|

市場調査レポート

商品コード

1651034

再生可能航空燃料:市場シェア分析、産業動向・統計、成長予測(2025~2030年)Renewable Aviation Fuel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 再生可能航空燃料:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年02月03日

発行: Mordor Intelligence

ページ情報: 英文 146 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

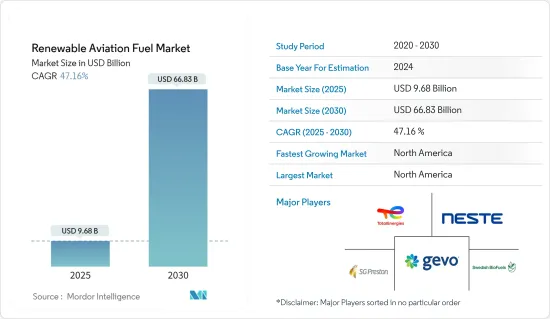

再生可能航空燃料市場規模は2025年に96億8,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは47.16%で、2030年には668億3,000万米ドルに達すると予測されます。

市場は2020年のCOVID-19によってマイナスの影響を受けました。現在、市場はパンデミック以前の水準に達しています。

主要ハイライト

- 長期的には、温室効果ガス排出に関する政府規制の強化、再生可能航空燃料の生産と消費の奨励といった要因が、予測期間中の再生可能航空燃料市場を牽引するとみられます。

- 一方、再生可能航空燃料のコストが高いことが、再生可能航空燃料市場の成長を抑制すると予想されます。

- 東南アジアのような新興地域からの需要の増加は、予測期間中に再生可能航空燃料市場に有利な機会を創出すると予想されます。

- 北米は、米国やカナダのような国からの需要が大半を占め、予測期間中、再生可能航空燃料市場を独占する可能性が高いです。

再生可能航空燃料市場の動向

加水分解エステル・脂肪酸(HEFA)技術が市場を独占する

- 水素化処理エステル・脂肪酸(HEFA)は、一般に水素化植物油(HVO)または水素化処理再生可能ジェット(HRJ)として知られ、動物油または植物油(トリグリセリド)を水素化処理することによって作られる炭化水素航空燃料の一種です。

- 2011年、加水分解エステル・脂肪酸(HEFA)技術は、米国材料検査協会(ASTM)からバイオジェット燃料製造の認定を受けました。HEFAは再生可能燃料製造のために、油脂などの油脂化学原料を使用します。

- 市販されているバイオジェット燃料の大部分はHEFAバイオジェットによるもので、世界各地に商業規模のバイオジェット燃料製造施設があります。しかし、再生可能ディーゼル(HEFA-diesel)もまた、より大きな市場範囲とより高い販売価格を持つプロセスで製造されています。そのため、生産者はHEFAジェットではなくHEFAディーゼルに注目しています。

- さらに、動物油や植物油から作られる炭化水素航空燃料は、バイオエネルギーに含まれます。国際再生可能エネルギー機関(International Renewable Energy Agency)によると、2022年の世界のバイオエネルギー容量は148GWで、その環境に優しい性質から成長が見込まれています。

- 2022年1月、ジョンソン・マッセイは、回収した二酸化炭素(CO2)とグリーン水素をFT技術を使ってサステイナブル航空燃料(SAF)に変換する革新的技術HyCOgenTMを発表しました。再生可能な航空燃料セグメントでのこのような開発は、予測期間中にFT技術の需要を増加させる可能性が高いです。

- さらに、2021年12月、英国運輸省は、チェシャー州に新設される施設の詳細エンジニアリング設計に取り組むと思われるAdvanced Biofuel Solutions(ABSL)に1,500万英ポンドの支援を発表しました。この工場では、ガス化とフィッシャー・トロプシュ(FT)技術により、年間13万3,000トンと推定される廃棄物を、航空燃料にアップグレード可能なバイオ原油に転換します。従って、今後のサステイナブル航空燃料プロジェクトへのこのような投資は、予測期間中にFT技術の需要を増加させる可能性が高いです。

- しかし、HEFAバイオジェット燃料は化石由来のジェット燃料よりもコストが高く、HEFAの潜在的原料もコストが高いです。航空部門を脱炭素化するため、Boeing社などの企業は、航空機における高凝固点HEFA(HEFA+)航空燃料の技術的適合性を検査しています。HEFA+は、植物油や廃脂肪などのバイオ原料から合成される炭化水素です。

- したがって、上記の点から、HEFAセグメントは予測期間中、再生可能航空燃料市場を独占すると予想されます。

市場を独占する北米

- 北米は航空産業と再生可能航空燃料の最大市場の一つです。1978~2022年の間に、米国の航空会社は燃料効率を130%以上改善し、その結果50億トン近くの二酸化炭素を削減しました。Airlines for America(A4A)によると、同国の航空会社はパンデミック前の段階で毎日約2万8,000便を運航しています。北米のほとんどの航空会社は、2020年と2021年に大きな財務上の損失を計上しました。しかし、航空輸送量は予測期間中に回復すると予想されます。さらに、原油価格が急速に上昇しているため、再生可能な航空燃料の需要は予測期間中に伸びると予想されます。

- 米国のバイオエネルギー技術局(BETO)とエネルギー省(DOE)は、エネルギー効率・再生可能エネルギー(EERE)の支援を受けて、再生可能燃料産業の成長を刺激するために、輸送と航空用のサステイナブル国産代替燃料の採用を拡大する努力をしています。

- 北米では、再生可能航空燃料生産に対する主要施策的インセンティブは米国の再生可能燃料基準(RFS)であり、これは再生可能燃料を輸送用燃料に混合して再生可能量義務基準を満たす精製業者や燃料輸入業者にクレジットするものです。

- 2022年1月、環境保護庁(EPA)は、RFSプログラムの下、セルロース系バイオ燃料、先進バイオ燃料、全再生可能燃料の数量要件案を発表しました。この提案では、2022年の再生可能燃料基準量は360億ガロンとされ、前年より30億ガロン以上増加しました。

- さらに、運輸省、エネルギー省、農務省は、この燃料供給を促進するためのロードマップを作成しました。ホワイトハウスは、航空機の温室効果ガス排出量を削減するため、2030年までにサステイナブルジェット燃料生産を年間30億ガロンに拡大する「グランド・チャレンジ」を発表しました。2050年までに、業務用ジェット燃料の消費量を100%満たすだけの燃料を生産することを目指しています。2023年3月、米国政府は、廃棄物をバイオ燃料に転換する科学とインフラを改善し、2050年の目標を支援する機会として、3,450万米ドルを資金提供し、スリル目標を修正しました。

- 北米における既存の燃料施策の枠組みは、将来的に加水分解エステル・脂肪酸(HEFA)燃料の生産を支援することが予想され、それによって同地域のHEFA燃料生産者の機会が増加します。

- 従って、このような要因が予測期間中の市場における北米の優位性を高めると予想されます。

再生可能航空燃料産業概要

再生可能航空燃料市場は適度にセグメント化されています。同市場の主要企業(順不同)には、TotaEnergies SE、Neste Oyj、Swedish Biofuels AB、Gevo Inc.、SG Preston Companyなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 2028年までの市場規模と需要予測(単位:100万米ドル)

- 政府の規制と施策

- 最近の動向と開発

- 市場力学

- 促進要因

- 温室効果ガス排出に関する政府規制の強化

- 再生可能な航空燃料の生産と消費の奨励

- 抑制要因

- 再生可能航空燃料の高コスト

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場セグメンテーション

- 技術

- フィッシャー・トロプシュ(FT)

- 加水分解エステル・脂肪酸(HEFA)

- 合成イソパラフィン(SIP)とアルコール-ジェット(AJT)

- 用途

- 商業

- 防衛

- 地域

- 北米

- 米国

- カナダ

- その他の北米地域

- アジア太平洋

- 中国

- インド

- 日本

- その他のアジア太平洋

- 欧州

- 英国

- フランス

- ドイツ

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- カタール

- その他の中東・アフリカ

- 北米

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- TotalEnergies SE

- Neste Oyj

- Swedish Biofuels AB

- Red Rock Biofuels LLC

- Gevo Inc.

- Honeywell International Inc.

- Fulcrum BioEnergy Inc.

- SG Preston Company

- LanzaTech Inc.

第7章 市場機会と今後の動向

- 東南アジアなど新興地域からの需要増加

The Renewable Aviation Fuel Market size is estimated at USD 9.68 billion in 2025, and is expected to reach USD 66.83 billion by 2030, at a CAGR of 47.16% during the forecast period (2025-2030).

The market was negatively impacted by COVID-19 in 2020. Presently the market has reached pre-pandemic levels.

Key Highlights

- Over the long term, factors such as increased government regulations for greenhouse gas emissions, and encouraging production and consumption of renewable aviation fuel are likely to drive the renewable aviation fuel market during the forecast period.

- On the other hand, high costs of renewable aviation fuel are expected to restrain the growth of renewable aviation fuel market.

- Nevertheless, increasing demand from emerging regions like southeast asia are exoected to create lucrative opportunities for the renewable aviation fuel market in the forecat period.

- North America is likely to dominate the renewable aviation fuel market during the forecast period, with a majority of the demand coming from countries like the United States and Canada.

Renewable Aviation Fuel Market Trends

Hydroprocessed Esters and Fatty Acids (HEFA) Technology to Dominate the Market

- Hydroprocessed Esters and Fatty Acids (HEFA), commonly known as Hydrogenated Vegetable Oil (HVO) or Hydroprocessed Renewable Jet (HRJ), is a type of hydrocarbon aviation fuel made from animal or vegetable oils (triglycerides) by hydroprocessing.

- In 2011, hydro-processed esters and fatty acids (HEFA) technology received certification from the American Society for Testing and Materials (ASTM) for bio-jet fuel production. HEFA uses oleo-chemical feedstock, such as oil and fats, for renewable fuel production.

- A significant share of available commercial volumes of bio-jet fuels comes from HEFA biojet, with several commercial-scale facilities worldwide producing the same. However, renewable diesel (HEFA-diesel) is also made during the process, with a larger market scope and a higher sales price. Thus, producers are focusing on HEFA-diesel instead of HEFA-jet.

- Moreover, hydrocarbon aviation fuel made from animal or vegetable oils comes under bioenergy. According to International Renewable Energy Agency, in 2022, the total global bioenergy capacity accounted for 148 GW, expected to grow due to its environment-friendly nature.

- In January 2022, Johnson Matthey launched an innovative technology, HyCOgenTM, by converting captured carbon dioxide (CO2) and green hydrogen into sustainable aviation fuel (SAF) using FT technology. Such developments in the renewable aviation fuel sector will likely increase demand for FT technology during the forecast period.

- Furthermore, in December 2021, the UK Department for Transport announced support of GBP 15 million to Advanced Biofuel Solutions (ABSL), which was likely to work on a detailed engineering design for a new facility in Cheshire. The plant will be used for gasification and Fischer-Tropsch (FT) technology to convert an estimated 133,000 metric tons of waste a year into a biocrude that can be upgraded to aviation fuel. Thus, such investments in upcoming sustainable aviation fuel projects will likely increase the demand for FT technology during the forecast period.

- However, HEFA biojet fuel costs more than fossil-derived jet fuels, and the potential feedstock for the HEFA is also costly. To decarbonize the aviation sector, companies such as Boeing are testing the technical suitability of high freezing point HEFA (HEFA+) aviation fuel in aircraft. HEFA+ is a synthetic hydrocarbon from bio feedstock, such as vegetable oil or waste fats.

- Therefore, owing to the above points, the HEFA segment is expected to dominate the renewable aviation fuel market during the forecast period.

North America to Dominate the Market

- North America is one of the largest markets for the aviation industry and renewable aviation fuel. Between 1978 and 2022, US airlines improved fuel efficiency by over 130%, which resulted in nearly 5 billion metric tons of carbon dioxide savings. According to the Airlines for America (A4A), the country's airlines operate approximately 28,000 flights daily in the pre-pandemic stage. Most airline companies in North America posted heavy financial losses in 2020 and 2021. However, airline traffic is expected to recover during the forecast period. Further, as crude oil prices are increasing rapidly, the demand for renewable aviation fuel is expected to grow during the forecast period.

- The Bio-Energy Technologies Office (BETO) of the United States and the Department of Energy (DOE), supported by Energy Efficiency and Renewable Energy (EERE), are making efforts to expand the adoption of sustainable, domestically produced alternative fuels for transportation and aviation to stimulate the growth of the renewable fuel industry.

- In North America, the primary policy incentive for renewable aviation fuel production is the US Renewable Fuel Standard (RFS), which credits refiners and fuel importers who blend renewable fuel into transportation fuel to meet Renewable Volume Obligation standards.

- In January 2022, the Environmental Protection Agency (EPA) issued proposed volume requirements, under the RFS program, for cellulosic biofuel, advanced biofuel, and total renewable fuel. Under this proposal, the renewable fuel standard 2022 was set at 36 billion gallons, an increment of over 3 billion gallons over the previous year.

- Moreover, The Departments of Transportation, Energy, and Agriculture developed a road map to guide their efforts to boost this fuel supply. The White House issued a "Grand Challenge" to expand sustainable jet fuel production to 3 billion gallons per year by 2030 to reduce aviation greenhouse gas emissions. It aims to create enough fuel by 2050 to meet 100% commercial jet fuel consumption. In March 2023, the U.S. government revised thr goals by funding USD 34.5 million as an opportunity to improve the science and infrastructure for converting waste into biofuels and help support the 2050 goal.

- The existing framework of fuel policies in North America is expected to support hydro-processed esters and fatty acids (HEFA) fuel production in the future, thereby increasing the opportunities for HEFA fuel producers in the region.

- Therefore, such factors are expected to boost the dominance of North America in the market during the forecast period.

Renewable Aviation Fuel Industry Overview

The renewable aviation fuel market is moderately fragmented. Some of the major players in the market (in no particular order) include TotaEnergies SE, Neste Oyj, Swedish Biofuels AB, Gevo Inc., and SG Preston Company.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD million, till 2028

- 4.3 Government Policies and Regulations

- 4.4 Recent Trends and Developments

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increased Government Regulations for Greenhouse Gas Emissions

- 4.5.1.2 Encouraging Production and Consumption of Renewable Aviation Fuel

- 4.5.2 Restraints

- 4.5.2.1 The High Costs of Renewable Aviation Fuel

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Technology

- 5.1.1 Fischer-Tropsch (FT)

- 5.1.2 Hydroprocessed Esters and Fatty Acids (HEFA)

- 5.1.3 Synthesisized Iso-Paraffinic (SIP) and Alcohol-to-Jet (AJT)

- 5.2 Application

- 5.2.1 Commercial

- 5.2.2 Defense

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States of America

- 5.3.1.2 Canada

- 5.3.1.3 Rest of the North America

- 5.3.2 Asia-Pacific

- 5.3.2.1 China

- 5.3.2.2 India

- 5.3.2.3 Japan

- 5.3.2.4 Rest of the Asia-Pacific

- 5.3.3 Europe

- 5.3.3.1 United Kingdom

- 5.3.3.2 France

- 5.3.3.3 Germany

- 5.3.3.4 Rest of the Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of the South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Qatar

- 5.3.5.4 Rest of the Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 TotalEnergies SE

- 6.3.2 Neste Oyj

- 6.3.3 Swedish Biofuels AB

- 6.3.4 Red Rock Biofuels LLC

- 6.3.5 Gevo Inc.

- 6.3.6 Honeywell International Inc.

- 6.3.7 Fulcrum BioEnergy Inc.

- 6.3.8 SG Preston Company

- 6.3.9 LanzaTech Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Demand from Emerging Regions like Southeast Asia