|

市場調査レポート

商品コード

1876808

人工膝関節全置換術市場の機会、成長要因、業界動向分析、および2025年から2034年までの予測Total Knee Replacement Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 人工膝関節全置換術市場の機会、成長要因、業界動向分析、および2025年から2034年までの予測 |

|

出版日: 2025年11月13日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

概要

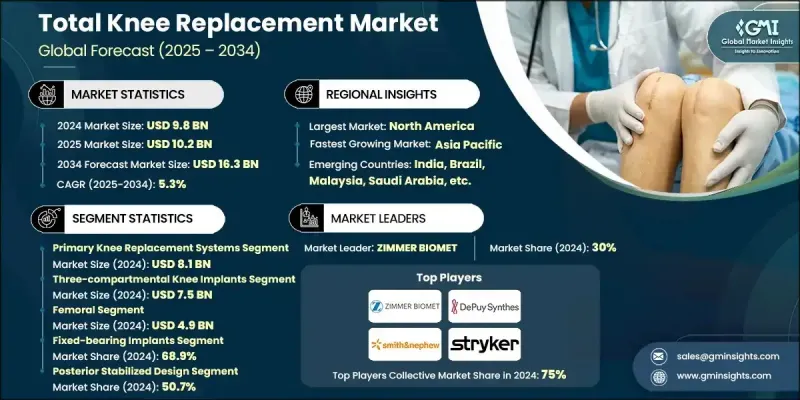

世界の全膝関節置換術市場は、2024年に98億米ドルと評価され、2034年までにCAGR5.3%で成長し、163億米ドルに達すると予測されています。

市場の成長は、変形性関節症および骨粗鬆症の有病率上昇、再手術を必要とする関節感染症の増加率、ならびに外科手術技術の継続的な進歩によって大きく牽引されています。外来手術センターおよび日帰り手術センターの拡大は、手術のアクセス向上にさらに寄与しています。変性性関節疾患は、特に高齢層において可動性を低下させ慢性疼痛を引き起こすため、機能回復と生活の質向上を目的とした人工膝関節全置換術の需要を促進しています。外科医や医療機器メーカーは、高度な画像診断技術やデジタル計画ツールを活用した革新的なインプラント設計や患者個別対応ソリューションでこれに対応しています。これらの技術はインプラントの適合性、快適性、長期的な性能を向上させると同時に、術後合併症を低減します。さらに、精密設計されカスタマイズ可能なインプラントへの需要が高まっており、メーカーは患者固有の解剖学的要件を満たし、回復結果を最適化するソリューションの開発を促進されています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測期間 | 2025-2034 |

| 開始時価値 | 98億米ドル |

| 予測金額 | 163億米ドル |

| CAGR | 5.3% |

一次膝関節置換システム分野は、2024年に81億米ドルの市場規模を生み出しました。肥満率の上昇、スマートインプラント技術の採用、3Dプリンティング技術の革新がこの分野を牽引しています。確立された臨床的信頼性と長期的な耐久性から、一次膝関節置換術は依然として第一選択の手術法として好まれています。

三室式膝関節インプラントセグメントは、2024年に75億米ドルの市場規模を生み出しました。これらのインプラントは膝の3つの関節室すべてを再表面化するよう設計されており、広範囲な関節変性を有する患者様に広く推奨され、包括的な関節修復を提供します。

北米の全膝関節置換市場は2024年に54.1%のシェアを占めました。同地域の成長は、先進的な医療インフラ、高齢化人口、精度とリハビリ成果を向上させるロボット支援手術およびスマートインプラントの導入によって牽引されています。確立された償還制度により低侵襲手術と外来手術が支援されており、市場のさらなる拡大を促進しています。

人工膝関節全置換市場における主要企業には、アレグラ、ビーブラウン、コリン、デピュイ・シンセス(ジョンソン・エンド・ジョンソン)、エノビス、エクサテック、メダクタ・インターナショナル、マイクロポート・オーソペディクス、オーソ・ディベロップメント、レストア3D、スミス・アンド・ネフュー、ストライカー、ヴァルデマール・リンク、ジマー・バイオメット、アンプリチュードなどが挙げられます。人工膝関節全置換市場をリードする主要企業は、患者個別対応インプラントや次世代手術システムの開発に向け研究開発投資を強化し、市場での存在感を高めております。多くの企業がデジタル計画技術やロボット支援技術を組み込み、手術の精度と治療成果の向上を図っております。病院、手術センター、医療提供者との戦略的提携により市場へのリーチを強化し、製品導入を促進しております。また、需要の高い地域に製造施設や流通ネットワークを構築することで、地理的な拡大も進めています。スマートインプラントや3Dプリント部品の革新は、耐久性と機能性の向上を支える優先課題です。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 関節炎および骨粗鬆症の有病率の増加

- 個別化および患者特異的なインプラントの必要性

- 増加する感染率が膝関節再手術の増加に寄与

- 二十字靭帯温存型人工膝関節全置換術への需要急増

- 単顆膝関節置換術の利用増加

- 業界の潜在的リスク&課題

- 膝関節インプラントのリコール件数の増加

- 手術に伴う高額な費用

- 機会

- スマートインプラントとIoT統合

- 新興市場における拡大

- 促進要因

- 成長可能性分析

- 規制情勢

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 償還シナリオ

- 手術の失敗率・成功率の概況

- 価格分析, 2021-2034

- 膝関節手術の現状

- 測定切除術

- ギャップバランス法

- バランスサイザー

- 測定サイズ測定器

- 患者層および疫学的動向

- ポーター分析

- PESTEL分析

- ギャップ分析

- 将来の市場動向

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業の市場シェア分析

- グローバル

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ地域

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- 提携および協力関係

- 新製品の発売

- 事業拡大計画

第5章 市場推計・予測:製品別、2021-2034

- 主要動向

- 一次人工膝関節置換システム

- 部分膝関節置換システム

- 再置換用膝関節置換システム

第6章 市場推計・予測:デバイス種別、2021-2034

- 主要動向

- 三室式膝関節インプラント

- 二室式膝関節インプラント

- 単室型膝関節インプラント

第7章 市場推計・予測:コンポーネント別、2021-2034

- 主要動向

- 大腿骨

- 脛骨

- 膝蓋骨

第8章 市場推計・予測:インプラントの種類別、2021-2034

- 主要動向

- 固定式インプラント

- 可動軸インプラント

- 内側ピボットインプラント

- その他のインプラントタイプ

第9章 市場推計・予測:設計別、2021-2034

- 主要動向

- 後方安定化設計

- 十字靭帯温存型設計

- その他の設計

第10章 市場推計・予測:手術の種類別、2021-2034

- 主要動向

- 従来型手術

- 技術支援型手術の種類

第11章 市場推計・予測:固定材料別、2021-2034

- 主要動向

- セメント固定式

- セメントレス

- ハイブリッド

第12章 市場推計・予測:材料別、2021-2034

- 主要動向

- 金属ープラスチック複合材

- セラミック対プラスチック

- 金属対金属

- セラミック対セラミック

第13章 市場推計・予測:ポリエチレンインサート別、2021-2034

- 主要動向

- 抗酸化剤入りポリエチレンインサート

- 高度架橋ポリエチレンインサート

- 従来型ポリエチレンインサート

第14章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 病院

- 外来手術センター

- その他の用途

第15章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- タイ

- マレーシア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ地域

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第16章 企業プロファイル

- Allegra

- amplitude

- B BRAUN

- Corin

- Depuy Synthes(Johnson &Johnson)

- enovis

- exactech

- Medacta International

- MicroPort Orthopedics

- ORTHO Development

16.11.復元3 D

- スミス・アンド・ネフュー

- ストライカー

- ヴァルデマール・リンク

- ジマー・バイオメット