|

市場調査レポート

商品コード

1755274

セメントレス部分膝インプラント市場機会、成長促進要因、産業動向分析、2025~2034年予測Cementless Partial Knee Implants Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| セメントレス部分膝インプラント市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年05月27日

発行: Global Market Insights Inc.

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

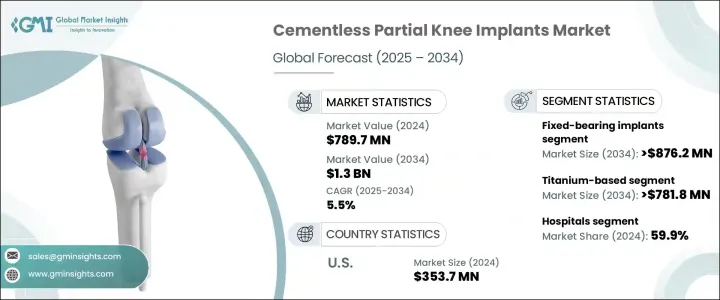

世界のセメントレス部分膝インプラント市場は、2024年には7億8,970万米ドルと評価され、CAGR 5.5%で成長し、2034年には13億米ドルに達すると推定されています。

この成長の主な要因としては、膝の再手術の増加につながる感染率の上昇、変形性関節症や関節リウマチの有病率の増加、低侵襲手術への嗜好の高まりなどが挙げられます。変形性関節症を患う高齢者の増加と、より効果的で侵襲性の低い手術オプションに対する需要は、この市場の重要な促進要因です。単コンパートメント人工膝関節置換術(UKA)で使用されるセメントレス部分膝インプラントは、膝関節の患部のみを置換し、より自然な骨と靭帯を保存します。

これらのインプラントは骨セメントを必要とせず、代わりに生物学的固定を促進します。この方法は、インプラント周囲の骨組織の自然な成長を促し、インプラントと骨との一体化をより強固で耐久性のあるものにします。骨セメントを使用しないことで、時間の経過とともにインプラントがゆるむリスクが最小限に抑えられるだけでなく、セメントに関連した感染症や炎症などの合併症の可能性も低くなります。さらに、生物学的固定はインプラントの全体的な安定性を高め、インプラントの寿命を延ばし、患者の長期予後を改善する可能性があります。その結果、セメントレスインプラントは、より自然な治癒プロセスを提供し、再置換の必要性が少なくなる可能性があるため、整形外科手術においてますます好まれる選択肢となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 7億8,970万米ドル |

| 予測金額 | 13億米ドル |

| CAGR | 5.5% |

固定式ベアリングインプラント分野は、CAGR 5.3%で成長し、2034年には8億7,620万米ドルに達すると予想されています。これらのインプラントは、可動式ベアリングシステムよりも機械的にシンプルで故障が少ないため、外科医の間で人気が高いです。これらのインプラントは、需要の少ない患者において、10年後の長期生存率が90%を超えています。さらに、可動式ベアリングシステムは一般的に高価で複雑であるため、その受容と普及には限界があります。その結果、固定式ベアリングシステムが多くの症例で好まれ、その採用を加速し、市場支配に貢献しています。

チタンベースのセグメントは5.4%の成長率を経験し、2034年までに7億8,180万米ドルに達すると予測されています。チタンの生体適合性は、セメントレスインプラントの成功に不可欠なオッセオインテグレーションを促進するため、セメントレスインプラントに理想的です。チタンインプラントは、コバルトクロム合金と比較して、骨組織との接着性が良く、緩みに対する抵抗力が大きいため、安定性と寿命が向上します。チタン合金の軽量な性質は、その強度と相まって、術後に大きな可動性を必要とする、より若く活動的な患者に特に適しています。さらに、チタンは金属過敏症の患者にとって理想的であり、個別化された人工膝関節の需要をさらに促進しています。

米国のセメントレス部分膝インプラントの市場規模は2024年に3億5,370万米ドル。米国では高齢化が急速に進んでおり、人工膝関節置換術の需要が高まっています。変形性膝関節症、特に内側一顆変形性膝関節症は、部分的人工膝関節置換術の必要性を高めている主な疾患の1つです。さらに米国では、麻酔時間の短縮、出血量の最小化、回復の早さなどの利点から、外来手術センターを中心に外来整形外科手術が増加しています。さらに、米国では償還制度が充実しており、民間保険会社もメディケアも、適切な患者には人工膝関節全置換術よりも部分膝関節置換術の方が費用対効果が高いと認識するようになっています。

セメントレス部分膝インプラント世界市場の主要企業には、Stryker、Medacta、Amplitude Surgical、Smith+Nephew、Waldemar Link、GRUPPO BIOIMPIANTI、ZIMMER BIOMET、Lepine、Just Medical、Medactaなどがあります。市場での存在感を高めるため、セメントレス部分膝インプラント業界の企業はいくつかの戦略に注力しています。インプラントの生体適合性やオッセオインテグレーション特性の向上など、インプラントのデザインや機能性を改善するための継続的な技術革新に投資しています。ヘルスケアプロバイダー、クリニック、病院との提携も、製品リーチを拡大し、より高い採用率を確保するために行われています。さらに、企業は地域拡大、特に整形外科手術の需要が増加している新興市場の拡大に注力しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 感染率の上昇が膝関節再置換手術の増加に寄与している

- 変形性関節症および関節リウマチの有病率の増加

- 低侵襲手術への関心の高まり

- セメントレス固定法の技術的進歩

- 業界の潜在的リスク&課題

- セメントレス膝インプラントに伴う高コスト

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 償還シナリオ

- ギャップ分析

- ポーター分析

- PESTEL分析

- 将来の市場動向

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:インプラントの種類別、2021年~2034年

- 主要動向

- 固定式ベアリングインプラント

- 可動式ベアリングインプラント

- 内側ピボットインプラント

- その他のインプラントの種類

第6章 市場推計・予測:材料別、2021年~2034年

- 主要動向

- チタンベース

- コバルトクロム合金

- ポリエチレン部品

- その他の材料

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 整形外科センター

- その他の用途

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- amplitude SURGICAL

- GRUPPO BIOIMPIANTI

- JUST MEDICAL

- lepine

- Medacta

- Smith+Nephew

- Stryker

- Waldemar Link

- ZIMMER BIOMET

The Global Cementless Partial Knee Implants Market was valued at USD 789.7 million in 2024 and is estimated to grow at a CAGR of 5.5% to reach USD 1.3 billion by 2034. The key factors contributing to this growth include the rising infection rates leading to an increase in knee revision surgeries, the growing prevalence of osteoarthritis and rheumatoid arthritis, and a greater preference for minimally invasive procedures. The increasing number of elderly individuals with osteoarthritis and the demand for more effective, less invasive surgical options are crucial drivers for this market. Cementless partial knee implants, used in unicompartmental knee arthroplasty (UKA) procedures, only replace the affected portion of the knee joint, preserving more natural bone and ligaments.

These implants eliminate the need for bone cement, facilitating biological fixation instead. This method encourages the natural growth of bone tissue around the implant, leading to stronger and more durable integration between the implant and the bone. The absence of bone cement not only minimizes the risk of implant loosening over time but also reduces the likelihood of complications such as cement-related infections and inflammation. Moreover, biological fixation can enhance the overall stability of the implant, potentially extending its lifespan and improving long-term patient outcomes. As a result, cementless implants offer a more natural healing process and may require fewer revisions, making them an increasingly preferred option in orthopedic procedures.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $789.7 Million |

| Forecast Value | $1.3 Billion |

| CAGR | 5.5% |

Fixed-bearing implants segment is expected to grow at a CAGR of 5.3% to reach USD 876.2 million by 2034. These implants are mechanically simpler and less prone to failure than mobile-bearing systems, making them more popular among surgeons. They offer long-term survival rates of over 90% at ten years in low-demand patients. Additionally, mobile-bearing systems are typically more expensive and complex, which limits their acceptance and widespread use. As a result, fixed-bearing systems are the preferred choice in many cases, accelerating their adoption and contributing to their market dominance.

The titanium-based segment is anticipated to experience a growth rate of 5.4%, reaching USD 781.8 million by 2034. Titanium's biocompatibility makes it ideal for cementless implants, as it promotes osseointegration, which is crucial for the success of these devices. Titanium implants offer better adhesion to bone tissue and greater resistance to loosening compared to cobalt-chromium alloys, enhancing their stability and lifespan. The lightweight nature of titanium alloys, combined with their strength, makes them particularly suitable for younger, more active patients who require greater mobility post-surgery. Additionally, titanium is ideal for individuals with metal sensitivities, further driving demand for personalized knee arthroplasty.

U.S. Cementless Partial Knee Implants Market was valued at USD 353.7 million in 2024. The aging population in the U.S. is one of the fastest-growing demographics globally, contributing to the rising demand for knee replacement procedures. Osteoarthritis, especially medial unicompartmental osteoarthritis, is one of the primary conditions driving the need for partial knee replacements. Additionally, outpatient orthopedic surgeries are on the rise in the U.S., particularly in ambulatory surgical centers, due to the advantages of shorter anesthesia times, minimal blood loss, and quicker recovery. Moreover, the U.S. benefits from a robust reimbursement system, with both private insurers and Medicare increasingly recognizing the cost-effectiveness of partial knee replacements over total knee replacements for suitable patients.

The leading players in the Global Cementless Partial Knee Implants Market include Stryker, Medacta, Amplitude Surgical, Smith+Nephew, Waldemar Link, GRUPPO BIOIMPIANTI, ZIMMER BIOMET, Lepine, Just Medical, and Medacta. To strengthen their market presence, companies in the cementless partial knee implants industry are focusing on several strategies. They are investing in continuous innovation to improve implant designs and functionality, such as enhancing the biocompatibility and osseointegration properties of the implants. Partnerships with healthcare providers, clinics, and hospitals are also being forged to expand product reach and ensure higher adoption rates. Additionally, companies are focusing on regional expansion, particularly in emerging markets where the demand for orthopedic procedures is increasing.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising infection rates contributing to the rise in knee revisions

- 3.2.1.2 Increasing prevalence of osteoarthritis and rheumatoid arthritis

- 3.2.1.3 Growing preference for minimally invasive procedures

- 3.2.1.4 Technological advancements in cementless fixation methods

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost associated with cementless knee implants

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Reimbursement scenario

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Future market trends

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Implant Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Fixed-bearing implants

- 5.3 Mobile-bearing implants

- 5.4 Medial pivot implants

- 5.5 Other implant types

Chapter 6 Market Estimates and Forecast, By Material, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Titanium-based

- 6.3 Cobalt-chromium alloys

- 6.4 Polyethylene components

- 6.5 Other materials

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Orthopedic centres

- 7.4 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 amplitude SURGICAL

- 9.2 GRUPPO BIOIMPIANTI

- 9.3 JUST MEDICAL

- 9.4 lepine

- 9.5 Medacta

- 9.6 Smith+Nephew

- 9.7 Stryker

- 9.8 Waldemar Link

- 9.9 ZIMMER BIOMET