|

市場調査レポート

商品コード

1641980

継続的デリバリー:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Continuous Delivery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 継続的デリバリー:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

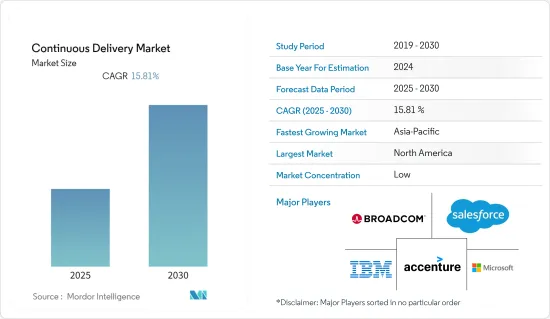

継続的デリバリー市場は予測期間中に15.81%のCAGRで推移すると予想されます。

米国のソフトウェア開発企業であるPerforce Software, Inc.によると、管理者、ソフトウェア開発者、経営幹部の65%が、組織で継続的デリバリーの利用を開始していると報告しています。

主なハイライト

- 継続的デリバリーの市場は、主に人工知能(AI)と機械学習(ML)の成長によって急速に拡大しています。コネクテッドインフラストラクチャの急速な展開とデジタル機器の自律性の高まりにより、AI/MLを搭載した技術はソフトウェア開発プロセスを変革しています。これらの技術は、自己再生システムを可能にし、テストを自動化し、展開結果を予測し、リリーススケジュールを改善し、スマートな監視とアラームを提供します。

- さらに、アジャイル開発アプローチは、ソフトウェアをより迅速かつ柔軟に提供できることから、支持を集めています。継続的デリバリーはアジャイルの原則にうまく合致しており、ソフトウェアを定期的に大幅にリリースするのではなく、少しずつ更新していく。オーストラリアのソフトウェア会社であるAtlassian Corporationによると、米国では少なくとも71%の組織がアジャイルを使用しています。さらに、アジャイル・イニシアチブの成功率は64%であるのに対し、ウォーターフォール・プロジェクトの成功率は49%です。アジャイルプロジェクトの成功率は、ウォーターフォールプロジェクトの成功率の1.5倍です。

- クラウド・コンピューティングとInfrastructure as Codeの採用が増加し、インフラ管理の拡張性と適応性が向上しています。継続的デリバリーによって、企業はクラウドプラットフォームとInfrastructure as Codeツールを使って、クラウド構成でアプリケーションを迅速にデプロイし、管理することができます。継続的デリバリーのCI/CDパイプラインは、企業や組織がソフトウェアを迅速かつ確実に構築、テスト、デプロイできるようにする自動化されたプロセスです。クラウド・インフラストラクチャは、これらのプロセスを実行するための柔軟でスケーラブルなプラットフォームを提供し、企業が需要の変化に適応してリソース使用を最適化することを可能にします。これらのツールは、いくつかの重要な方法で、組織がより大きなビジネス・アジリティを達成するのに役立ちます。

- しかし、オープンソースの継続的デリバリープロジェクトとツールは、商用継続的デリバリーツールのセグメントを支配し、サービス定常デリバリー市場の成長を促進するように設定されています。継続的デリバリー市場は、企業やビジネスがサービスを提供する方法を変更し、より正確で、コストを節約し、生産性を高めるためにビジネスを実行するのに役立ちます。また、より良い、より迅速な意思決定に役立つ多くの有益な情報を生み出します。この情報は、現在のプロセスやオペレーションを最適化したり、いつ、どこで、どのように最高の製品やサービスを提供するかを予測したりすることができます。

- しかし、企業が変化を受け入れず、新しいテクノロジーを既存のプロセスやツールチェーンに統合することに消極的なため、継続的な市場拡大には改善が必要な場合があります。多くの企業は、DevOpsと継続的デリバリーソリューションを使用するために、完全に自動化された技術を採用するためのサポートを必要としています。

継続的デリバリーの市場動向

継続的デリバリー市場におけるクラウド技術の採用の増加

- クラウド上に継続的デリバリーツールを実装することで、高い拡張性、柔軟性、定義された権限による共有機能が提供されます。継続的デリバリーツールを作る人々は、市場の一角を占めるチャンスを活かしています。

- 継続的デリバリーツールはDevOpsの機能を提供し、チームがクラウド上でコラボレーション、開発、テスト、デプロイ、ソフトウェア管理を一箇所で行えるようにします。これにより、エンドユーザーはクラウド上のあらゆるものにアクセスし、新しいアプリケーションを構築することができます。

- ほとんどの企業がデータをクラウドに移行しているため、業界各社はクラウドベースのソリューションを開発し、市場機会を開拓しています。このことが、今後数年間の市場成長を後押しすると思われます。

- グーグルは、継続的デリバリーと統合プラットフォームを完全に管理し、ソフトウェアの迅速かつ大規模なビルド、テスト、デプロイを支援するCloud Buildを発表しました。また、企業はクラウド・コンピューティングへの投資を進めており、これが今後数年間の市場成長を後押しすると予想されます。

- 例えば、今年、Amazon.com Inc.のクラウド・コンピューティング部門であるAmazon Web Services(AWS)は、インドへの大規模な投資計画を発表しました。同社は今年、1兆600億インドルピー(130億米ドル)という途方もない金額を投資する意向です。インドにおけるクラウド・サービスへの需要の高まりが、多額の資金を投入する原動力となっています。今回の投資は、主にAWSのクラウドインフラを全国的に拡大・強化することに重点を置く。

- パブリッククラウドを利用することで、企業は市場の変化に応じて、より迅速かつ効果的に業務を変更し、実行することができます。テクノロジーの使い勝手が向上します。これまで考えられなかったような方法で、驚くほど魅力的な消費者体験を構築することが可能になった。

- クラウドの採用により、人々や組織は行動を修正し、いくつかのビジネスラインは技術的な制約を乗り越えることで物事を成し遂げるようになった。クラウドの動向は、組織がどのように投資を計画し、デジタルビジネスについてどのように意思決定を行い、どのようにベンダーを選択し、どのようなテクノロジーを選択するかに影響を与えます。

- 継続的デリバリー市場における顕著な動向の1つは、リリース管理、計画、リリース自動化ツールであり、DevOpsアプリケーションやツールがパブリッククラウドやプライベートクラウドへのソフトウェアのデプロイを容易にします。例えば、リリース自動化ツールは、スタッフがデプロイ設定のテンプレートを簡単に設定できるようにすることで、時間を節約することができます。

北米が大きな市場シェアを占める

- 米国がクラウドベースのテクノロジーとIoTを早くから採用していることから、北米地域の需要が最も大きく伸びると予測されます。しかし、柔軟性や俊敏性の向上、新しいアプリケーションの実装能力といった利点は不可欠です。

- さらに、北米地域では企業がクラウドベースのアプリケーションを採用しており、米国では中小企業の35%近くがすでにクラウドソリューションを導入していると推定されています。北米では、このチャンスを生かすために、合併、提携、買収が相次いでいます。例えば、SteltixはAutodeployと協業し、継続的デプロイとデリバリーのソフトウェア・スイートを欧州市場に投入しました。

- 機械学習(ML)、人工知能(AI)、予測・処方分析などの新技術の台頭と、これらの新技術を継続的デリバリーモデル、ルール、自己学習、データセット、推論エンジンと統合することで、組織はより円滑に運営できるようになります。

- これらの投資の主な原動力は、これまで非商業的と考えられていたボリュームを活用するための新技術の絶え間ない進化です。こうした投資により、北米では小売、ヘルスケア、通信、製造の各アプリケーションが大きな市場シェアを占めると予想されます。

継続的デリバリー業界の概要

継続的デリバリー市場は細分化されています。新技術の採用に伴い、多くのプレーヤーが技術革新と市場開拓で市場に参入しており、市場競争を激化させています。主なプレーヤーには、IBM Corporation、Microsoft Corporation、Accenture PLC、Salesforce Inc.、Wipro Limited、CA Technologies(Broadcom Company)、XebiaLabs(DIGITAL.AI)、Electric Cloud Inc.(CloudBees Inc.)、Red Hat Inc.、Atlassianなどがあります。

2024年5月継続的デリバリー(CD)の業界標準として認知されているOctopus Deployは、大企業向けのKubernetes CDを合理化することを目的とした機能を発表しました。新しいKubernetesエージェントとコンテナイメージとHelmの外部フィードトリガーのイントロダクションより、Octopus DeployはKubernetesへの大規模デプロイを容易にし、複雑でコストのかかる継続的インテグレーション(CI)スクリプトの必要性を排除します。

2024年3月CircleCIは、リリースオーケストレーション機能を導入することでCI/CDプラットフォームを強化し、開発者がアプリケーションのデプロイをよりコントロールできるようにしました。この追加機能により、開発チームはコードの特定のサブセットを本番環境にデプロイし、コードのパフォーマンスに関するフィードバックを即座に受け取ることができます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- ビジネスプロセス全体の自動化需要の増加

- クラウド技術の採用増加

- 市場抑制要因

- データセキュリティとプライバシーの維持

- 業界バリューチェーン分析

- 業界の魅力- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の業界への影響評価

第5章 市場セグメンテーション

- 展開タイプ別

- クラウド

- オンプレミス

- 組織規模別

- 大企業

- 中小企業

- エンドユーザー業界別

- BFSI

- 通信・IT

- 小売・消費財

- ヘルスケア・ライフサイエンス

- 製造業

- 政府・防衛

- その他のエンドユーザー産業

- 地域別

- 北米

- 欧州

- アジア

- ラテンアメリカ

- 中東・アフリカ

第6章 競合情勢

- 企業プロファイル

- XebiaLabs(DIGITAL.AI)

- Broadcom Inc.(CA Technologie)

- IBM Corporation(Red Hata Inc.)

- Electric Cloud Inc.(CloudBees Inc.)

- Atlassian Corporation PLC

- Microsoft Corporation

- Accenture PLC

- Wipro Limited

- Salesforce Inc.

- Flexagon LLC

- Clarive Software Inc.

第7章 投資分析

第8章 市場の将来

The Continuous Delivery Market is expected to register a CAGR of 15.81% during the forecast period.

According to Perforce Software, Inc., an American software developer, 65% of managers, software developers, and executives report that their organizations have started using continuous delivery.

Key Highlights

- The market for continuous delivery is expanding rapidly, owing primarily to the growth of artificial intelligence (AI) and machine learning (ML). AI/ML-powered technologies are transforming the software development process due to the rapid deployment of connected infrastructure and the rising autonomy of digital devices. These technologies enable self-regeneration systems, automate testing, forecast deployment results, improve release schedules, and provide smart monitoring and alarms.

- Moreover, Agile development approaches have grown in favor due to their ability to deliver software more quickly and flexibly. Continuous delivery aligns well with Agile principles, giving the software minor incremental updates rather than significant, periodic releases. According to Atlassian Corporation, an Australian software company, at least 71% of United States organizations use Agile. Further, Agile initiatives have a 64% success rate, while waterfall projects have a 49% success rate. Agile projects are 1.5X more successful than waterfall projects.

- The rising adoption of cloud computing and Infrastructure as Code has improved scaling and adaptability in infrastructure management. Continuous delivery swiftly allows enterprises to deploy and manage their applications in cloud configurations with cloud platforms and Infrastructure as Code tools. Continuous delivery CI/CD pipelines are automated processes enabling businesses and organizations to build, test, and deploy software quickly and reliably. Cloud infrastructure provides a flexible and scalable platform for running these processes, allowing companies to adapt to changing demands and optimize resource usage. These tools help organizations achieve greater business agility in several vital ways.

- However, open-source continuous delivery projects and tools are set to dominate the commercial straight delivery tools segment, driving the growth of the service steady delivery market. The constant delivery market helps businesses or enterprises change how they deliver services and run their businesses to be more accurate, save money, and be more productive. Also, it creates a lot of helpful information that helps people make better and faster decisions. This information can optimize current processes and operations or predict when, where, and how to offer the best products and services.

- However, the continuous market expansion may need to be improved due to businesses' reluctance to embrace change and integrate new technologies into their existing processes and toolchains. Many companies require support in adopting completely automated techniques for using DevOps and continuous delivery solutions.

Continuous Delivery Market Trends

Increasing Adoption of Cloud Technology in the Continuous Delivery Market

- Implementing continuous delivery tools on the cloud provides high scalability, flexibility, and sharing capabilities with defined authority. The people who make constant delivery tools are taking advantage of the chance to get a piece of the market.

- Continuous delivery tools provide DevOps capabilities that allow teams to collaborate, develop, test, deploy, and manage software on the cloud in one place. This helps end users access everything and build new applications on the cloud.

- Most companies are moving their data to the cloud, so industry players are developing cloud-based solutions to exploit the market opportunity. This is likely to boost market growth over the next few years.

- Google announced Cloud Build, which helps fully manage continuous delivery and integration platforms, helping build, test, and deploy software quickly and at scale. Also, companies are investing in cloud computing, which is expected to help the market grow over the next few years.

- For instance, in the current year, Amazon Web Services (AWS), a cloud computing division of Amazon.com Inc., has announced a significant investment plan for India. The company intends to invest a staggering INR 1.06 trillion (USD 13 billion) in the current year. The increasing demand for cloud services in India drives substantial financial commitment. The investment will primarily focus on expanding and strengthening AWS's cloud infrastructure nationwide.

- With the public cloud, businesses can make changes and run their operations more quickly and effectively in response to changes in the market. It improves the user-friendliness of technology. It has made building incredibly engaging consumer experiences in previously unthinkable ways possible.

- Due to cloud adoption, people and organizations have modified their behavior, and several business lines have gotten things done by getting past technological restrictions. Cloud trends affect how organizations plan to invest, how they make decisions about their digital businesses, how they choose vendors, and what technologies they choose.

- One of the prominent trends in the continuous delivery market is release management, planning, and release automation tools, which make it easier for DevOps applications and tools to deploy software to public or private clouds. Release automation tools, for example, can save time by making it easy for the staff to set up templates for deployment configurations.

North America to Occupy Significant Market Share

- The North American region is projected to have the most significant growth in demand due to the early adoption of cloud-based technologies and IoT by the United States. However, advantages such as increased flexibility and agility and the ability to implement new applications are essential.

- Additionally, companies are adopting cloud-based applications in the North American region, and it was estimated that nearly 35% of SMBs in the United States have already deployed cloud solutions. There have been a series of mergers, collaborations, and acquisitions in North America to take advantage of this opportunity. Steltix, for example, has collaborated with Autodeploy to bring a continuous deployment and delivery software suite to European markets.

- The rise of new technologies like machine learning (ML), artificial intelligence (AI), and predictive and prescriptive analytics, and integrating these new technologies with continuous delivery models, rules, self-learning, data sets, and inference engines will help organizations run more smoothly.

- The primary driver behind these investments has been the continuous evolution of new technologies to utilize previously considered non-commercial volumes. With these investments, North America's retail, healthcare, communications, and manufacturing applications are expected to hold a significant market share.

Continuous Delivery Industry Overview

The continuous delivery market is fragmented. With the adoption of new technologies, many players are entering the market with innovation and development, making the market competitive. Some of the key players include IBM Corporation, Microsoft Corporation, Accenture PLC, Salesforce Inc., Wipro Limited, CA Technologies (Broadcom Company), XebiaLabs (DIGITAL.AI), Electric Cloud Inc. (CloudBees Inc.), Red Hat Inc., and Atlassian, among others.

May 2024: Octopus Deploy, recognized as the industry standard for Continuous Delivery (CD), has unveiled features aimed at streamlining Kubernetes CD for large enterprises. With the introduction of a new Kubernetes agent and external feed triggers for container images and Helm, Octopus Deploy facilitates large-scale deployments to Kubernetes, doing away with the necessity for intricate and costly continuous integration (CI) scripts.

March 2024: CircleCI enhanced its CI/CD platform by introducing a release orchestration feature, empowering developers with greater control over application deployments. This addition allows development teams to deploy a specific subset of code to a live production environment, enabling them to receive immediate feedback on the code's performance.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand For Automation Across Business Processes

- 4.2.2 Increasing Adoption Of Cloud Technology

- 4.3 Market Restraints

- 4.3.1 Maintaining Data Security And Privacy

- 4.4 Industry Value Chain Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Assessment of COVID-19 impact on the industry

5 MARKET SEGMENTATION

- 5.1 Deployment Type

- 5.1.1 Cloud

- 5.1.2 On-premise

- 5.2 Organization Size

- 5.2.1 Large Enterprises

- 5.2.2 Small and Medium-sized Enterprises

- 5.3 End User Industry

- 5.3.1 BFSI

- 5.3.2 Telecom and IT

- 5.3.3 Retail and Consumer Goods

- 5.3.4 Healthcare and Life Sciences

- 5.3.5 Manufacturing

- 5.3.6 Government and Defense

- 5.3.7 Other End User Industries

- 5.4 Geography

- 5.4.1 North America

- 5.4.2 Europe

- 5.4.3 Asia

- 5.4.4 Latin America

- 5.4.5 Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 XebiaLabs (DIGITAL.AI)

- 6.1.2 Broadcom Inc. (CA Technologie)

- 6.1.3 IBM Corporation (Red Hata Inc.)

- 6.1.4 Electric Cloud Inc. (CloudBees Inc.)

- 6.1.5 Atlassian Corporation PLC

- 6.1.6 Microsoft Corporation

- 6.1.7 Accenture PLC

- 6.1.8 Wipro Limited

- 6.1.9 Salesforce Inc.

- 6.1.10 Flexagon LLC

- 6.1.11 Clarive Software Inc.