膝関節置換術:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)

Knee Replacement - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 113 Pages

- 納期

- 2~3営業日

- 商品コード

- 1850246

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

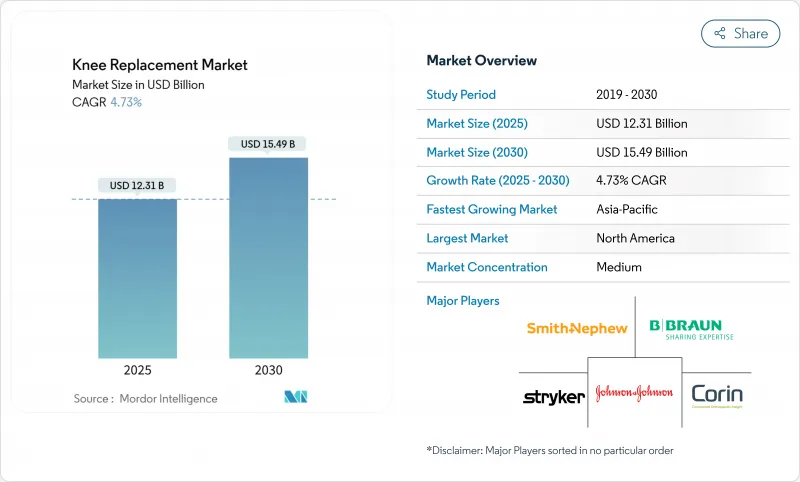

膝関節置換術市場規模は2025年に123億1,000万米ドルと推定・予測され、予測期間(2025-2030年)のCAGRは4.73%で、2030年には154億9,000万米ドルに達すると予測されます。

65歳以上人口の急増、肥満の蔓延、インプラントの設計と手術手技の着実な改善など、さまざまな要因が重なりあっての成長です。技術導入により、この分野はデータガイドに基づく精密さへとシフトしており、ロボットプラットフォームが大規模病院と外来手術センターの両方で支持を集めています。並行して行われる診療報酬改革では、即日退院のプロトコルに報酬が与えられるようになり、入院患者と外来患者の間の競争が激化しています。メーカー各社は、製品ラインナップの拡充、プラットフォームの買収、持続可能性への取り組みの強化などを通じて対応しており、こうした動きは、あらゆる主要地域における外科医の嗜好や購買意思決定に影響を与えています。

世界の膝関節置換術市場の動向と洞察

高齢化と肥満人口の増加

平均寿命の延びは、座りがちなライフスタイルと相まって変形性膝関節症の発症率を高め、膝関節置換術の需要を加速させています。膝関節置換術の利用は65~74歳の集団で最も多いが、75~84歳の集団が最も急速な伸びを記録しており、高所得市場では女性が男性の9倍の割合で膝関節置換術を受けています。インプラントの耐久性が向上しているため、50代前半の患者への介入も可能になり、対応可能な患者層が拡大し、再手術の負担がさらに将来へとシフトしています。

ロボット支援下全置換術の急速な普及膝関節置換術

現在、臨床研究において、ロボット支援は靭帯のバランシングをより強固にし、アライメントの異常値をより少なくし、早期段階の患者報告アウトカムスコアをより高くしています。Stryker社のMakoプラットフォームは、累計150万手技を突破し、調査対象となった外科医の95%が術中の信頼性の向上を挙げています。ジョンソン・エンド・ジョンソンのVELYSシステムは、2024年にCTベースのプランニングを必要としない単顆型膝関節に対するFDA認可を取得し、既存の優位性に課題し、ワークフローの統合と費用対効果を中心とした技術競争に拍車をかけています。

中国とインドにおける価格キャップ規制

中国の数量ベースの調達枠組みにより、膝関節インプラントの平均価格が50%引き下げられ、入院患者の総削減額の93.21%を膝関節インプラントが占めました。インドのNational Pharmaceutical Pricing Authorityは、研究開発費に見合わない上限を設定し、貿易摩擦を引き起こしています。メーカー各社は、現在ではポートフォリオをプレミアム価格帯とバリュー価格帯にセグメント化し、義務化されたマークダウンからイノベーション予算を保護しています。

セグメント分析

市場セグメンテーションは、2024年の市場シェア71.24%を占めると同時に、2030年までのCAGR 5.83%で成長をリードしています。この現象は、さまざまな病態に対応できる術式の多様性と、インプラントの設計や手術手技における絶え間ない技術革新を反映しています。ジョンソン・エンド・ジョンソン社のVELYSシステムが2024年に単顆置換術のFDA認可を取得し、骨温存術式がこれまで十分に活用されてこなかったことに対処しています。

膝蓋大腿骨置換術は、ニッチではあるが成長分野であり、特に膝前面に痛みを持つ若年患者を対象としています。一方、再置換術や複雑な膝関節置換術手術は、プライマリー・インプラントの設置ベースが高齢化するにつれて需要が増加しています。再置換術の分野では、骨量管理やコンポーネントの互換性の問題など、独自の課題に直面しており、モジュラー・インプラント・システムやカスタム3Dプリント・ソリューションの技術革新が進んでいます。ジマー・バイオメットのオックスフォード・セメントレス部分膝は、米国で唯一のセメントレス部分膝インプラントとして2024年にFDAから承認され、10年後のインプラント生存率は94.1%で、部分膝の平均的な性能指標を大幅に上回っています。

地域別分析

北米は2024年の売上高が41.11%で膝関節置換術市場をリードしており、これは米国における年間手術件数79万件以上、強力な技術導入、強固な民間負担制度が牽引しています。カナダの公費負担制度は待ち時間の制約をもたらし、米国やメキシコの医療施設への受診を促しています。メキシコはその流れを利用し、米国で訓練された外科医やロボット工学をバンドルしたパッケージを販売する民間の整形外科機関を拡大しています。入院患者の在院日数短縮を求める支払者の圧力は、バリュー・ベース購買の焦点を鮮明にしています。

欧州は、成熟しつつも異質なプロファイルを示しています。ドイツは最も手術件数が多いが、フランスでは診療報酬が引き下げられ、インプラントの価格が25%引き下げられました。英国では、NHSの待機患者数が活動目標達成のために民間病院との契約に拍車をかけています。南欧諸国は、欧州投資銀行の資金援助を受けて、手術室を近代化する一方、コスト抑制のためにインプラントの処方箋を縮小しています。東欧市場は、より低いベースラインからスタートします。EUの結束基金と技能移転パートナーシップは、整形外科病棟のアップグレードを加速させる。スカンジナビアで先駆けて導入されたカーボンフットプリント開示などの環境調達基準は、国境を越えた支持を集めており、ベンダー資格基準を再構築する可能性があります。

アジア太平洋地域はCAGR 15.08%と最も高い成長率を示しており、2030年までに世界の膝関節置換術市場に変革をもたらすと考えられています。中国の数量ベースの調達は機器価格を半減させたが、手技の普及を妨げるものではありません。日本は年間8万2,304件の一次膝関節置換術を登録し、セラミックオンセラミックベアリングは金属イオンを嫌う文化を反映しています。韓国の手術率は、国民保険と低侵襲手術の積極的なマーケティングに支えられ、過去10年間で407%の伸びを示しました。インドは、急増する需要と価格上限のバランスがとれており、技術革新予算には制約があるもの、国内のインプラント製造を刺激しています。オーストラリアでは、男性10万人当たり83.9人という傷害発生率が、スポーツに関連した膝の外傷の増加を示しており、政府のコスト抑制が強化される中でも、パイプラインの需要に拍車をかけています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 高齢化と肥満人口の増加

- ロボット支援の膝関節全置換術(TKR)の急速な導入

- 外来診療(ASC)償還プログラムの拡大

- 新興市場における人工関節置換術の能力拡大

- カスタマイズされた3Dプリントインプラント技術

- 軍用グレードのポリエチレンの長寿命化におけるブレークスルー

- 市場抑制要因

- 中国とインドにおける価格上限規制

- 再手術の経済的負担

- インプラント金属のカーボンフットプリントに関する環境調査

- カスタムインプラントの知的財産に関する法的リスク

- テクノロジーの展望

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力/消費者

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 製品別

- 膝関節全置換術

- 膝関節部分置換術

- 膝蓋大腿骨置換術

- 再置換/複雑膝関節置換術

- 外科技術別

- マニュアル

- ロボット支援

- 患者固有の機器(PSI)

- コンピューターナビゲーション

- エンドユーザー別

- 病院

- 外来手術センター(ASC)

- 整形外科専門クリニック

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 市場集中度

- 市場シェア分析

- 企業プロファイル

- Zimmer Biomet

- Stryker Corporation

- Johnson & Johnson(DePuy Synthes)

- Smith & Nephew plc

- B. Braun(Aesculap)

- Exactech Inc.

- Medacta Group

- MicroPort Orthopedics

- Medtronic plc

- Corin Group

- Conformis Inc.

- THINK Surgical

- Waldemar Link GmbH

- DJO Global(Enovis)

- United Orthopedic Corp.

- LimaCorporate

- Amplitude SAS

- Auxein Medical

- Arthrex Inc.

- SurgTech Inc.

第7章 市場機会と将来の展望

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 113 Pages

- 納期

- 2~3営業日