|

市場調査レポート

商品コード

1437991

臨床診断:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Clinical Diagnostics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 臨床診断:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

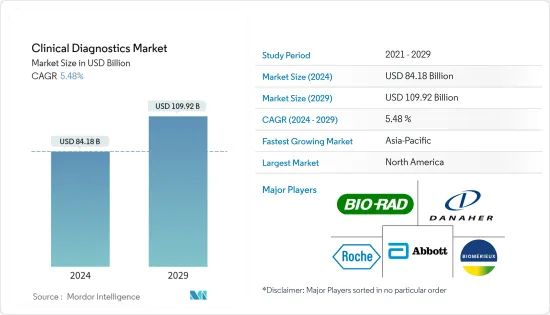

臨床診断市場規模は2024年に841億8,000万米ドルと推定され、2029年までに1,099億2,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に5.48%のCAGRで成長します。

新型コロナウイルス感染症(COVID-19)のパンデミックにより臨床検査が増加し、COVID-19症の疑いのある症例に対応するために需要がさらに急速に増加しました。アトランティック・マンスリー・グループによると、世界的にCOVID-19検査数が大幅に増加し、2020年9月の76万441件から2020年10月までに96万4792件に増加しました。したがって、患者数の絶え間ない増加と政府による資金提供により、検査数は増加しています。政府は、COVID-19検査キットの需要を増大させる要因となり、市場全体の成長を指数関数的に押し上げました。さらに、新型コロナウイルス感染症(COVID-19)ウイルスの変異株の出現により、臨床診断の需要はパンデミック後の期間も一定であり、それによって5年間の市場の成長に貢献するとみられます。

感染症や慢性疾患の発生率の増加と自動化プラットフォームの採用の増加により、市場は成長すると予想されています。 2022年 2月の世界保健機関の報告書によると、毎年約40万人の0~19歳の小児および青少年ががんを発症しています。同情報筋は、最も一般的な種類の小児がんには、白血病、脳腫瘍、リンパ腫、神経芽腫やウィルムス腫瘍などの固形腫瘍が含まれるとも述べています。国際がん調査機関(IARC)が2020年12月に発表した報告書によると、世界のがん患者数は1,930万人に増加しています。したがって、世界中でがんの有病率が高いため、効果的な臨床診断に対する需要があり、それが市場の成長に貢献しています。また、感染症の増加も臨床診断市場の成長に寄与すると予想されます。たとえば、世界保健機関が2021年 11月に発表した報告書では、世界中で100万人以上の性感染症が感染しており、そのほとんどが無症状であると報告しています。また、淋病、クラミジア、トリコモナス症、梅毒という性感染症の4つのうち1つで、毎年推定3億7,400万人が新たに感染していると報告しました。

慢性疾患の増加により、ヘルスケアシステムへの需要も増加しています。したがって、臨床診断は慢性疾患に有益であることが証明されており、疾患の予防、検出、管理に価値があることがわかっています。したがって、慢性疾患の発生率の増加により、市場全体がさらに推進されると予想されます。

臨床診断市場の動向

脂質パネル検査セグメントは、予測期間中に良好な成長を記録すると予想されます

脂質パネルは、体がエネルギー源として使用する脂質、脂肪、脂肪物質を測定する血液検査です。脂質パネルには、総コレステロール、HDLコレステロール、トリグリセリド、LDLコレステロール、コレステロール/HDL比、および非HDLコレステロールの検査が含まれます。

脂質パネルは、血液中の特定の脂質のレベルを測定して心血管疾患のリスクを評価し、心イベントを発症するリスクが高い被験者を特定するための集団のスクリーニングに使用されます。英国心臓財団は2022年 1月に、世界中で影響を受ける最も一般的な心臓疾患は、冠状動脈(虚血性)心疾患(世界有病率2億人と推定)、末梢動脈(血管)疾患(1億1,000万人)、脳卒中(1億人)であると報告しました。心房細動(6,000万人)。このような世界の普及が市場の成長を促進しています。さらに、2021年9月に更新された疾病管理予防センター(CDC)の記事では、米国の40歳以上の約650万人が末梢動脈疾患を患っていると報告されています。さらに、2021年9月に発表されたMDPIジャーナルの調査論文では、末梢動脈疾患(PAD)の世界の有病率は3%~12%と推定されており、アメリカと欧州の約2,700万人が罹患していると報告されています。同情報源は、欧州ではPADの有病率が45歳から55歳の間で約17.8%と推定されているとも報告しています。したがって、末梢血管疾患の負担が大きいことを示すこれらの研究は、市場の成長を後押しすると期待されています。したがって、心血管疾患の有病率と発生率の増加に伴い、初期段階での脂質プロファイル検査の必要性が増加しており、これが脂質パネルセグメントの促進要因となっています。

また、脂質パネル検査用の製品発売数の増加も、予測期間中の調査対象セグメントの成長に寄与すると予想されます。たとえば、2022年 10月に、Boston Heart DiagnosticsはLipoMapの利用可能性を発表しました。この33の脂質、リポタンパク質、およびアポリポタンパク質検査のパネルは、高分解能600 MHz核磁気共鳴によって実行され、市販されている脂質代謝の最も包括的な評価の1つです。

主要企業は、潜在的な機会を活用するために、新しい製品の開発と発売に注力しています。したがって、このセグメントは、前述の要因により、予測期間中に成長すると推定されます。

予測期間中、北米が臨床診断市場を独占すると予想される

北米の臨床診断市場は、高齢者人口の増加、臨床検査の価値に対する患者の意識の高まり、感染症や慢性疾患の患者数の増加によって主に推進されています。

たとえば、2022年に米国がん協会が発表したデータでは、2022年に米国で合計 190万人の新たながん症例が発生すると予想されています。また、疾病管理予防センターは2021年 3月に、1人を超える患者が発生すると発表しました。 7では、2021年には米国成人の15%が慢性腎臓病を患っていると推定されています。このような慢性疾患の有病率が市場の成長を促進すると予想されます。

また、臨床診断の成長を支援するための資金調達活動の増加も、この地域の市場の成長に貢献すると予想されます。たとえば、2020年9月、米国国立衛生研究所は、MatMaCorp、Maxim Biomedical Inc.、MicroGEM Internationalなどを含む9社に1億2,930万米ドルの資金を提供し、 Rapid Acceleration of Diagnostics(RADx)イニシアチブの一環としての新しい一連のCOVID-19検査テクノロジー、医療用医薬品の製造サポートを拡大する計画を発表しました。

これにより、効率的な管理によるより良い治療に対する需要が高まり、北米市場をさらに牽引しています。したがって、感染症および慢性疾患の有病率の増加と臨床検査の価値に対する意識の高まりが、この国の市場の成長を促進すると予想されます。

臨床診断業界の概要

市場は競争が激しく、世界およびローカルのプレーヤーで構成されています。競合情勢には、市場シェアを保持し、よく知られている数社の国際企業と地元企業の分析が含まれています。市場の主な主要企業には、Abbott Laboratories、Bio-Rad Laboratories Inc.、Danaher Corporation、Becton, Dickinson and Company、Qiagen、およびRoche Diagnosticsが含まれます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 増大する感染症および慢性疾患の負担

- 自動化プラットフォームの採用の増加

- 市場抑制要因

- ハイエンドの分子診断を手頃な価格で提供

- 償還シナリオに関連する制限

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション(金額ベースの市場規模)

- 検査別

- 脂質パネル

- 肝臓パネル

- 腎臓パネル

- 全血球計算

- 電解質試験

- 感染症検査

- その他の検査

- 製品別

- 機器

- 試薬

- その他の製品

- エンドユーザー別

- 病院検査室

- 診断検査室

- ポイントオブケア検査

- その他のエンドユーザー

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東とアフリカ

- GCC

- 南アフリカ

- その他中東およびアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Abbott Laboratories

- Becton, Dickinson and Company

- BioMerieux

- Bio-Rad Laboratories Inc.

- Danaher Corporation

- Siemens AG

- Hologic Inc.

- Qiagen NV

- F. Hoffmann-La Roche AG

- Thermo Fisher Scientific

- Quest Diagnostics Inc.

- Sysmex Corporation

- Sonic Healthcare Ltd

- Charles River Laboratories

第7章 市場機会と将来の動向

The Clinical Diagnostics Market size is estimated at USD 84.18 billion in 2024, and is expected to reach USD 109.92 billion by 2029, growing at a CAGR of 5.48% during the forecast period (2024-2029).

Owing to the COVID-19 pandemic, there had been an increase in lab testing, which saw demand grow even more rapidly to keep pace with the suspected cases of COVID-19. According to the Atlantic Monthly Group, there was a tremendous increase globally in COVID-19 tests, rising from 760,441 tests in September 2020 to 964,792 tests by October 2020. Thus, the rising number of tests owing to the constant upsurge in patients and funding by governments were the factors responsible to escalate the demand for COVID-19 test kits and drove the overall market growth exponentially. In addition, the demand for clinical diagnostics is expected to remain constant during the post-pandemic period due to the emergence of a mutant strain of the COVID-19 virus, thereby contributing to the growth of the market over the five years.

The market is expected to grow due to the increasing incidence of infectious as well as chronic diseases and the increasing adoption of automated platforms. According to the World Health Organization report in February 2022, each year, approximately 400,000 children and adolescents of 0-19 years old develop cancer. The same source also mentioned that the most common types of childhood cancers include leukemias, brain cancers, lymphomas, and solid tumors, such as neuroblastomas and Wilms tumors. The report Published by International Agency for Research on Cancer (IARC) in December 2020 that the global cancer burden has risen to 19.3 million cases. and thus, due to the high prevalence of cancer around the world, the demand for effective clinical diagnostics, thereby contributing to the growth of the market. Also, the rising infectious diseases are expected to contribute to the growth of the clinical diagnostics market. For instance, the report published by the World Health Organization in November 2021, reported that more than 1.0 million sexually transmitted infections are acquired globally and most of them are asymptomatic. It also reported that every year there are an estimated 374.0 million new infections with 1 out of 4 sexually transmitted infections: gonorrhea, chlamydia, trichomoniasis, and syphilis.

Owing to the increase in chronic diseases, the demand for healthcare systems is also increasing. Clinical diagnostics have, thus, proven to be beneficial in chronic disease conditions and are found to be valuable for disease prevention, detection, and management. Thus, the increasing incidence of chronic diseases is expected to propel the overall market further.

Clinical Diagnostics Market Trends

Lipid Panel Tests Segment is Expected to Register Good Growth in the Forecast Period

The lipid panel is a blood test that measures the lipids, fats, and fatty substances used as a source of energy by the body. The lipid panel includes tests for total cholesterol, HDL cholesterol, triglycerides, LDL cholesterol, cholesterol/HDL ratio, and non-HDL cholesterol.

A lipid panel measures the level of specific lipids in the blood to assess the risk of cardiovascular disease and is used in screening populations to identify subjects with a high risk of developing a cardiac event. The British Heart Foundation reported in January 2022 that the most common heart conditions affected globally were coronary (ischemic) heart disease (global prevalence estimated at 200 million), peripheral arterial (vascular) disease (110 million), stroke (100 million), and atrial fibrillation (60 million). Such a large prevalence globally is fueling the growth of the market. Furthermore, the Centers for Disease Control and Prevention (CDC) article updated in September 2021 reported that approximately 6.5 million people aged 40 and older in the United States have peripheral arterial disease. Additionally, the MDPI Journal research article published in September 2021 reported that the worldwide prevalence of peripheral arterial disease (PAD) is estimated to be 3%-12%, affecting nearly 27 million people in America and Europe. The same source also reported that in Europe, the prevalence of PAD is estimated at around 17.8% between the ages of 45 and 55. Thus, these studies showing the high burden of peripheral vascular diseases are expected to boost the growth of the market. Hence, with an increase in the prevalence and incidence rate of cardiovascular diseases, there is an increase in the requirement for lipid profile testing at an early stage, which is driving the lipid panel segment.

Also, the increasing number of product launches for lipid panel tests is also expected to contribute to the growth of the studied segment over the forecast period. For instance, in October 2022, Boston Heart Diagnostics announced the availability of LipoMap. This panel of 33 lipid, lipoprotein, and apolipoprotein tests is performed via high-resolution 600 MHz nuclear magnetic resonance and is one of the most comprehensive assessments of lipid metabolism commercially available.

Key companies are focusing on novel product developments and launches to leverage potential opportunities. Hence, the segment is estimated to grow over the forecast period due to the aforementioned factors.

North America is Expected to Dominate the Clinical Diagnostics Market Over the Forecast Period

The market for clinical diagnostics in North America is majorly driven by the increasing geriatric population, rising patient awareness about the value of laboratory tests, and the rising prevalence of infectious and chronic disease patients.

For instance, the data published by the American Cancer Society in 2022 mentioned that a total 1.9 million new cancer cases are expected to occur in the United States in 2022. Also, the Centers for Disease Control and Prevention in March 2021 published that more than 1 in 7, which is 15% of the United States adults are estimated to have chronic Kidney disease in 2021. such prevalence of chronic diseases is expected to drive the growth of the market.

Also, the rising funding activities to support the growth of clinical diagnostics are expected to contribute to the growth of the market in this region. For instance, in September 2020, the National Institutes of Health, US, announced its plan to give funding of USD 129.3 million to nine companies, including MatMaCorp, Maxim Biomedical Inc., MicroGEM International, etc., to scale-up manufacturing support for a new set of COVID-19 testing technologies as part of its Rapid Acceleration of Diagnostics (RADx) initiative.

This has led to a higher demand for better treatment with efficient management, further driving the market in the North America. Hence, the increasing prevalence of infectious and chronic diseases and the growing awareness of the value of laboratory tests are expected to fuel the market growth in the country.

Clinical Diagnostics Industry Overview

The market is highly competitive and consists of global and local players. The competitive landscape includes an analysis of a few international as well as local companies that hold market shares and are well known. The major key players in the market include Abbott Laboratories, Bio-Rad Laboratories Inc., Danaher Corporation, Becton, Dickinson and Company, Qiagen, and Roche Diagnostics.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Burden of Infectious and Chronic Diseases

- 4.2.2 Increasing Adoption of Automated Platforms

- 4.3 Market Restraints

- 4.3.1 Affordability for High-end Molecular Diagnostics

- 4.3.2 Limitations Associated with Reimbursement Scenario

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 By Test

- 5.1.1 Lipid Panel

- 5.1.2 Liver Panel

- 5.1.3 Renal Panel

- 5.1.4 Complete Blood Count

- 5.1.5 Electrolyte Testing

- 5.1.6 Infectious Disease Testing

- 5.1.7 Other Tests

- 5.2 By Product

- 5.2.1 Instruments

- 5.2.2 Reagents

- 5.2.3 Other Products

- 5.3 By End User

- 5.3.1 Hospital Laboratory

- 5.3.2 Diagnostic Laboratory

- 5.3.3 Point-of-care Testing

- 5.3.4 Other End Users

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Abbott Laboratories

- 6.1.2 Becton, Dickinson and Company

- 6.1.3 BioMerieux

- 6.1.4 Bio-Rad Laboratories Inc.

- 6.1.5 Danaher Corporation

- 6.1.6 Siemens AG

- 6.1.7 Hologic Inc.

- 6.1.8 Qiagen NV

- 6.1.9 F. Hoffmann-La Roche AG

- 6.1.10 Thermo Fisher Scientific

- 6.1.11 Quest Diagnostics Inc.

- 6.1.12 Sysmex Corporation

- 6.1.13 Sonic Healthcare Ltd

- 6.1.14 Charles River Laboratories