|

市場調査レポート

商品コード

1536955

トラクター- 市場シェア分析、産業動向と統計、成長予測(2024年~2029年)Tractors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| トラクター- 市場シェア分析、産業動向と統計、成長予測(2024年~2029年) |

|

出版日: 2024年08月14日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

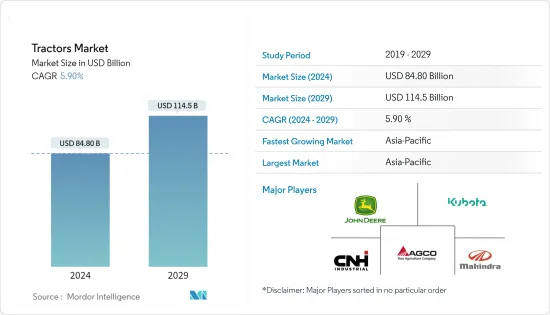

トラクター市場規模は2024年に848億米ドルと推定され、2029年には1,145億米ドルに達すると予測され、予測期間中(2024-2029年)のCAGRは5.90%で成長すると予測されます。

トラクター市場は、農業の機械化の進展、高馬力トラクターの需要増加、農業機械化を支援する政府の取り組みなどの要因によって、近年着実な成長を遂げています。農業の効率化においてトラクターが不可欠であることを反映して、市場規模は相当なものとなっています。精密農業技術の採用と持続可能な農法へのニーズは、トラクター市場の成長軌道にさらに貢献しています。

この市場の特徴は、John Deere、CNH Industrial(Case IHとNew Holland)、AGCO Corporation(Massey FergusonとFendt)、Kubotaなど、世界をリードする企業が存在することです。これらの企業は激しい競争を繰り広げ、欧州の農家の多様なニーズに応えるため、さまざまな出力容量と機能を備えたトラクターを提供しています。競争の中心は製品だけでなく、アフターセールス・サービスが農業機械分野で重要な役割を果たすため、サービスやサポート・ネットワークも含まれます。

長期的に見ると、世界のトラクター販売の増加に寄与している主な要因は、特に発展途上国における農業機械化率の上昇、農業労働コストの上昇、季節的な労働力不足、トラクターの買い替えサイクルの短縮です。しかし、業界の有力企業の中には、市場でのM&Aや新製品開発に注力しているところもあります。例えば

主なハイライト

- フランスの新興企業Seederal社は、2023年に電動トラクターの開発に乗り出すと発表しました。同社は現在、電気トラクターのプロトタイプを建設中で、160馬力の強大な出力能力を持つ見込みです。このイニシアチブは、持続可能な農業の実践と電動農業機械の採用を目指す世界の動向に沿ったものです。

- 2022年10月に開催されたクボタコネクトで、クボタはディーラーに新製品を公開しました。シリーズM7ジェネレーション4クボタM7は、畜産・飼料生産者向けの同社最大のトラクターです。

トラクター技術の進歩は欧州市場に大きな影響を与えています。GPSガイダンスシステム、テレマティクス、自動操舵などの精密農業技術は、最新のトラクターにますます統合されています。これらの技術は作業効率を高め、投入資材の使用量を最適化し、環境への影響を最小限に抑えることで持続可能な農業に貢献します。精密農業の採用は顕著な傾向であり、農家は生産性を向上させるためにスマート技術を搭載したトラクターに投資しています。

アジア太平洋は、インド、中国、日本などの新興主要経済国が、トラクターの導入を奨励するために、農機具の補助金や低クレジット率を提供することで、自国の農家を奨励しているため、今後5年間で大きな成長が見込まれます。このような動きは、これらの地域におけるトラクターの需要を促進する可能性が高いです。

トラクター市場動向

40馬力以下のトラクター・セグメントの成長は今後5年間で強化される見込み

世界のトラクター市場は、魅力的な動向を目の当たりにしています。困難な地形や多様な用途で優れた性能を発揮するため、大型で高馬力のトラクターへの関心が続いている一方で、40馬力(HP)未満のセグメントも今後5年間で大きな成長が見込まれています。

コンパクトトラクターと呼ばれるこれらのトラクターは、一般的にエンジン排気量が1500cc未満で、占有スペースも小さいです。そのため、小規模農場、狭いスペースの操縦、草刈り、耕うん、軽作業の運搬といった基本的な農作業に理想的です。

インドや中国などの主要トラクター市場は、近年40馬力以下のセグメントでプラス成長を報告しています。中小規模の農場では、従来の手作業に比べて効率と生産性を向上させるため、小型トラクターの採用が増加しています。一部の政府は、小規模農家がこれらのトラクターに投資することを奨励するために補助金や融資プログラムを提供しており、採用をさらに後押ししています。

メーカーはこの需要の増加を認識し、特に40馬力以下のセグメントに対応する新モデルを発表しています。例えば

- マヒンドラ・ジオ(インド):機動性と手頃な価格で知られる小型トラクターで、小規模農家や趣味家をターゲットにしています。

- John Deere 1025R(米国):草刈り、造園、軽作業用に設計された多用途のサブコンパクトトラクター。

アジア太平洋地域が2024年から2029年にかけて市場をリードすると予測される

アジア太平洋地域は、その広大で多様な農業景観により、世界のトラクター市場のリーダーとして際立っています。この地域は、幅広い気候と地形を含み、さまざまな作物と農法を支えています。多くのアジア太平洋諸国では農業が主要な経済活動であるため、トラクターの需要は本質的に高いです。小規模農家も大規模農家も同様に、耕作、植え付け、収穫にトラクターを頼りにしており、多様な農業分野で持続的な需要を牽引しています。

アジア太平洋は世界人口の大部分を擁する地域であり、食料安全保障の確保は同地域の多くの国にとって最優先事項です。トラクターは、農業生産性を向上させ、農家がより広い面積を効率的に耕作できるようにする上で重要な役割を果たしています。増加する人口に食料を供給する必要性から、機械化への投資に拍車がかかり、トラクターはアジア太平洋地域の農業生産と全体的な食料安全保障の強化に不可欠なものとなっています。

アジア太平洋の多くの政府は、経済発展と食糧生産における農業機械化の重要性を認識しています。その結果、トラクターを含む近代的農業機械の導入を奨励するための支援政策、補助金、財政的インセンティブを実施してきました。農作業の効率化と持続可能な慣行の促進を目指す政府の取り組みは、トラクター市場におけるアジア太平洋地域のリーダーシップに大きく貢献しています。

アジア太平洋地域は農業技術の進歩を受け入れており、近代的で技術的に高度なトラクターの普及につながっています。精密農業技術、GPSガイド付きトラクター、スマート農業ソリューションがこの地域で支持を得ています。農家は、資源利用を最適化し、環境への影響を低減し、全体的な農業生産性を高めるために、最先端技術を搭載したトラクターへの投資を増やしています。

- 2023年8月、ベンガルールのトラクター・耕うん機専門メーカーVST Tillers Tractorsは、専用の研究開発センター設立に100カロールインドルピーを投資する意向を表明しました。この多額の投資は、世界の農業分野における研究の促進と技術革新の促進を目的としています。このイニシアチブは、技術の進歩の最前線に立ち続け、世界の農業慣行の進化に貢献するというVST Tillers Tractorsのコミットメントを強調するものです。

- 2023年8月、日本の三菱マヒンドラ農業機械との協力により、マヒンドラ・アンド・マヒンドラは南アフリカのケープタウンでOJAプラットフォームによるトラクターの新シリーズを発売しました。このパートナーシップにより、20馬力から40馬力(14.91-29.82kW)のサブコンパクト、コンパクト、小型ユーティリティトラクターのシリーズがイントロダクションされました。OJAプラットフォームへの1,200カロールインドルピーの投資により、マヒンドラ・アンド・マヒンドラは来年、大型ユーティリティトラクターを発表する予定であり、技術的に先進的なトラクターの包括的なラインナップを提供するというコミットメントを強調しています。

トラクター業界の概要

トラクター市場は、複数の世界的・地域的プレーヤーが積極的に参入しているため、適度に統合されています。主なプレーヤーは以下の通りです。 Mahindra & Mahindra, Tractor, Kubota Corporation, Farm Equipment Limited, and HMT Limited are adopting agreements and product launches as key developmental strategies to improve the product portfolio of tractor products. For instance,

- 2023年12月、AutoNxt Automationは国内最大の農業展示会であるKrishithon 2023で最新のイノベーションを発表しました。イベント中、同社の創業者兼CEOであるKaustubh Dhonde氏は、45HPトラクターの新しいローダー・アプリケーションを誇らしげに紹介し、20HP電動トラクターのプロトタイプを発表しました。今回で16回目を迎えるKrishithon 2023は、AutoNxt Automationが農業セクターの変革に取り組む姿勢を示す極めて重要な場となった。

- 2023年7月、完全電動、運転者任意、コネクテッド・トラクターのMK-Vで有名なMonarch Tractor社は、シンガポールでの事業拡大を発表しました。この動きは、アジア太平洋地域における同社の大幅な成長とAI、ロボット工学、スマート農業技術への強い関心を意味します。事業拡張の決定は、アジア太平洋で急成長する先端農業技術への需要を活用するというモナーク・トラクターの戦略的位置づけを反映しています。

- 2022年11月、ニューホランドはSIMA 2022で、運転手のいない穀物カートの収穫アプリケーションであるレイヴン・オートノミー搭載のT8トラクターを初公開しました。これは、穀物カート収穫のための世界初の 促進要因レス農業技術であるOMNiDRIVEを組み込んだものです。この最先端技術スタックにより、農家は収穫機の運転席から 促進要因レス・トラクターを監視、同期、操作することができます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 市場の課題

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(市場規模)

- 馬力別

- 40馬力未満

- 40 HP-100 HP

- 100馬力以上

- 駆動タイプ別

- 二輪駆動

- 四輪駆動/全輪駆動

- 地域別

- 北米

- 米国

- カナダ

- その他北米

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- その他アジア太平洋

- 世界のその他の地域

- 南米

- 中東・アフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Deere and Company

- CNH Global NV(includes New Holland and Case IH)

- AGCO Corporation(includes Massey Ferguson, Valtra, Fendt, and Challenger)

- CLAAS KGaA mbH

- Mahindra and Mahindra Corporation

- Kubota Corporation

- Escorts Limited

- Tractors and Farm Equipment Limited(TAFE)

- Kuhn Group(Subsidiary of Bucher Industries)

- Yanmar Company Limited

- Deutz-Fahr

The Tractors Market size is estimated at USD 84.80 billion in 2024, and is expected to reach USD 114.5 billion by 2029, growing at a CAGR of 5.90% during the forecast period (2024-2029).

The tractor market has experienced steady growth in recent years, driven by factors such as increasing mechanization in agriculture, rising demand for high-horsepower tractors, and government initiatives supporting farm mechanization. The market size is substantial, reflecting the essential nature of tractors in enhancing agricultural efficiency. The adoption of precision farming techniques and the need for sustainable farming practices further contribute to the growth trajectory of the tractor market.

The market is characterized by the presence of leading global players, including John Deere, CNH Industrial (Case IH and New Holland), AGCO Corporation (Massey Ferguson and Fendt), and Kubota. These companies compete intensely, offering a diverse range of tractors with varying power capacities and features to cater to the diverse needs of European farmers. The competition is not only centered around product offerings but also involves service and support networks, as after-sales services play a critical role in the agricultural machinery sector.

Over the long term, the key factors contributing to the increase in worldwide tractor sales are increasing farm mechanization rates, especially in developing nations, rising farm labor costs, seasonal labor shortages, and shorter tractor replacement cycles. However, some of the prominent players in the industry are focusing on mergers and acquisitions and new product development in the market. For instance,

Key Highlights

- The French start-up Seederal announced its venture into the development of an electric tractor in 2023. The company is currently in the process of constructing the electric tractor prototype, which is expected to possess a formidable power capacity of 160 hp. This initiative aligns with the global trend toward sustainable farming practices and the adoption of electric-powered agricultural machinery.

- In October 2022, At Kubota Connect, the manufacturer gave dealers a sneak peek at the new products. Series M7 Generation 4 The Kubota M7s are the company's largest tractors, aimed at livestock and forage producers.

Advancements in tractor technology have significantly influenced the European market. Precision farming technologies, such as GPS guidance systems, telematics, and automated steering, are increasingly integrated into modern tractors. These technologies enhance operational efficiency, optimize input usage, and contribute to sustainable agriculture by minimizing environmental impact. The adoption of precision farming practices is a notable trend, and farmers are investing in tractors equipped with smart technologies to improve productivity.

Asia-Pacific is expected to witness significant growth in the next five years as emerging key economies like India, China, and Japan are encouraging farmers in their countries by offering subsidized farm equipment and low credit rates to encourage tractor adoption. Such developments are likely to drive the demand for tractors in these regions.

Tractors Market Trends

The Below 40 HP Tractors Segment's Growth is Expected to be Bolstered over the Next Five Years

The global tractor market is witnessing a fascinating trend: while there's a continued interest in larger, high-horsepower tractors for superior performance in difficult terrains and diverse applications, the segment below 40 horsepower (HP) is also expected to experience significant growth in the coming five years.

These tractors, often referred to as compact tractors, are typically less than 1500 cc in engine displacement and occupy less space. This makes them ideal for smaller farms, maneuvering tight spaces, and handling basic agricultural tasks like mowing, tilling, and light-duty transport.

Major tractor markets like India and China have reported positive growth in the sub-40 HP segment in recent years. Small and medium-scale farms are increasingly adopting compact tractors to improve efficiency and productivity compared to traditional manual labor. Some governments offer subsidies or loan programs to encourage small farmers to invest in these tractors, further boosting adoption.

Manufacturers are recognizing this increasing demand and launching new models specifically catering to the sub-40 HP segment. For instance:

- Mahindra Gio (India): A compact tractor known for its maneuverability and affordability, targeting small farms and hobbyists.

- John Deere 1025R (United States): A versatile sub-compact tractor designed for mowing, landscaping, and light utility tasks.

Asia-Pacific is Anticipated to Lead the Market Between 2024 and 2029

Asia-Pacific stands out as a leader in the global tractor market due to its vast and diverse agricultural landscape. The region encompasses a wide range of climates and topographies, supporting a variety of crops and farming practices. With agriculture being a primary economic activity in many Asia-Pacific countries, the demand for tractors is inherently high. Small-scale and large-scale farmers alike rely on tractors for plowing, planting, and harvesting, driving sustained demand across diverse agricultural sectors.

Asia-Pacific is home to a significant portion of the world's population, and ensuring food security is a top priority for many nations in the region. Tractors play a crucial role in increasing agricultural productivity, allowing farmers to cultivate larger areas efficiently. The need to feed growing populations has spurred investments in mechanization, making tractors indispensable for enhancing farm output and overall food security in Asia-Pacific.

Many governments in Asia-Pacific have recognized the importance of mechanized agriculture for economic development and food production. As a result, they have implemented supportive policies, subsidies, and financial incentives to encourage the adoption of modern agricultural machinery, including tractors. Government initiatives aimed at improving farm efficiency and promoting sustainable practices contribute significantly to the leadership of Asia-Pacific in the tractor market.

Asia-Pacific has embraced technological advancements in agriculture, leading to the widespread adoption of modern and technologically advanced tractors. Precision farming techniques, GPS-guided tractors, and smart farming solutions have gained traction in the region. Farmers are increasingly investing in tractors equipped with cutting-edge technologies to optimize resource utilization, reduce environmental impact, and enhance overall agricultural productivity.

- In August 2023, VST Tillers Tractors, a Bengaluru-based manufacturer specializing in tractors and tillers, declared its intention to invest INR 100 crore in establishing a dedicated research and development center. This substantial investment is aimed at advancing research and fostering innovation in the global agricultural sector. The initiative underscores VST Tillers Tractors' commitment to staying at the forefront of technological advancements and contributing to the evolution of farming practices worldwide.

- In August 2023, in a collaborative effort with Mitsubishi Mahindra Agriculture Machinery, Japan, Mahindra and Mahindra launched a new line of tractors under the OJA platform in Cape Town, South Africa. This partnership led to the introduction of a series of sub-compact, compact, and small utility tractors, ranging from 20 hp to 40 hp (14.91-29.82 kW). With an investment of INR 1,200 crore in the OJA platform, Mahindra and Mahindra plans to unveil large utility tractors next year, highlighting their commitment to delivering a comprehensive range of technologically advanced tractors.

Tractors Industry Overview

The tractor market is moderately consolidated as it witnesses active engagement from several global and regional players. Major players such as Mahindra & Mahindra, Tractor, Kubota Corporation, Farm Equipment Limited, and HMT Limited are adopting agreements and product launches as key developmental strategies to improve the product portfolio of tractor products. For instance,

- In December 2023, AutoNxt Automation unveiled its latest innovations at Krishithon 2023, the largest agricultural exhibition in the country. During the event, Kaustubh Dhonde, the company's Founder and CEO, proudly introduced a new Loader application in a 45HP tractor and presented the prototype of a 20HP Electric Tractor. Krishithon 2023, now in its 16th edition, served as a pivotal platform for AutoNxt Automation to showcase its dedication to transforming the agricultural sector.

- In July 2023, Monarch Tractor, renowned for its MK-V, a fully electric, driver-optional, and connected tractor, announced the expansion of its operations in Singapore. This move signifies substantial growth and a strong interest in the company's AI, robotics, and smart farming technology within Asia Pacific. The decision to extend operations reflects Monarch Tractor's strategic positioning to capitalize on the burgeoning demand for advanced agricultural technologies in Asia-Pacific.

- In November 2022, At SIMA 2022, New Holland debuted the T8 tractor with Raven Autonomy, a driverless grain cart harvest application. It incorporates OMNiDRIVE, the world's first driverless agriculture technology for grain cart harvesting. The cutting-edge technology stack allows the farmer to monitor, synchronize, and operate a driverless tractor from the harvester's cab.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Challenges

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in USD billion)

- 5.1 By Horsepower

- 5.1.1 Below 40 HP

- 5.1.2 40 HP - 100 HP

- 5.1.3 Above 100 HP

- 5.2 By Drive Type

- 5.2.1 Two-wheel Drive

- 5.2.2 Four-wheel Drive/All-wheel Drive

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Spain

- 5.3.2.5 Italy

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Rest of the World

- 5.3.4.1 South America

- 5.3.4.2 Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles*

- 6.2.1 Deere and Company

- 6.2.2 CNH Global NV (includes New Holland and Case IH)

- 6.2.3 AGCO Corporation (includes Massey Ferguson, Valtra, Fendt, and Challenger)

- 6.2.4 CLAAS KGaA mbH

- 6.2.5 Mahindra and Mahindra Corporation

- 6.2.6 Kubota Corporation

- 6.2.7 Escorts Limited

- 6.2.8 Tractors and Farm Equipment Limited (TAFE)

- 6.2.9 Kuhn Group (Subsidiary of Bucher Industries)

- 6.2.10 Yanmar Company Limited

- 6.2.11 Deutz-Fahr