|

|

市場調査レポート

商品コード

1404421

航空機用塗料:市場シェア分析、産業動向と統計、2024~2029年の成長予測Aircraft Paints - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 航空機用塗料:市場シェア分析、産業動向と統計、2024~2029年の成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 101 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

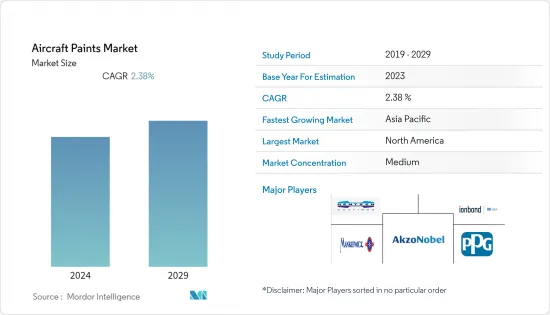

航空機用塗料市場規模は、2024年の13億5,000万米ドルから2029年には15億2,000万米ドルに成長し、予測期間(2024~2029年)のCAGRは2.38%を記録すると予測されています。

民間機と軍用機の納入増加に後押しされた航空市場の成長が、予測期間中の航空機塗料市場の成長を牽引すると予想されます。就航中の古い航空機を改修する必要性も、航空機塗料市場の収益を生み出しています。軽量化と燃費向上を実現する環境に優しい新しい航空機用塗料・コーティング製品の市場開拓は、市場の成長に影響を与えると予想されます。2023年4月、Akzo Nobelは、数年にわたり収集したデータを利用するAerofleet Coatings Managementシステムを開発しました。これは、航空機の再塗装を固定されたスケジュールだけでなく、必要なときだけ行うようにするためのものです。

航空機塗料市場の動向

民間航空機セグメントが最も高い市場シェアを占める

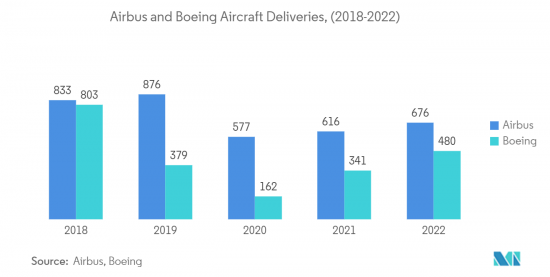

現在、民間航空機セグメントが市場を独占しており、予測期間中も引き続き大きなシェアを占めると予想されます。旅客輸送量はパンデミックの影響から徐々に回復しており、2023年末までにはパンデミック前の水準を上回ると予想されます。回復の背景には、世界の国内旅行の増加があります。国内旅客の増加に伴い、民間航空機の需要は今後数年間で堅調な伸びが見込まれ、それに伴い航空機の電気系統への需要影響も予想されます。航空会社による航空機の調達もまた、航空旅行の増加に対応するために驚異的に増加しています。2022年末までにAirbusは676機、Boeingは480機を納入しました。したがって、予測期間中、民間航空機の継続的な生産と納入が予想されます。民間航空機の生産と納入は、航空機用塗料市場の民間セグメントの成長を牽引すると予想されます。

アジア太平洋は予測期間中に顕著な成長を示すだろう

アジア太平洋の新興諸国では、堅調な経済成長、良好な人口、人口動態が航空旅客輸送を促進しています。同地域では過去10年間に航空旅客輸送量が大幅に増加したが、これは主に同地域の観光地と航空旅行へのアクセスのしやすさに起因するもので、予測期間中もこの傾向は続くと予想されます。

中国は、大きな内需によって世界の民間航空の回復をリードしており、航空会社の財政回復を後押ししています。民間と軍用顧客からの高い需要により、長年にわたって航空産業の主要なハブとなっています。民間航空は、長年にわたって中国の航空産業にとって重要な貢献者です。Boeingによると、中国は国内航空旅客輸送量の増加により航空業界最大の市場となっており、北米地域を上回り、2040年までに4.4%の急成長が見込まれています。

近隣諸国間の緊張に起因する域内諸国の軍事費の増加や、オーストラリアのような国に軍事基地局を配置するために投資する諸外国に伴い、アジア太平洋の軍事航空も増加しています。中国は軍事航空能力を高めています。2021年10月には、世界初の双座ステルス戦闘機である新型ステルス戦闘機J~20が発表されました。こうした発展が、この地域の航空機塗料市場の成長を後押ししています。

航空機用塗料業界概要

航空機用塗料市場は適度に細分化されており、Akzo Nobel NV、PPG Industries Inc.、IHI Ionbond AG、Mankiewicz Gebr &Co.、Hentzen Coatings Inc.などの大手メーカーが占めています。現在、塗料・コーティング業者の多くは北米と欧州に進出しています。各社の世界のプレゼンスが高まることで、各社は他社に対する競争優位性を獲得しやすくなります。また、軽量化、燃費向上、航空機のステルス特性向上、環境に優しい塗料の新興国市場開拓は、企業が市場でより良いポジションを獲得するのに役立つと思われます。2023年4月、AkzoNobelは、AkzoNobelの航空宇宙コーティング事業が開発したデジタル管理システムを通じて、航空会社や運航会社が航空機全体の塗料メンテナンススケジュールを最適化できると発表しました。このような開発は、企業が他社に対して競争上の優位性を獲得するのに役立つと思われます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手・消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- タイプ

- 液体コーティング

- パワーコーティング

- エンドユーザー

- 商業

- 軍用

- 一般航空

- 用途

- 外装

- 内装

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- フランス

- ドイツ

- ロシア

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- ラテンアメリカ

- ブラジル

- その他のラテンアメリカ

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他の中東とアフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- DuPont

- BASF SE

- 3M Co

- PPG Industries Inc.

- Mankiewicz Gebr. & Co.

- Hentzen Coatings, Inc.

- Sherwin-Williams Co

- Akzo Nobel NV

- Mapaero Coatings

- Henkel AG & Company

- IHI Ionbond AG

第7章 市場機会と今後の動向

The aircraft paints market size is expected to grow from USD 1.35 billion in 2024 to USD 1.52 billion by 2029, registering a CAGR of 2.38% during the forecast period (2024-2029).

The growth of the aviation market, fuelled by increasing deliveries of commercial and military aircraft, is expected to drive the growth of the aircraft paints market during the forecast period. The need to refurbish the old aircraft that are in service is also generating revenues for the aircraft paints market. The development of new eco-friendly aircraft painting and coating products that can reduce weight and increase fuel efficiency is expected to impact the growth of the market. In April 2023, AkzoNobel developed the Aerofleet Coatings Management system, which uses data gathered over several years. It is to ensure that aircraft are only repainted when needed, not according to a fixed schedule alone.

Aircraft Paint Market Trends

Commercial Aviation Segment Accounts for the Highest Market Share

Currently, the commercial aircraft segment dominates the market, and it is expected to continue to hold a major share throughout the forecasted period. Passenger traffic is gradually recovering from the impact of the pandemic and is expected to surpass the pre-pandemic levels by the end of 2023. The recovery is attributed to growing domestic travel across the globe. With the growing domestic passengers, the demand for commercial aircraft is expected to witness robust growth in the coming years, with a subsequent demand impact on the aircraft's electrical systems. The procurement of aircraft by the airlines to cater to the increasing air travel also increased tremendously. By the end of 2022, Airbus had delivered 676 aircraft, and Boeing had delivered 480 aircraft. Thus, continuous production and deliveries of commercial aircraft are expected during the forecast period. The production and delivery of commercial aircraft are expected to drive the growth of the commercial segment of the aircraft paints market.

Asia-Pacific Will Showcase Remarkable Growth During the Forecast Period

The robust economic growth, favorable population, and demographic profiles of the populace in developing countries in the Asia-Pacific region are driving air passenger traffic. The region saw a significant increase in air passenger traffic during the past decade, mostly due to the tourist destinations in the region and the ease of access to air travel, which is expected to continue during the forecast period.

China is leading the recovery of global commercial aviation due to great domestic demand, helping the airlines witness financial recovery. It became a major hub for the aviation industry over the years due to high demand from civilian and military customers. Commercial aviation is a key contributor to China's aviation industry over the years. According to Boeing, China is the largest market in aviation due to an increase in domestic air passenger traffic, which surpassed the North American region and is expected to grow rapidly at a rate of 4.4% by 2040.

With the increase in military spending of the countries in the region due to tensions between neighboring countries and with foreign nations investing in arranging military base stations in countries like Australia, military aviation in the Asia-Pacific region is also increasing. China is increasing its military airborne capabilities. A new stealth fighter aircraft, the new version of the J-20, which is the world's first twin-seat stealth fighter aircraft, was unveiled in October of 2021. Developments such as these are boosting the growth of the aircraft paints market in this region.

Aircraft Paint Industry Overview

The aircraft paints market is moderately fragmented, occupied by major manufacturers like Akzo Nobel NV, PPG Industries Inc., IHI Ionbond AG, Mankiewicz Gebr. & Co., and Hentzen Coatings Inc. Currently, most of the paints and coating providers are present in North America and Europe. The increase in the global presence of the companies will help companies to gain a competitive advantage over others. Also, the development of paints that reduce weight, increase fuel efficiency, increase the stealth characteristics of aircraft, and are eco-friendly will help companies attain a better position in the market. In April 2023, AkzoNobel announced that airlines and operators could optimize the paint maintenance schedules for their entire fleets through a digital management system developed by AkzoNobel's Aerospace Coatings business. Developments such as these will help companies to gain a competitive advantage over others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Liquid Coating

- 5.1.2 Power Coating

- 5.2 End-User

- 5.2.1 Commercial

- 5.2.2 Military

- 5.2.3 General Aviation

- 5.3 Application

- 5.3.1 Exterior

- 5.3.2 Interior

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 France

- 5.4.2.3 Germany

- 5.4.2.4 Russia

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Latin America

- 5.4.4.1 Brazil

- 5.4.4.2 Rest of Latin America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Rest of Middle-East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share**

- 6.2 Company Profiles

- 6.2.1 DuPont

- 6.2.2 BASF SE

- 6.2.3 3M Co

- 6.2.4 PPG Industries Inc.

- 6.2.5 Mankiewicz Gebr. & Co.

- 6.2.6 Hentzen Coatings, Inc.

- 6.2.7 Sherwin-Williams Co

- 6.2.8 Akzo Nobel NV

- 6.2.9 Mapaero Coatings

- 6.2.10 Henkel AG & Company

- 6.2.11 IHI Ionbond AG