|

市場調査レポート

商品コード

1403970

患者モニタリング:市場シェア分析、産業動向と統計、2024年~2029年の成長予測Patient Monitoring - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 患者モニタリング:市場シェア分析、産業動向と統計、2024年~2029年の成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 144 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

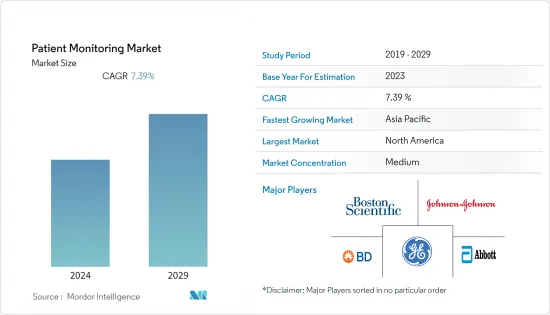

世界の患者モニタリング市場規模は、2024年の438億米ドルから2029年には626億米ドルに成長し、予測期間(2024年~2029年)のCAGRは7.39%を記録すると予測されています。

患者モニタリング市場の基準年の市場規模は371億1,597万米ドルで、予測期間中のCAGRは8.97%と予測されます。

パンデミックの発生は患者モニタリング市場に影響を与えました。パンデミックの間、COVID-19患者の常時モニタリングの必要性から、神経モニタリング、呼吸器、心臓デバイスなどの患者モニタリングデバイスの需要が急激に増加しました。例えば、2022年10月に発表されたNCBIの研究によると、ウェアラブル呼吸センサーは、COVID-19によって引き起こされる呼吸数や咳の回数の異常などの生体力学的信号や、呼気からのウイルスバイオマーカーなどの生化学的信号を監視できるため、パンデミック中に広く使用されました。このため、市場はパンデミック期に健全な成長を遂げ、予測期間中も上昇傾向を維持すると予想されます。

患者モニタリング市場の成長は、ライフスタイルの変化による慢性疾患の負担増、高齢者人口の増加、在宅モニタリングや遠隔モニタリングへの嗜好の高まり、ポータブル機器の使いやすさなどに起因しています。例えば、米国疾病予防管理センター(CDC)の2022年6月の更新によると、糖尿病、がん、心臓病、脳卒中などの1つ以上の慢性疾患が米国人の10人中6人に影響を及ぼしています。これらやその他の慢性疾患は、米国における医療費の主な原因であり、死亡や身体障害の重大な原因となっています。同様に、2022年4月にNCBIが発表したデータによると、2022年には65歳以上のアメリカ人のうち推定650万人がアルツハイマー型認知症を患っています。その数は2060年までに1,380万人に増加すると予想されています。このように慢性疾患の負担が大きいため、これらの疾患では常時監視が必要であり、患者監視装置の出番となるため、患者監視装置の需要が高まると予想されます。さらに、常時モニタリングすることで、再入院率を下げ、回避可能な入院を防ぎ、不必要な診察の回数を減らし、旅行関連費用を削減することができます。適切な導入により、患者モニタリング技術は質の高いヘルスケアへのアクセスを拡大し、時間と費用を節約することができます。このような要因により、予測期間中にかなりの市場成長が見込まれます。

さらに、事業拡大や製品発売などの取り組みも市場成長の要因となっています。例えば、2021年9月、メドトロニックのインド子会社はStasis Health社と提携し、コネクテッドケアのベッドサイド・マルチパラメーター・モニタリングシステムであるStatis Monitorへのアクセスをインド全土に拡大しました。同様に、2021年7月、テルモ株式会社は日本のDexcom G6持続グルコースモニタリングシステムを発売しました。米国に本社を置くDexcom, Inc.が製造し、テルモが日本での独占販売契約を結んでいます。こうした発展は、予測期間中の患者モニタリング市場の成長を後押しすると思われます。

しかし、患者モニタリングシステムの導入に対するヘルスケア業界関係者の抵抗や技術コストの高さが、予測期間中の市場成長の妨げになる可能性が高いです。

患者モニタリング市場動向

心臓病学セグメントは予測期間中にかなりの市場成長が見込まれる

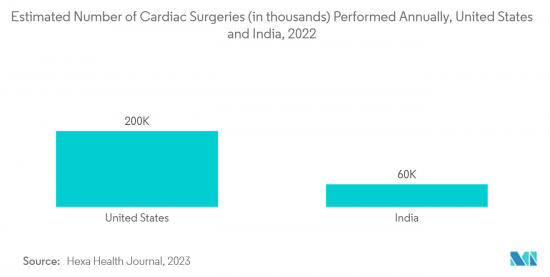

心臓病学では、患者モニタリング装置は心臓や循環器系全体のさまざまな障害や異常の診断とモニタリングに使用されます。同分野の成長を促進する主な要因は、心血管疾患による症例数や死亡者数の増加、心臓手術件数の増加です。例えば、2023年1月のCDC更新によると、米国では毎年約620万人の成人が心不全を患っています。同様に、HexaHealthが2022年10月に発行した雑誌によると、米国では年間およそ200万件、インドでは年間6万件の手術が行われています。手術後の継続的な患者モニタリングは、合併症の可能性と回復率を追跡するために不可欠であり、心臓患者モニタリングが活躍します。したがって、心臓手術の増加もこのセグメントの成長を急増させると予想されます。

さらに、心臓モニタリング分野の市場参入企業による製品投入や好意的な取り組みも、同分野の成長を後押しする可能性が高いです。例えば、GEヘルスケアは2022年6月にワイヤレス患者モニタリングシステム「Portrait Mobile」を発売しました。この製品は、一般病棟や手術後の患者の呼吸数、酸素飽和度、脈拍数を継続的に把握することができ、臨床医が早期に対処して重大な有害事象を回避することを可能にします。同様に、2021年1月、ボストン・サイエンティフィック・コーポレーションは、成人および小児患者向けの遠隔およびウェアラブル心臓モニターを提供する非公開会社であるPreventiceSolutions, Inc.を買収しました。この買収により、ボストン・サイエンティフィック・コーポレーションは、植え込み型心臓モニター市場で強力な足場を築くことになります。ボストン・サイエンティフィック社の心臓モニターは、不整脈を検出するための埋め込み型診断装置です。このため、同分野は予測期間中に大きく成長すると予測されています。

北米地域が予測期間中に大きな市場シェアを占める

北米の患者モニタリング市場は大幅な成長が見込まれ、予測期間中も同様の動向を示すと予測されます。老人人口の増加、慢性疾患の罹患率の上昇、ワイヤレスおよびポータブルシステムに対する需要の高まり、自己負担額を削減することを目的とした高度な償還構造が、大きな市場シェアの主な要因です。例えば、カナダ公衆衛生局が2021年12月に発表した報告書によると、65歳以上の人口10万人当たりの虚血性心疾患の粗発生率は男性2,306.9人、女性1,537人、慢性閉塞性肺疾患は男性1,750.6人、女性1,411.4人でした。また、カナダ慢性疾患サーベイランス・システムが2022年11月に発表した報告書によると、慢性疾患を抱える65歳以上の成人は、今後数年間で約630万人になると予想されています。そのため、予測期間中にかなりの市場成長が見込まれます。

北米では、米国が予測期間中に大きな成長を遂げると予想されています。主要企業による製品上市と同国での製品承認が市場の主な促進要因となっています。例えば、2021年7月、Abbott社は挿入型心臓モニターJot Dxを発表しました。これはデータ負担を軽減し、異常な心臓リズムを診断するように設計されています。同様に、2022年7月、スイスに本拠を置く医療技術企業Sleepizは、非接触型呼吸・心拍測定装置Sleepiz One+の米国FDA認可を取得し、米国で発売されました。Sleepiz One+は、睡眠中の患者データを非接触で監視・記録する初の呼吸監視装置の一つです。Sleepiz技術により、医師はもはや無作為の検診測定に頼ることなく、継続的なデータにアクセスできるため、患者の健康について新たな視点を持つことができます。このように、革新的な製品の発売と北米地域における慢性疾患の有病率の上昇により、市場は予測期間中に高い成長率を示すと予想されます。

患者モニタリング産業概要

患者モニタリング市場は適度な競争があり、複数の大手企業で構成されています。各社は、合併、新製品発売、買収、提携など特定の戦略的イニシアチブを実施しており、市場での地位強化に役立っています。主な参入企業は、Abbott Laboratories、Baxter International Inc.、Boston Scientific Corporation、Becton, Dickinson and Company、General Electric Company(GEヘルスケア)、Johnson &Johnsonなどです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- ライフスタイルの変化による慢性疾患の負担増

- 在宅・遠隔モニタリングへの嗜好の高まり

- 市場抑制要因

- 患者モニタリングシステムの導入に対するヘルスケア業界関係者の抵抗

- 技術コストの高さ

- ポーターのファイブフォース分析

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(市場規模-米ドル)

- デバイスタイプ別

- 血行動態モニタリング機器

- 神経モニタリング機器

- 心臓モニタリング機器

- マルチパラメーターモニター

- 呼吸器モニタリング装置

- その他の機器

- 用途別

- 心臓病学

- 神経学

- 呼吸器

- 胎児・新生児

- 体重管理・フィットネスモニタリング

- その他の用途

- エンドユーザー別

- 在宅ヘルスケア

- 病院・診療所

- その他のエンドユーザー

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Abbott Laboratories

- Baxter International Inc.

- Boston Scientific Corporation

- Becton, Dickinson and Company

- General Electric Company(GE Healthcare)

- Johnson & Johnson

- Masimo Corporation

- Medtronic PLC

- Omron Corporation

- Koninklijke Philips NV

- Dragerwerk AG & Co. KGaA

第7章 市場機会と今後の動向

The Global Patient Monitoring Market size is expected to grow from USD 43.8 billion in 2024 to USD 62.6 billion by 2029, registering a CAGR of 7.39% during the forecast period (2024-2029).

The patient monitoring market was valued at USD 37,115.97 million in the base year and is expected to register a CAGR of 8.97% over the forecast period.

The outbreak of the pandemic impacted the patient monitoring market. During the pandemic, the demand for patient monitoring devices such as neuromonitoring, respiratory, and cardiac devices drastically increased due to the need for constant monitoring of COVID-19 patients. For instance, according to the NCBI study published in October 2022, wearable respiratory sensors were widely used during the pandemic as they can monitor biomechanical signals, such as the abnormities in respiratory rate and cough frequency caused by COVID-19, as well as biochemical signals, such as viral biomarkers from exhaled breaths. Thus, the market witnessed healthy growth during the pandemic and is expected to maintain an upward trend over the forecast period.

The growth of the patient monitoring market is attributed to the rising burden of chronic diseases due to lifestyle changes, growth in the geriatric population, growing preference for home and remote monitoring, and the ease of use of portable devices. For instance, according to the June 2022 update of the Centers for Disease Control and Prevention (CDC), one or more chronic diseases, such as diabetes, cancer, heart disease, and stroke, affect six out of ten Americans. These and other chronic illnesses are the main contributors to health care costs and the significant causes of death and disability in the United States. Similarly, according to the data published by the NCBI in April 2022, an estimated 6.5 million Americans aged 65 and older were living with Alzheimer's dementia in 2022. The number is expected to grow to 13.8 million by 2060. Thus, such a high burden of chronic diseases is expected to increase the demand for patient monitoring devices as these diseases require constant monitoring, in which patient monitoring devices come into play. In addition, constant monitoring reduces readmission rates, prevents avoidable hospitalizations, decreases the number of unnecessary trips to the doctor's office, and reduces travel-related expenses. With the proper implementation, patient monitoring technologies can expand access to quality healthcare and save time and money. Thus, considerable market growth is expected over the forecast period due to such factors.

Additionally, initiatives such as expansion and product launches are other factors responsible for the market's growth. For instance, in September 2021, the Indian subsidiary of Medtronic partnered with Stasis Health to expand access to Statis Monitor, a connected care bedside multi-parameter monitoring system across India. Similarly, in July 2021, Terumo Corporation launched Japan's Dexcom G6 continuous glucose monitoring system. Dexcom, Inc., based in the United States, manufactures the product, and Terumo holds the exclusive distribution agreement in Japan. Such developments are likely to bolster the growth of the patient monitoring market over the forecast period.

However, resistance from healthcare industry professionals toward adopting patient monitoring systems and the high cost of technology will likely hinder the market growth over the forecast period.

Patient Monitoring Market Trends

The Cardiology Segment is Expected to Witness Considerable Market Growth Over the Forecast Period

In cardiology, patient monitoring devices are used to diagnose and monitor various disorders or abnormalities of the heart and the overall cardiovascular system. The major factor driving the segment's growth is the rising number of cases and deaths due to cardiovascular diseases and the increasing number of cardiac surgeries. For instance, according to the CDC update in January 2023, around 6.2 million adults in the United States have heart failure yearly. Similarly, according to the journal published by HexaHealth in October 2022, around 2,00,000 surgeries were performed in the United States and 60,000 in India annually. Post-surgery continuous patient monitoring is essential to track any possibility of complications and the recovery rate in which cardiac patient monitoring comes into play. Thus, increasing cardiac surgeries is also expected to surge the segment growth.

Furthermore, product launches and favorable initiatives by the market players in the cardiac monitoring space are also likely to fuel the growth of this segment. For instance, in June 2022, GE Healthcare launched its wireless patient monitoring system, Portrait Mobile. The product helps capture respiration rate, oxygen saturation, and pulse rate for general ward and post-surgery patients continuously, allowing clinicians to act early and avert serious adverse events. Similarly, in January 2021, Boston Scientific Corporation acquired PreventiceSolutions, Inc., a privately held company offering remote and wearable cardiac monitors for adults and pediatric patients. The acquisition will establish a strong footprint for Boston Scientific Corporation in the implantable cardiac monitor market. It is an implantable diagnostic device for detecting arrhythmias. Therefore, owing to the above factors, the segment is anticipated to grow considerably over the forecast period.

North America Region Holds a Considerable Market Share Over the Forecast Period

The North American patient monitoring market is expected to witness considerable growth and is estimated to show a similar trend over the forecast period. The increasing geriatric population, rising incidences of chronic diseases, growing demand for wireless and portable systems, and sophisticated reimbursement structures aimed at cutting out-of-pocket expenditure levels are the major factors attributed to its large market share. For instance, according to a report published by the Public Health Agency of Canada in December 2021, the crude incidence rate per 100,000 persons aged 65 years and more for ischemic heart disease was 2,306.9 in men and 1,537 for women and chronic obstructive pulmonary disease was 1,750.6 in men and 1,411.4 in women. In addition, according to the report published by the Canadian Chronic Disease Surveillance System in November 2022, the overall number of adults aged 65 years and older who were to be living with chronic conditions were expected to be about 6.3 million in the coming years. Thus, owing to such instances, considerable market growth is expected over the forecast period.

In the North America, the United States is expected to witness significant growth over the forecast period. The product launches by the key players and product approvals in the country are the major drivers for the market. For instance, in July 2021, Abbott introduced Jot Dx, an insertable cardiac monitor. It is designed to reduce data burden and diagnose abnormal heart rhythms. Similarly, in July 2022, Switzerland-based medical technology company Sleepiz received the U.S. FDA clearance for Sleepiz One+ contactless respiration and heart rate measuring device and was launched in the United States. Sleepiz One+ is one of the first respiratory monitoring devices that non-contactly monitors and records patient data during sleep. Sleepiz technology enables a new perspective on patient health, as doctors no longer rely on random check-up measurements but instead have access to continuous data. Thus, owing to the launch of innovative products and the rising prevalence of chronic diseases in the North American region, the market is expected to witness a high growth rate over the forecast period.

Patient Monitoring Industry Overview

The patient monitoring market is moderately competitive and consists of several major players. The companies are implementing certain strategic initiatives, such as mergers, new product launches, acquisitions, and partnerships, that help strengthen their market position. The key players in the market are Abbott Laboratories, Baxter International Inc., Boston Scientific Corporation, Becton, Dickinson and Company, General Electric Company (GE Healthcare), and Johnson & Johnson, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Burden of Chronic Diseases due to Lifestyle Changes

- 4.2.2 Growing Preference for Home and Remote Monitoring

- 4.3 Market Restraints

- 4.3.1 Resistance from Healthcare Industry Professionals Toward the Adoption of Patient Monitoring Systems

- 4.3.2 High Cost of Technology

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Type of Device

- 5.1.1 Hemodynamic Monitoring Devices

- 5.1.2 Neuromonitoring Devices

- 5.1.3 Cardiac Monitoring Devices

- 5.1.4 Multi-parameter Monitors

- 5.1.5 Respiratory Monitoring Devices

- 5.1.6 Other Types of Devices

- 5.2 By Application

- 5.2.1 Cardiology

- 5.2.2 Neurology

- 5.2.3 Respiratory

- 5.2.4 Fetal and Neonatal

- 5.2.5 Weight Management and Fitness Monitoring

- 5.2.6 Other Applications

- 5.3 By End-User

- 5.3.1 Home Healthcare

- 5.3.2 Hospitals and Clinics

- 5.3.3 Other End-Users

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Abbott Laboratories

- 6.1.2 Baxter International Inc.

- 6.1.3 Boston Scientific Corporation

- 6.1.4 Becton, Dickinson and Company

- 6.1.5 General Electric Company (GE Healthcare)

- 6.1.6 Johnson & Johnson

- 6.1.7 Masimo Corporation

- 6.1.8 Medtronic PLC

- 6.1.9 Omron Corporation

- 6.1.10 Koninklijke Philips NV

- 6.1.11 Dragerwerk AG & Co. KGaA