|

市場調査レポート

商品コード

1433492

発泡剤- 市場シェア分析、産業動向と統計、成長予測(2024年~2029年)Blowing Agents - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 発泡剤- 市場シェア分析、産業動向と統計、成長予測(2024年~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

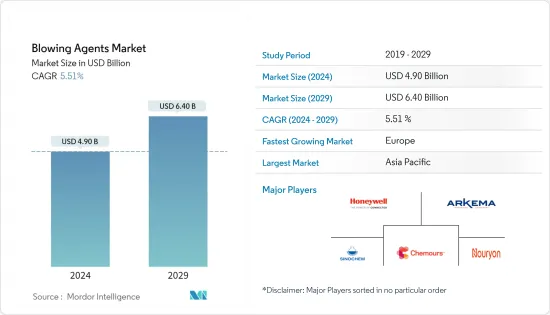

発泡剤市場規模は、2024年に49億米ドルと推定され、2029年までに64億米ドルに達すると予測されており、予測期間(2024年から2029年)中に5.51%のCAGRで成長します。

調査対象の市場を牽引する主な要因は、建物、自動車、家電製品向けのポリマー断熱フォームの需要の増加です。発泡剤に関する厳しい環境規制は、調査対象の市場の成長を妨げると予想されます。

主なハイライト

- オゾン層破壊係数(ODP)がゼロで地球温暖化係数(GWP)が低い発泡剤に対する高い需要は、将来的にはチャンスとなる可能性があります。

- 収益の面では、北米が予測期間中に調査された市場を独占していました。量の面では、アジア太平洋が世界市場を独占しました。

発泡剤市場動向

建築・建設業界からの需要の増加

- 発泡剤は、VOCを含まず、オゾン層を破壊せず、地球温暖化係数が低く、エネルギー消費量が少ないため、環境的に許容され、建築や建設に使用されています。より均一なコンポーネントの作成に役立ち、その結果、より優れた、より緊密な断熱、より高いエネルギー効率、および制限されたエネルギー消費が実現します。

- 発泡剤は、ブロックパイプや屋根の断熱材、ドア、外装材などの建物の断熱材や、基礎を必要とする構造物の成分として使用されます。窓やドアのシーリング材としても使用されます。

- これらは主にポリウレタンフォームに使用されており、熱の損失を防ぎ、寒冷地でも温度を維持し、長距離加熱時の凍結や亀裂を防ぐためにパイプで頻繁に使用されています。

- これらはフェノールフォームにも使用されますが、用途は限られています。フェノールフォームは主に、屋根、壁空洞、および床断熱材の断熱バリアとして機能するパネルに使用されます。世界中で建設活動が増加しているため、発泡剤市場は大幅に拡大すると予想されます。

- アジア太平洋地域は建築・建設部門を支配しており、インド、中国、その他の東南アジア諸国が市場の成長を大きく牽引しています。

- 前述のようなプラスの要因は、予測期間を通じて市場の成長を促進すると予想されます。

中国がアジア太平洋市場を独占へ

- グループIのメンバーである中国は、2024年までにHFCの生産と使用を合意されたベースラインレベルで凍結すると予想されており、2029年までに凍結レベルより10%低い段階で段階的に生産と使用を段階的に削減する予定です。

- CFC-11の使用はオゾン層破壊の影響により2010年に国際的に禁止されたが、硬質ポリウレタンフォーム断熱分野での発泡剤としてのCFC-11の違法な製造および使用を証明する証拠が発見されています。英国に本拠を置くNGOである環境調査局が実施した現地調査によると、中国の大気中のCFC-11濃度は予想を大幅に上回っており、CFC-11の有害性が証明されています。

- 禁止されているCFCおよびHCFC(使用は規制されており、2040年までに段階的に廃止される予定)とは別に、中国はプレブレンドCP(シクロペンタン)、HFOブレンド、水などの代替発泡剤を使用しています。

- 中国には世界最大の建設産業があります。しかし、中国政府がサービス主導型経済への移行を目指しているため、この業界の成長率はますます緩やかになってきています。

- 中国は世界で第2位の包装産業を有しており、カスタマイズされた包装の台頭、電子レンジ用食品、スナック食品、冷凍食品などの需要の増加により、予測期間中に一貫した成長が見込まれています。

- 中国には世界最大の繊維・アパレル産業があり、同国経済の重要なプレーヤーでもあります。しかし、米国との貿易戦争や市場の成熟により、米国のアパレル輸出市場における同国のシェアは低下しています。

- したがって、前述の要因は、予測期間中の中国の発泡剤の需要に影響を与える可能性があります。

発泡剤業界の概要

発泡剤の世界市場は細分化されています。市場には国際的なプレーヤーだけでなく、地元のプレーヤーもたくさんいます。主要企業には、Honeywell International Inc.、The Chemours Company、Arkema、Sinochem Group、Nouryonなどが含まれます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 建築物、自動車、家電製品向けポリマー断熱フォームの需要増加

- ポリウレタンフォーム製造における発泡剤需要の増加

- 抑制要因

- 発泡剤に関する厳しい環境規制

- COVID-19の影響

- その他の阻害要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

- 規制と政策

第5章 市場セグメンテーション

- 製品タイプ

- ハイドロクロロフルオロカーボン(HCFC)

- ハイドロフルオロカーボン(HFC)

- 炭化水素(HC)

- ハイドロフルオロオレフィン(HFO)

- その他の製品タイプ

- フォームタイプ

- ポリウレタンフォーム

- ポリスチレンフォーム

- フェノールフォーム

- ポリプロピレンフォーム

- ポリエチレンフォーム

- その他のフォーム

- 用途

- 建築・建設

- 自動車

- 寝具・家具

- 家電製品

- 包装

- その他の用途

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- その他北米

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東とアフリカ

- アジア太平洋

第6章 競合情勢

- 合併、買収、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- A-Gas

- Americhem

- Arkema

- Form Supplies Inc.(FSI)

- Harp International Ltd

- HCS Group GmbH

- Honeywell International Inc.

- Huntsman International LLC

- Lanxess

- Nouryon

- Sinochem Group Co. Ltd

- Solvay

- The Chemours Company

- The Linde Group

- Zeon Corporation

第7章 市場機会と今後の動向

- オゾン層破壊係数(ODP)ゼロで地球温暖化係数(GWP)の低い発泡剤への高い需要

- 発泡包装用ポリスチレン押出シートの高い消費量

The Blowing Agents Market size is estimated at USD 4.90 billion in 2024, and is expected to reach USD 6.40 billion by 2029, growing at a CAGR of 5.51% during the forecast period (2024-2029).

Major factors driving the market studied is rise in demand for polymeric insulation foams for buildings, automotive, and appliances. stringent environmental regulations regarding blowing agents is expected to hinder the growth of the market studied.

Key Highlights

- High Demand for Zero Ozone Depletion Potential (ODP) and Low Global Warming Potential (GWP) Blowing Agents is likely to act as an opportunity in the future.

- In terms of revenue, North America dominated the market studied during the forecast period. In terms of volume, Asia-Pacific dominated the global market.

Blowing Agents Market Trends

Increasing Demand from the Building and Construction Industry

- Owing to their non-VOC, non-ozone depleting, low global warming potential, and reduced energy consumption, blowing agents are environmentally acceptable, and are thus, used in building and construction. They help to create better uniform components, resulting in better, tighter insulation, higher energy efficiency, and limited energy consumption.

- Blowing agents are used as a component in building insulation, such as block pipe and roof insulation, doors, sheathing, and in structures that require foundation. They are also used as sealants for windows and doors.

- They are majorly used in polyurethane foams that have high utilization in pipes to prevent loss of heat and to maintain temperatures even during cold climates, to avoid freezing or cracking for long-distance heating.

- They are also used in phenolic foams, but with limited usage. Phenolic foams are majorly used in panels to act as insulating barriers in roofing, wall cavities, and floor insulation. The increasing construction activities worldwide is expected to significantly boost the blowing agents market.

- The Asia-Pacific region dominates the building and construction sector, with India, China, and various other South East Asian countries driving the market growth significantly.

- The positive factors like the aforementioned ones are expected to drive the market growth through the forecast period.

China to Dominate the Asia-Pacific Market

- As a Group I member, China is expected to freeze HFC production and use at agreed baseline levels, by or before 2024, and is expected to phase down the production and use, beginning with a 10% phasedown below freeze levels, by 2029.

- Though the usage of CFC-11 was banned internationally in 2010, owing to the ozone depletion effects of the substance, evidence has been found proving the illegal production and usage of CFC-11 as a blowing agent in the rigid polyurethane foam insulation sector. According to a field study carried out by the Environmental Investigative Agency, a UK-based NGO, the atmospheric levels of CFC-11 in China are significantly greater than expected, proving the harmful nature of CFC-11.

- Apart from the banned CFCs and HCFCs (whose usage is regulated and is expected to phase out by 2040), China has been using alternative blowing agents, like preblended CP (cyclopentane), HFO blends, and water.

- China has the world's largest construction industry. However, the growth rate of the industry has become increasingly modest, as the Chinese government is looking to shift toward a services-led economy.

- China has the second-largest packaging industry in the world and is expected to witness a consistent growth during the forecast period, owing to the rise of customized packaging, increased demand for microwave food, snack foods, and frozen foods, among others.

- China has the world's largest textile and apparel industry, which is also a key player for the country's economy. However, there has been a drop in the market share occupied by the country in the global apparel export market, owing to the trade war with the United States and maturation of the market.

- Hence, the aforementioned factors are likely to affect the demand for blowing agents in China during the forecast period.

Blowing Agents Industry Overview

The global market for blowing agents is fragmented. There are many local players in the market along with international players. The major companies include Honeywell International Inc., The Chemours Company, Arkema, Sinochem Group Co. Ltd, and Nouryon, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Rise in Demand for Polymeric Insulation Foams for Buildings, Automotive, and Appliances

- 4.1.2 Increasing Demand for Foam Blowing Agents in the Manufacturing of Polyurethane Foams

- 4.2 Restraints

- 4.2.1 Stringent Environmental Regulations Regarding Blowing Agents

- 4.2.2 Impact of COVID-19

- 4.2.3 Other Restraints

- 4.3 Industry Value-Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Policies and Regulations

5 MARKET SEGMENTATION

- 5.1 Product Type

- 5.1.1 Hydrochlorofluorocarbons (HCFCs)

- 5.1.2 Hydrofluorocarbons (HFCs)

- 5.1.3 Hydrocarbons (HCs)

- 5.1.4 Hydrofluoroolefin (HFO)

- 5.1.5 Other Product Types

- 5.2 Foam Type

- 5.2.1 Polyurethane Foam

- 5.2.2 Polystyrene Foam

- 5.2.3 Phenolic Foam

- 5.2.4 Polypropylene Foam

- 5.2.5 Polyethylene Foam

- 5.2.6 Other Foam Types

- 5.3 Application

- 5.3.1 Building and Construction

- 5.3.2 Automotive

- 5.3.3 Bedding and Furniture

- 5.3.4 Appliances

- 5.3.5 Packaging

- 5.3.6 Other Applications

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Rest of North America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers, Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 A-Gas

- 6.4.2 Americhem

- 6.4.3 Arkema

- 6.4.4 Form Supplies Inc. (FSI)

- 6.4.5 Harp International Ltd

- 6.4.6 HCS Group GmbH

- 6.4.7 Honeywell International Inc.

- 6.4.8 Huntsman International LLC

- 6.4.9 Lanxess

- 6.4.10 Nouryon

- 6.4.11 Sinochem Group Co. Ltd

- 6.4.12 Solvay

- 6.4.13 The Chemours Company

- 6.4.14 The Linde Group

- 6.4.15 Zeon Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 High Demand for Zero Ozone Depletion Potential (ODP) and Low Global Warming Potential (GWP) Blowing Agents

- 7.2 High Consumption of Extruded Sheets of Polystyrene for Packaging Foam