動ブレーキのような)新しい軽量ブレーキが開発されています。

- 航空機のブレーキシステムは、航空機が安全かつ迅速に着陸できるようにする、すべての航空機に不可欠なコンポーネントです。新しい民間航空機や軍用航空機の需要の高まりと、高度なブレーキ・システムの開発に対する支出の増加が、航空機用ブレーキの需要を後押ししています。航空機用ブレーキシステムの技術的進歩と先進的なブレーキディスクのイントロダクションが市場の成長を後押ししています。

航空機用ブレーキ市場の動向

予測期間中、商用セグメントが最も高い成長を示すと予測

- 予測期間中、航空機用ブレーキ市場では商用セグメントが大きな成長を示すと予測されます。この成長は、世界中で増加する旅客輸送に対応するための航空機の受注と納入の増加に起因しています。現在、カーボンブレーキは航空業界で非常に人気があり、スチールブレーキに比べて軽量で、平均修理間隔(MTBR)が長いため、ナローボディ、ワイドボディ、リージョナルジェットのほとんどが採用しています。

- サフラン・ランディング・システムズのカーボン・ブレーキはエアバスA320ceo/neo、A350ファミリー、ボーイングB737NG/MAX、B787ドリームライナーに採用されています。ブレーキシステムの主な利点は、効率性と耐久性の向上です。サフランによると、B737に装備されたカーボンブレーキはオーバーホールとオーバーホールの間に2,200回の着陸が可能です。また、A320neoファミリーでは2,500回、A350では2,000回の着陸が可能です。

- しかし近年、民間航空部門は、軽量化と燃料費削減を主な目的として、より電気的なアーキテクチャへと移行しつつあります。このシフトは、軽量で性能が向上し、メンテナンスも容易な新しい電気ブレーキ技術の採用を後押ししています。航空会社は、燃料費と整備費の削減に役立つ電気ブレーキを採用する傾向にあります。民間航空機技術の動向は、予測期間中このセグメントの成長を支える主要因となると思われます。

予測期間中、アジア太平洋地域が最も高い成長を遂げる

- 予測期間中、航空機用ブレーキ市場で最も高い成長を示すのはアジア太平洋地域です。この成長は、航空交通量の増加、新しい空港の開発、民間機や軍用機の調達にかかる支出の増加によるものです。国際航空運送協会(IATA)によると、中国は2020年半ばに座席数で世界最大の航空市場になり、インドは2024年までに英国を抜いて世界第3位の航空市場になります。さらに、航空機のOEMであるエアバスは、アジア太平洋地域では2040年までに17,600機以上の航空機が新たに必要になると予測しています。

- 調達や受注に加え、この地域は、インド向けの先進中型戦闘機(AMCA)プログラム、韓国とインドネシア向けのKF-X、中国向けのCOMAC C919といった新型機の開発にも携わっています。こうした先進的な航空機の開発には、性能を向上させる新型のブレーキが必要になります。現在進行中の航空機の調達は、製造能力の向上とともに、予測期間中のこの地域の成長を押し上げると思われます。例えば、2022年8月、RUAGオーストラリアは、アジア太平洋(APAC)地域におけるF-35統合打撃戦闘機の車輪とブレーキプログラムのためのメンテナンス、修理、オーバーホール(MRO)認定サービスセンターになるために、ハネウェル・インターナショナル・インクと契約を締結しました。

航空機用ブレーキ業界の概要

航空機用ブレーキ市場は、少数のプレーヤーが市場で大きなシェアを占めており、その性質上、統合されています。市場の著名なプレーヤーは、RTX Corporation、Safran、Crane Aerospace &Electronics、Meggitt PLC、Honeywell International Inc.です。これらは、軍事、商業、一般航空分野の航空機のほとんどにブレーキとブレーキ・システムを供給している企業です。

高いブランド価値と航空機OEMとの長期契約により、これらの有力企業が市場を独占しており、新規参入企業がこの状況を利用することを困難にしています。現在初期段階にある電気ブレーキ技術への各社の投資も、近い将来、カーボンブレーキから電気ブレーキへの移行期に、各社が有力な地位を維持するのに役立つと予想されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- タイプ

- 電動ブレーキ

- カーボン製ブレーキ

- スチール製ブレーキ

- エンドユーザー

- 商用

- 軍用

- 一般航空

- 地域

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- ロシア

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- その他ラテンアメリカ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- カタール

- その他中東とアフリカ

- 北米

第6章 競合情勢

- 市場シェア分析

- 企業プロファイル

- Safran

- Meggitt PLC

- Honeywell International Inc.

- RTX Corporation

- Crane Aerospace & Electronics

- Beringer Aero

- Advent Aircraft Systems Inc.

- Tactair

- RAPCO, Inc.

- Matco Aircraft Landing Systems

- The Carlyle Johnson Machine Company, LLC

第7章 市場機会と今後の動向

The Aircraft Brakes Market size is estimated at USD 9.83 billion in 2024, and is expected to reach USD 12.65 billion by 2029, growing at a CAGR of 5.16% during the forecast period (2024-2029).

Key Highlights

- The aviation sector faced unmatched challenges due to the COVID-19 pandemic. Supply chain disruptions brought by the pandemic and labor shortages hindered the market growth during the pandemic. Also, key aircraft OEMs such as Airbus and Boeing halted production due to employee safety concerns and government regulations that hamper the market growth. The market showcased a strong recovery from 2021 due to increased demand for new aircraft and rising spending on advanced aircraft brakes.

- The procurement of newer generation aircraft in the commercial and military sectors is one of the major reasons for the development of the aircraft brakes market. With increasing emphasis on the reduction of the weight of aircraft and with the concept of more electric aircraft, new lightweight brakes are being developed (like electric brakes).

- Aircraft brake systems are essential components of all aircraft that allow the aircraft to land safely and quickly. Growing demand for new commercial and military aircraft and rising spending on the development of advanced braking systems propel the demand for aircraft brakes. Technological advancements in the aircraft braking system and the introduction of advanced brake discs drive the growth of the market.

Aircraft Brakes Market Trends

The Commercial Segment is Projected to Show Highest Growth During the Forecast Period

- The commercial segment is anticipated to show significant growth in the aircraft brakes market during the forecast period. The growth is attributed to the increase in aircraft orders and deliveries to cater to the growing passenger traffic around the world. Currently, carbon brakes are very much popular in the aviation industry, with most narrow-body, wide-body, and regional jets using them due to their lightweight, as compared to steel brakes, and more mean time between repairs (MTBR).

- Safran Landing Systems' carbon brakes feature on the Airbus A320ceo/neo and A350 family, Boeing B737NG/MAX, and the B787 Dreamliner. Increased efficiency and durability are the major benefits of braking systems. According to Safran, carbon brakes equipped with B737 can conduct 2,200 landings between overhauls. It also offers 2,500 landings on A320neo family aircraft and 2,000 landings for those on the A350.

- However, in recent years, the commercial aviation sector has been moving toward more electric architecture, with the main aim of reducing weight and lowering fuel costs. This shift is supporting the adoption of the new electric brake technology that comes with low weight and improved performance, as well as ease of maintenance. The airlines tend to use electric brakes, as they help in cutting down fuel and maintenance costs. The trend in commercial aircraft technology will be a major factor in supporting the growth of this segment during the forecast period.

Asia-Pacific to Experience the Highest Growth During the Forecast Period

- The Asia-Pacific will showcase the highest growth in the aircraft brakes market during the forecast period. The growth is due to increasing air traffic, the development of new airports, and rising expenditure on the procurement of commercial and military aircraft. According to the International Air Transport Association (IATA), China would become the largest aviation market in terms of seating capacity in mid-2020, and India will surpass the UK and become the third-largest aviation market in the world by 2024. Furthermore, Airbus, an aircraft OEM, forecasts that the Asia-Pacific region will need over 17,600 new aircraft by 2040.

- In addition to the procurements and orders, the region is involved in the development of new aircraft, like the Advanced Medium Combat Aircraft (AMCA) program for India, KF-X for Korea and Indonesia, and the COMAC C919 for China. The development of such advanced aircraft will require newer types of brakes, which will improve performance. The ongoing procurements of aircraft, along with the increasing manufacturing capabilities, will boost the growth of the region during the forecast period. For instance, in August 2022, RUAG Australia signed an agreement with Honeywell International Inc. to become a maintenance, repair, and overhaul (MRO) Authorised Service Centre for the F-35 Joint Strike Fighter Wheels and Brakes program in the Asia-Pacific (APAC) region.

Aircraft Brakes Industry Overview

The aircraft brakes market is consolidated in nature, with a presence of few players holding significant shares in the market. The prominent players in the market are RTX Corporation, Safran, Crane Aerospace & Electronics, Meggitt PLC, and Honeywell International Inc. These are firms that supply brakes and braking systems to most of the aircraft in the military, commercial, and general aviation sectors.

With high brand values and long-term contracts with aircraft OEMs, these prominent players dominate the market, making it difficult for new players to capitalize on this landscape. The investments by the companies in electric brake technology, which is currently in its initial stage, are also expected to help them maintain prominent positions, during the transition from carbon brakes to electric brakes, in the near future.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Electric Brakes

- 5.1.2 Carbon Brakes

- 5.1.3 Steel Brakes

- 5.2 End-User

- 5.2.1 Commercial

- 5.2.2 Military

- 5.2.3 General Aviation

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 France

- 5.3.2.4 Russia

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Mexico

- 5.3.4.3 Rest of Latin America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Qatar

- 5.3.5.4 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Share Analysis

- 6.2 Company Profiles

- 6.2.1 Safran

- 6.2.2 Meggitt PLC

- 6.2.3 Honeywell International Inc.

- 6.2.4 RTX Corporation

- 6.2.5 Crane Aerospace & Electronics

- 6.2.6 Beringer Aero

- 6.2.7 Advent Aircraft Systems Inc.

- 6.2.8 Tactair

- 6.2.9 RAPCO, Inc.

- 6.2.10 Matco Aircraft Landing Systems

- 6.2.11 The Carlyle Johnson Machine Company, LLC