|

市場調査レポート

商品コード

1438095

皮膚がん診断および治療:世界市場シェア分析、業界動向と統計、成長予測(2024~2029年)Global Skin Cancer Diagnostics and Therapeutics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 皮膚がん診断および治療:世界市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

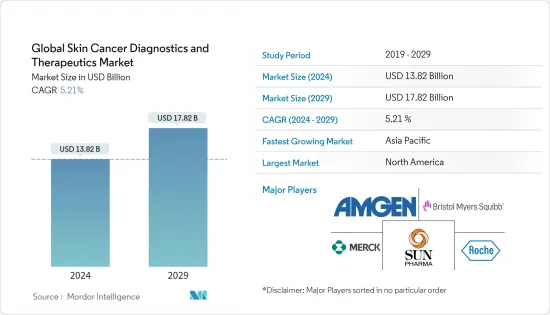

世界の皮膚がん診断および治療市場規模は、2024年に138億2,000万米ドルと推定され、2029年までに178億2,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に5.21%のCAGRで成長します。

新型コロナウイルス感染症(COVID-19)のパンデミックの発生は、調査対象の市場に大きな影響を与えました。パンデミックが始まった後、世界保健機関(WHO)のガイドラインは、慢性疾患患者は屋内にとどまるよう提案しました。したがって、これが皮膚がん診断市場の妨げとなっていました。しかし、COVID-19の影響で、非黒色腫皮膚がん(NMSC)または黒色腫がんの患者に対する治療の遅れの影響を研究する調査の数が急増しました。 2021年8月に発表された研究「COVID-19感染症のパンデミックが皮膚がん患者の生活の質に及ぼす影響」では、がん患者は免疫不全/免疫抑制状態のため、基礎となる腫瘍疾患と負担に応じて、以下のような症状に陥る可能性があると述べられています。重度のCOVID-19感染症を発症し、集中治療室での治療が必要になるリスクが高くなります。したがって、パンデミック中に皮膚がんの発生率が増加したことで、皮膚がんの診断が増加し、新しい高度な治療法への需要が生まれました。したがって、パンデミックは、パンデミック期の皮膚がん診断および治療にプラスの影響を与えると予測されています。

市場の成長を促進する特定の要因には、皮膚がんの発生率の増加、広範な研究開発(R&D)パイプライン、皮膚がんに関する意識の高まりなどが含まれます。たとえば、米国臨床腫瘍学会が2022年 2月に更新したところによると、2020年には推定324,635人が黒色腫と診断され、2020年には米国で約2,400人の15歳から29歳の人々が黒色腫と診断されたと推定されています。したがって、人口における皮膚がんの有病率は、調査対象の市場の成長を促進しています。

さらに、研究開発の増加により、予測期間中に皮膚がん治療薬の需要が高まると予測されています。

したがって、上記の要因は集合的に、予測期間中に調査された市場の成長に起因すると考えられます。ただし、治療法と厳格な規制枠組みに関連する過度のコストは、予測期間中の市場の成長を妨げると予想されます。

皮膚がん診断および治療市場の動向

がんタイプ別の非黒色腫セグメントは予測期間中に増加すると予想される

非黒色腫皮膚がんは皮膚細胞から発生し、がん性(悪性)増殖は、近くの組織に増殖して破壊する可能性のあるがん細胞のグループです。体の他の部分に広がる(転移する)こともありますが、非黒色腫皮膚がんではこれはまれです。したがって、非黒色腫の症例の増加がこの分野の成長を促進すると予想されます。

パンデミック中にすべての皮膚がんに対するパンデミックの影響を分析する調査が増加しました。 2021年12月に発表された研究「COVID-19症時代の皮膚がんに対する治療遅延の影響:症例対照研究」では、議論の中で、COVID-19感染症のパンデミックが皮膚がんの発生率の増加と皮膚がんの手術の増加に関連していると述べた。ロックダウン後の期間に実施された研究は、非黒色腫がんの一種である扁平上皮がん(SCC)に対してのみ有意でした。したがって、パンデミック中に診断と改善された治療法の需要が増加し、非黒色腫セグメントにプラスの影響を与えました。

2022年 5月に更新された皮膚がん財団のデータは、非黒色腫皮膚がんの約90%が太陽からの紫外線(UV)放射線への曝露に関連していることを示しています。皮膚がん財団の推定によると、基底細胞がん(BCC)は皮膚がんの最も一般的な形態であり、米国では毎年推定360万件のBCCが診断されています。また、上記の情報源は、米国における皮膚がんの年間治療費は81億米ドルと推定されており、非黒色腫皮膚がんでは約48億米ドル、黒色腫では33億米ドルであると報告しています。したがって、非黒色腫タイプの皮膚がんの発生率とそれに関連する治療費により、米国および世界中の他の郡で高度な治療法と診断の機会が生まれると予想されます。これにより、セグメント全体の成長が促進されることが期待されます。

この分野での研究開発の増加に関する洞察も、この分野の成長を促進すると予測されています。たとえば、2021年12月、ノーサンプトン総合病院NHSトラストの研究者と放射線科医は、特定の種類の基底細胞または扁平上皮皮膚がんの治療に使用される高度に標的を絞った放射線治療技術である皮膚近接照射療法を導入しました。

したがって、非黒色腫セグメントは成長しており、予測期間中に大幅な成長が見込まれます。したがって、調査対象市場の成長を促進します。

予測期間中、北米が市場を独占すると予想される

北米は、予測期間を通じて皮膚がんおよび治療薬市場全体を支配すると予想されます。市場の成長は、皮膚がんの有病率や発生率の増加などの要因によるものです。米国はこの地域で最大の市場になると予想されています。

がん治療薬の研究開発(R&D)において確立されたヘルスケアインフラに焦点を当てた市場プレーヤーは、最近の製品発売と米国における皮膚がんの負担の増大と相まって、この国の市場の主な成長要因となっています。たとえば、2021年7月、米国とカナダ以外ではMSDとして知られるメルクは、メルクの抗PD-1療法であるキイトルーダの単独療法としてのラベル拡大の承認を食品医薬品局(FDA)から得た。手術や放射線では治癒できない局所進行性皮膚扁平上皮がん(cSCC)患者の数。さらに、2022年 5月には、世界有数のライフサイエンス企業の1つであるLabcorp.が、黒色腫の治療選択肢のための新しいアッセイを開始しました。この新しい検査により、腫瘍組織における免疫組織化学(IHC)によるリンパ球活性化遺伝子 3(LAG-3)の発現レベルの測定が可能になります。 LAG-3は、黒色腫患者において明らかな臨床上の利点を持つ免疫腫瘍学の標的です。この検査は、臨床試験と患者のケアと治療の両方で使用できます。これらの最近の開発は、国内の皮膚がん診断および治療の需要を促進し、この地域の市場全体の成長を促進すると予想されます。

さらに、2022年5月に更新された皮膚がん財団のデータは、2022年に米国で推定197,700例の黒色腫が診断されることを示しています。そのうち97,920例は、表皮(最上層)に限定された原位置(非侵襲的)症例となります。 99,780例は表皮から皮膚の2番目の層(真皮)に侵入する侵襲性のものです。侵襲的症例のうち、57,180人が男性、42,600人が女性となります。したがって、国内の皮膚がんの発生率と有病率は、国内での治療のための高度な診断法と治療法の開発を要求しており、この地域の市場全体の成長を推進しています。

したがって、上記の要因に従って、米国の皮膚がんの症例は、高度な皮膚がん診断および治療の機会を生み出し、国内の市場全体の成長を促進すると予想されます。

皮膚がん診断および治療業界の概要

皮膚がん診断および治療市場は、世界的にも地域的にも競争が激しいです。市場は、継続的な製品開発と発売に従事する複数の主要企業で構成されています。現在市場を独占している企業としては、アボット社、ファイザー社、サノフィ SA、F.ホフマンラロシュ社、ラボコープ社、サンファーマシューティカルズインダストリーズリミテッドなどが挙げられます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 皮膚がんの発生率の増加

- 皮膚がんに対する意識の高まり

- 広範な調査開発

- 市場抑制要因

- 治療に伴う高額な費用

- 厳格な規制の枠組み

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- がんタイプ別

- 黒色腫

- 非黒色腫

- タイプ別

- 診断

- 皮膚鏡検査

- 生検

- 遺伝子検査

- その他

- 治療

- 化学療法

- 免疫療法

- 標的療法

- その他

- 診断

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東とアフリカ

- GCC

- 南アフリカ

- その他中東およびアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Abbott

- Amgen, Inc.

- Pfizer Inc.

- Bristol-Myers Squibb Company

- F. Hoffmann-La Roche Ltd

- Sanofi

- Merck &Co., Inc.

- Novartis AG

- QIAGEN

- Sun Pharmaceutical Industries Ltd

- Daiichi Sankyo Company, Limited

- Labcorp

- Sirnaomics, Inc.

第7章 市場機会と将来の動向

The Global Skin Cancer Diagnostics and Therapeutics Market size is estimated at USD 13.82 billion in 2024, and is expected to reach USD 17.82 billion by 2029, growing at a CAGR of 5.21% during the forecast period (2024-2029).

The outbreak of the COVID-19 pandemic had a significant impact on the market studied. After the pandemic began, the World Health Organization (WHO) guidelines suggested that chronic disease patients remain indoors. Hence, this hampered the skin cancer diagnostic market. However, the surge in the number of research for studying the impact of the treatment delay on patients with non-melanoma skin cancer (NMSC) or melanoma cancer amid Covid-19 increased. A study, 'The impact of the Covid-19 pandemic on quality of life in skin cancer patients' published in August 2021, mentioned that due to an immunocompromised/-suppressed status and dependent on the underlying tumor disease and burden, cancer patients might be at an increased risk of developing severe Covid-19 disease and requiring treatment in an intensive care setting. Thus, the increased skin cancer incidences during the pandemic increased the diagnostics for the same and created demand for new advanced therapeutics for treatment. Therefore, the pandemic is predicted to have a positive impact on skin cancer diagnostics and therapeutics during the pandemic phase.

Certain factors driving the market growth include increasing incidence of skin cancer, extensive research and development (R&D) pipelines, and rising awareness about skin cancer. For instance, updated in February 2022 by the American Society of Clinical Oncology, an estimated 324,635 people were diagnosed with melanoma in 2020, and in 2020, about 2,400 cases of melanoma were estimated to be diagnosed in people aged 15 to 29 in the United States. Thus, the prevalence of skin cancer among the population is augmenting the growth of the market studied.

Moreover, the increased R&D is predicted to drive the demand for skin cancer therapeutics over the forecast period. For instance, in January 2022, Immunocore, a commercial-stage biotechnology company pioneering the development of a novel class of T cell receptor (TCR) bispecific immunotherapies designed to treat a broad range of diseases, including cancer, received approval from the United States Food and Drug Administration (FDA) for KIMMTRAK (tebentafusp-tebn) for the treatment of HLA-A*02:01-positive adult patients with unresectable or metastatic uveal melanoma (mUM). Additionally, In April 2022, barnaclanic+ launched its Dermatological Diagnosis Unit for the diagnosis and treatment of skin cancer, and the new unit will also have the latest technology on the market in dermatological diagnosis and skin cancer. Thus, this increasing R&D is expected to drive the growth of the studied market.

Therefore, the factors mentioned above are attributed collectively to the studied market growth over the forecast period. However, the excessive cost associated with therapies and stringent regulatory frameworks is expected to hinder the market growth over the forecast period.

Skin Cancer Diagnostics and Therapeutics Market Trends

Non-Melanoma by Cancer Type Segment is Expected to Grow Over the Forecast Period

Non-melanoma skin cancer starts in skin cells, and a cancerous (malignant) growth is a group of cancer cells that can grow into and destroy nearby tissue. It can also spread (metastasize) to other parts of the body, but this is rare with non-melanoma skin cancer. Thus, the increasing cases of non-melanoma are anticipated to drive the growth of the segment.

The research increased during the pandemic to analyze the impact of a pandemic on all skin cancers. A study 'The impact of treatment delay on skin cancer in COVID-19 era: a case-control study' published in December 2021 mentioned in their discussion that the COVID-19 pandemic is associated with an increased skin cancer incidence and more skin cancer operations were performed in the post-lockdown period which was significant only for squamous cell carcinoma (SCC) a type of non-melanoma cancer. Thus, the demand for diagnostics and improved therapeutics increased during the pandemic, marking a positive impact on the non-melanoma segment.

The Skin Cancer Foundation data updated in May 2022 shows that about 90% of non-melanoma skin cancers are associated with exposure to ultraviolet (UV) radiation from the sun. As per the estimates of the Skin cancer Foundation, basal cell carcinoma (BCC) is the most generic form of skin cancer, and an estimated 3.6 million cases of BCC are diagnosed in the United States each year. And the source mentioned above also reported that the annual cost of treating skin cancers in the United States is estimated at USD 8.1 billion, which is about USD 4.8 billion for non-melanoma skin cancers and USD 3.3 billion for melanoma. Thus, the incidence of non-melanoma type skin cancer and associated treatment costs is anticipated to create opportunities for advanced therapeutics and diagnostics in the United States and other counties across the globe. Thereby, it is expected to boost the overall segment growth.

The insights on increased R&D in the segment are also predicted to drive segment growth. For instance, in December 2021, researchers and radiologists at Northampton General Hospital NHS Trust introduced Skin Brachytherapy, a highly targeted radiotherapy technique used to treat certain types of basal cell or squamous cell skin cancers.

Hence, the non-melanoma segment is growing, and it is expected to have significant growth over the forecast period. Hence, driving the growth of the studied market.

North America is Expected to Dominate the Market Over the Forecast Period

North America is expected to dominate the overall skin cancer and therapeutics market throughout the forecast period. The market growth is due to factors like the increasing prevalence and incidence of skin cancers. The United States is expected to be the largest market in this region.

The well-established healthcare infrastructure-focused market players in research and development (R&D) for cancer therapeutics, coupled with recent product launches and the rising burden of skin cancer in the United States, are primary growth factors for the market in the country. For instance, in July 2021, Merck, known as MSD outside the United States and Canada, received approval from the Food and Drug Administration (FDA) for its expanded label for KEYTRUDA, Merck's anti-PD-1 therapy, as monotherapy for the treatment of patients with locally advanced cutaneous squamous cell carcinoma (cSCC) that is not curable by surgery or radiation. Additionally, in May 2022, Labcorp., one of the leading global life sciences companies, launched a new assay for treatment options for melanoma. The new test enables the measurement of Lymphocyte-activation gene 3 (LAG-3) expression levels by immunohistochemistry (IHC) in tumor tissue. LAG-3 is an immune-oncology target with demonstrable clinical benefits in patients with melanoma. The test is available for use in both clinical trials and the care and treatment of patients. These recent developments are expected to drive the skin cancer diagnostics and therapeutics demand in the country, driving the overall market growth in the region.

Furthermore, the Skin Cancer Foundation data updated in May 2022 shows that an estimated 197,700 cases of melanoma will be diagnosed in the United States in 2022. Among those, 97,920 cases will be in situ (noninvasive), confined to the epidermis (the top layer of skin), and 99,780 cases will be invasive, penetrating the epidermis into the skin's second layer (the dermis). Of the invasive cases, 57,180 will be men and 42,600 women. Thus, the incidence and prevalence of skin cancer in the country are demanding the development of advanced diagnostics and therapeutics in the country for treatment, propelling the overall market growth in the region.

Hence, as per the factors mentioned above, the skin cancer cases in the United States is anticipated to create opportunity for advanced skin cancer diagnostics and therapeutics, driving the overall market growth in the country.

Skin Cancer Diagnostics and Therapeutics Industry Overview

The skin cancer diagnostics and therapeutics market is competitive globally and regionally. The market consists of several major players who are engaged in continuous product development and launches. Some companies currently dominating the market are Abbott, Pfizer Inc., Sanofi SA, F. Hoffmann-La Roche Ltd, Labcorp., and sun pharmaceuticals industries limited, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Incidence of Skin Cancer

- 4.2.2 Rising Awareness About Skin Cancer

- 4.2.3 Extensive Research and Developments

- 4.3 Market Restraints

- 4.3.1 High Cost Associated with Therapy

- 4.3.2 Stringent Regulatory Framework

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Cancer Type

- 5.1.1 Melanoma

- 5.1.2 Non-melanoma

- 5.2 By Type

- 5.2.1 Diagnosis

- 5.2.1.1 Dermatoscopy

- 5.2.1.2 Biopsy

- 5.2.1.3 Genetic Tests

- 5.2.1.4 Others

- 5.2.2 Therapeutics

- 5.2.2.1 Chemotherapy

- 5.2.2.2 Immunotherapy

- 5.2.2.3 Targeted Therapy

- 5.2.2.4 Others

- 5.2.1 Diagnosis

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle-East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle-East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Abbott

- 6.1.2 Amgen, Inc.

- 6.1.3 Pfizer Inc.

- 6.1.4 Bristol-Myers Squibb Company

- 6.1.5 F. Hoffmann-La Roche Ltd

- 6.1.6 Sanofi

- 6.1.7 Merck & Co., Inc.

- 6.1.8 Novartis AG

- 6.1.9 QIAGEN

- 6.1.10 Sun Pharmaceutical Industries Ltd

- 6.1.11 Daiichi Sankyo Company, Limited

- 6.1.12 Labcorp

- 6.1.13 Sirnaomics, Inc.