|

|

市場調査レポート

商品コード

1137803

ストレージクラスメモリ市場- 成長、動向、予測(2022年~2027年)Storage Class Memory Market - Growth, Trends, and Forecasts (2022 - 2027) |

||||||

|

|

|||||||

|

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。 |

|||||||

| ストレージクラスメモリ市場- 成長、動向、予測(2022年~2027年) |

|

出版日: 2022年10月13日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

ストレージクラスメモリ(SCM)市場は、予測期間中に35.6%のCAGRで推移すると予測されています。

SCMは、メモリ階層における特定の性能と信頼性のギャップを埋めるものです。SCMの使用事例は、高性能なストレージキャッシュから、ブロックレベルおよびバイトレベルでのアドレス指定が可能なことから、フラッシュに代わる高速ストレージメディアまで多岐にわたります。

主なハイライト

- ストレージ・クラス・メモリ(SCM)は、ディスク・ドライブなどの回転機械式ストレージからソリッド・ステート不揮発性RAMへの移行において重要なコンポーネントです。その結果、SCMは既存のSLC/MLC NANDフラッシュ製品よりも高性能で、エネルギー効率の高いソリューションを提供することが期待されます。

- ストレージクラスメモリ(SCM)は、NANDフラッシュに比べ、読み出しや書き込みの動作が高速です。さらに、データの書き換え耐性が大幅に向上しているため、高い耐久性を有しています。SCMの特徴としては、NANDフラッシュと比較して優位性があり、DRAMと比較するとGBあたりのコストが低いことが挙げられます。

- さらに、メモリに近い速度で処理できること、停電時でも超高耐久性・持続性があることから、SCMは金融取引アプリケーション、分析、直接接続型ストレージアプリケーション、データベースなどのレイテンシーの影響を受けやすいアプリケーションに適しています。

- インタラクティブなデータベースクエリなどのビッグデータアプリケーションで使用されるインメモリ処理の需要が高まっているため、インテルや他のチップメーカーはメモリ帯域幅を増強しています。Sparkベースのクラスターコンピューティングフレームワークなどの分析ワークロードを実行する場合、Intelは、クエリがDRAMストレージの組み合わせよりも永続メモリ上で8倍速く実行されると主張しています。

- また、データセンターにおけるアプリケーションコンテナの台頭も、近年の永続的メモリへの要求を高めています。そのため、市場のエコシステムに参加しているベンダーは、CPUとサーバーの利用率の向上、分散アプリケーションの高速配信など、より大きな永続メモリ層の利点を強調しています。

- 今後、デジタルデータを不揮発性メモリに保存する場合、特定のエラーを検出・訂正するメカニズムが不可欠となります。ECC(エラー訂正コード)は、デコーダがデータの誤りを特定し訂正できるようにデータを符号化するものです。

- 世界の大流行により、多くのエンドユーザーが影響を受け、さまざまな業務が停止しています。例えば、インドではロックダウンの導入により、すべてのセクターと活動が停止されました。このようなロックダウンの導入は、あらゆる産業に大きな影響を与え、大半の企業が損失を被りました。インテルによると、仮想化デスクトップインフラと仮想化ストレージソリューションのニーズの高まりが、データセンターにおける同社のストレージおよびメモリ製品の需要を促進しています。この2つのアプリケーションのために、ストレージとメモリの機能を強化・高速化する必要性が出てきたのは、ホームオフィスに移動した大量の労働者とCOVID-19の大流行が促したデジタルリソースの利用増に対応するためだそうです。インテルの不揮発性メモリ・ソリューション・グループの第1四半期の売上高は、前年同期比46%増の13億米ドルとなりました。

主な市場動向

大幅な成長が期待されるパーシステントメモリ

- インタラクティブなデータベースクエリなどのビッグデータアプリケーションでますます利用されるようになっているインメモリ処理の需要により、インテルや他のチップメーカーはメモリ帯域幅を増強しています。Sparkベースのクラスターコンピューティングフレームワークなどの分析ワークロードを実行する場合、DRAMストレージの組み合わせよりも永続的メモリでクエリを実行した方が8倍速くなるとIntelは主張しています。

- また、データセンターにおけるアプリケーションコンテナの台頭も、近年の永続的メモリへの要求を高めています。したがって、市場エコシステムのベンダーは、CPUとサーバーの利用率の向上、分散アプリケーションの高速配信など、より大きな永続メモリ層の利点を強調しています。

- また、永続記憶メモリは、性能と効率を向上させながら、最大512ギガバイトまでメモリ容量を大幅に増やすことができます。この性能により、永続的メモリは、インメモリデータベース、分析、コンテンツ配信ネットワークなどのアプリケーションに最適です。

- また、パーシステントメモリは、パフォーマンスと効率を高めながら、メモリ容量を最大512ギガバイトまで大幅に増加させることが可能です。この性能により、永続記憶メモリはインメモリデータベース、分析、コンテンツデリバリーネットワークなどのアプリケーションに最適なものとなっています。

- ストレージコントローラーは、ハードディスクやSSDなどの周辺機器をサーバーやコンピューターに接続するために使用されていました。コントローラはCPUと直接通信し、通常はPCIeインタフェースを介して通信します。ストレージコントローラの仕事は、I/O要求をデータブロックに変換して、物理メディアとの間で読み書きを行うことです。ハードディスクはメインメモリより速度が遅いため、ストレージコントローラはキャッシュの役割も果たし、ハードウェアRAIDなどのデータセキュリティ機能を実行します。

- 潜在的な応用分野での永続メモリの需要が高まる中、2020年8月、マウザー・エレクトロニクスは、インテルOptane永続メモリの在庫を開始したことを発表しました。Intel Optaneパーシステントメモリモジュールは、揮発性メモリまたは永続的な高性能データ層として機能することができる、大容量で手頃な価格のメモリへのアクセスを提供するために開発されました。

北米が市場で高いシェアを獲得

- 北米では、ビッグデータ解析の増加、モバイルブロードバンドの普及、クラウドコンピューティングなどが、新しいデータセンターインフラへの需要を促進しています。また、この地域では、ストレージやメモリ市場に参入する新しいプレーヤーや技術も示されています。

- Data Reportalによると、2022年1月、米国のインターネットユーザー数は3億720万人でした。2022年初頭には、米国の総人口の92.0%がインターネットにアクセスできるようになりました。2022年1月、米国には約3億720万人のインターネットユーザーがいた。このとき、約2億7000万人がソーシャルメディアを利用していました。

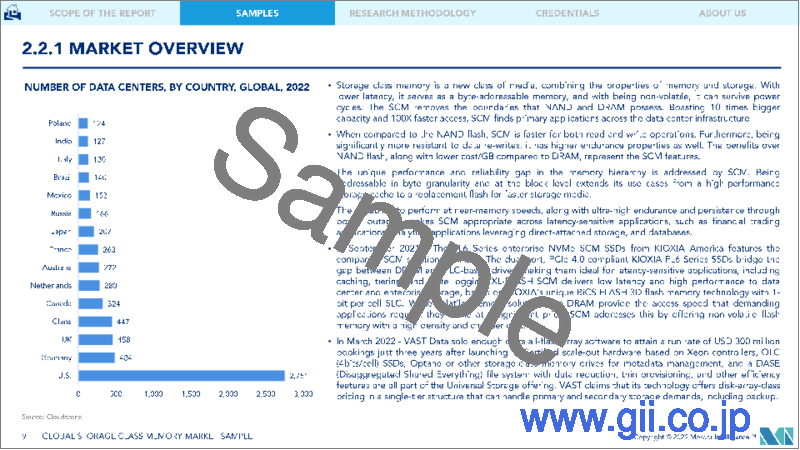

- さらに、2021年第3四半期には、米国のインターネットユーザーの90%が携帯電話からインターネットにアクセスしていました。さらに、同国は最大数のデータセンターを保有しています。Cloudsceneによると、同国には合計で2,751のデータセンターがあり、世界第2位に立ったドイツは合計で484のデータセンターしかなかっています。これは、世界最大のデータセンターである米国のデータセンター市場に大きな差があることを示しており、したがって、ストレージクラスメモリの巨大市場であることを表しています。

- また、同地域では、データセンターのアップグレード、拡張、新規建設など、データセンター市場への投資が継続的に行われています。例えば、2022年2月、コロジックスはCIMグループと提携し、カナダのトロントに新しいデータセンターを建設しました。2つのジョイントベンチャーは、オンタリオ州マーカムに50,000平方フィート(4,650平方メートル)、15MWのデータセンター「TOR4」を建設・運営することを目的としています。

- 低レイテンシー、高耐久性、信頼性の高いデータの一貫性を必要とする戦略的な業務用アプリケーションやデータベースは、永続記憶による恩恵を受ける傾向にあります。この技術は、仮想マシン(VM)ストレージを高速化し、マルチノード、分散型クラウドアプリケーションに高いパフォーマンスを提供することができます。この地域の主要プレイヤーは、最先端技術の開発に積極的に取り組んでおり、市場には大きなチャンスが広がっています。

- さらに、同地域ではビッグデータとIoTの浸透により、次世代モジュール型データセンターの規模と範囲が大きく変化すると予想されます。既存の競争に伴い、組織はITのスケーラビリティと容量の進化を迫られています。データの急激な増加、ハイブリッドクラウド、サードパーティデータセンターのアウトソーシングにより、最小限の時間でセンターを設置できる柔軟性から、コンテナ型データセンターが人気を博しています。

競合情勢

ストレージクラスメモリの市場は、サムスンやパナソニックなどの大手企業が独占的に製品を提供しているため、統合されています。また、SCMは製造コストが高いため、新規参入やシェア獲得は厳しい状況です。したがって、この傾向は予測期間中も続くと予想されます。

- 2022年8月-Kioxiaは、Linux FoundationのSoftware-Enabled Flash技術に対応した新しいソフトウェア定義インターフェースなどの開発成果を発表しました。このオープンソースプロジェクトは、技術をよりよく利用するカスタマイズ可能なフラッシュストレージを導入することで、レガシーHDDのプロトコルから脱却しています。Kioxiaはまた、新しいPCIe Gen 5 SSDファミリーとFL6ストレージクラスメモリ(SCM)の更新を発表しました。

- 2022年3月-Micron Technology, Inc.は、データセンター向けに初めて垂直統合された176層NAND SSDのリリースを発表しました。NVMeTM搭載Micron 7450 SSDは、2ミリ秒(ms)未満のサービス品質(QoS)レイテンシ、広い容量範囲、および最も多くのフォームファクタにより、最も要求の厳しいデータセンターのワークロードの要件を満たします。3D Xpointを含むその他のストレージ・クラス・メモリ(SCM)。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査対象範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場の力学

- 市場概要

- 市場促進要因と抑制要因のイントロダクション

- 市場促進要因

- NANDとDRAMの機能融合による性能と信頼性の向上

- メモリ増設による演算性能の向上

- 市場の課題

- 高い製造コスト

- バリューチェーン分析

- 業界の魅力- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- COVID-19の業界への影響

第5章 市場のセグメンテーション

- アプリケーション

- SSD

- クライアントSSD

- エンタープライズSSD

- 永続記憶装置

- データセンター

- ワークステーション

- SSD

- 地域

- 北米

- 欧州

- アジア太平洋地域

- 世界のその他の地域

第6章 競合情勢

- 企業プロファイル

- Crossbar Inc.

- Hewlett Packard Enterprise

- Everspin Technologies Inc.

- Western Digital Corporation

- Micron Technology Inc.

- Samsung Electronics Co. Ltd

- Intel Corporation

- Toshiba Memory Holding Corporation(Kioxia)

- MemVerge

第7章 投資分析

第8章 市場の将来性

The Storage Class Memory (SCM) Market is projected to register a CAGR of 35.6% during the forecast period. SCM fills the specific performance and reliability gap in the memory hierarchy. Its use cases range from high-performance storage cache to a replacement for flash for faster storage media due to its addressability at the block and byte levels.

Key Highlights

- Storage Class Memory (SCM) is a critical component in the transition from rotating mechanical storage, such as disk drives, to solid-state, non-volatile RAM. As a result, SCM promises to deliver higher-performance and more energy-efficient solutions than existing SLC/MLC NAND flash products.

- Storage Class Memory (SCM) is faster for reading and writing operations than NAND flash. Furthermore, it has higher endurance properties due to being significantly more resistant to data rewrites. SCM features include advantages over NAND flash and a lower cost per GB when compared to DRAM.

- Furthermore, the ability to perform at near-memory speeds, as well as ultra-high endurance and persistence through power outages, makes SCM suitable for latency-sensitive applications such as financial trading applications, analytics, direct-attached storage applications, and databases.

- The demand for in-memory processing increasingly used in Big Data applications, like interactive database queries, has prompted Intel and other chipmakers to boost memory bandwidth. When running analytics workloads, such as the Spark-based cluster computing framework, Intel claims queries run eight times faster on persistent memory than on DRAM storage combinations.

- The rise of application containers in data centers also has boosted requirements for persistent memory in recent years. Hence, vendors present in the market ecosystem are emphasizing the advantages of larger persistent memory tiers, including increased CPU and server utilization and the faster delivery of distributed applications.

- Moving forward, when digital data is stored in non-volatile memory, it is essential to have a mechanism for detecting and correcting specific errors. Error correction code (ECC) offers to encode data so that a decoder can identify and correct errors in the data.

- Many end-user industries across different nations were affected by the pandemic resulting in the shutdown of various business operations. For instance, the introduction of lockdowns in India indicated shutting down all sectors and activities. These lockdown implementations lead to a massive impact on every industry, with the majority of businesses suffering losses. According to Intel, the increased need for virtualized desktop infrastructure and virtualized storage solutions is driving demand for its storage and memory products in the data center. The need to enhance and accelerate storage and memory capabilities for the two application types has come in response to the large number of workers who moved to home offices and a rise in the use of digital resources that have been prompted by the COVID-19 pandemic. Intel's Non-Volatile Memory Solutions Group saw first-quarter revenue grow 46% year-over-year to USD 1.3 billion.

Key Market Trends

Persistent Memory is Expected to Grow Significantly

- Demand for in-memory processing, increasingly used in big data applications like interactive database queries, has prompted Intel and other chipmakers to boost memory bandwidth. When running analytics workloads such as the Spark-based cluster computing framework, Intel claims queries run eight times faster on persistent memory than on DRAM storage combinations.

- The rise of application containers in data centers has also boosted requirements for persistent memory in recent years. Hence, vendors in the market ecosystem emphasize the advantages of larger persistent memory tiers, including increased CPU and server utilization and the faster delivery of distributed applications.

- Persistent memory can also significantly increase memory capacity to up to 512 Gigabytes while providing increased performance and efficiency. This performance makes persistent memory ideal for applications such as in-memory databases, analytics, and content delivery networks.

- Persistent memory is also capable of significantly increasing memory capacity to up to 512 Gigabytes while providing increased performance and efficiency. This performance makes persistent memory ideal for applications such as in-memory databases, analytics, and content delivery networks.

- A storage controller was used to link peripheral devices like hard drives and SSDs to a server or computer. The controller communicates with the CPU directly, typically over the PCIe interface. The storage controller's job is to translate I/O requests into data blocks for reading and writing to and from physical media. Because hard drives are slower than main memory, the storage controller also serves as a cache and performs data security features, such as hardware RAID.

- With the rising demand for persistent memory in potential application areas, in August 2020, Mouser Electronics announced that it is now stocking Intel Optane persistent memory. Intel Optane persistent memory modules were developed to provide access to large, affordable memory capacity that is able to act as either volatile memory or a persistent, high-performance data tier.

North America to Hold a Prominent Share in the Market

- An increase in big data analytics, growth of mobile broadband, and cloud computing are driving the demand for new data center infrastructure in the North American region. The region also witnesses new players and technology entering the storage and memory markets.

- According to Data Reportal, in January 2022, there were 307.2 million internet users in the United States. At the start of 2022, 92.0% of the United States' total population had internet access. In January 2022, the United States had around 307.2 million internet users. Around 270 million people were using social media at the time.

- Further, 90% of US internet users accessed the internet via their mobile phones in the third quarter of 2021. Moreover, the country hosts the maximum number of data centers. According to Cloudscene, the country has 2,751 data centers in total, while Germany, which stood at the second-highest in the world, had only 484 data centers in total. This shows the huge difference in the data center market of the United States, which is the biggest in the world; therefore, it represents a huge market for storage-class memory.

- Additionally, the region is witnessing continue investment in the data center market in upgradation, expansion, and new construction of data centers. For instance, in February 2022, Cologix partnered with CIM Group to create a new data center in Toronto, Canada. The two joint venture aims to build and operate TOR4, a 50,000 square foot (4,650 square meters), 15MW data center in Markham, Ontario.

- Strategic operational applications and databases requiring low latency, high durability, and reliable data consistency tend to benefit from persistent memory. The technology can accelerate virtual machine (VM) storage and deliver higher performance to multi-node, distributed cloud applications. The region's major players are actively involved in the development of cutting-edge technology, which is opening up huge opportunities for the market.

- Moreover, Big Data and IoT penetration in the region is expected to significantly transform the next-generation modular data centers' size and scope. With the existing competition, organizations are under pressure to evolve IT scalability and capacity. With the exponential growth of data, hybrid cloud, and outsourcing third-party data centers, containerized data centers gain traction, owing to their flexibility in installing a center within the least possible time.

Competitive Landscape

The market for storage-class memory is consolidated due to the presence of major players like Samsung and Panasonic, who dominate the market with their offerings. Also, as the manufacturing cost is high for SCM, the entry for new entrants and gaining market share is challenging. Hence, the trend is expected to continue in the forecast period.

- August 2022 - Kioxia announced a number of developments, including a new software-defined interface for the Linux Foundation's Software-Enabled Flash technology. The open source project departs from legacy HDD protocols by introducing customizable flash storage that uses the technology better. Kioxia also introduced a new PCIe Gen 5 SSD family and an update to its FL6 storage class memory (SCM).

- March 2022 - Micron Technology, Inc. announced the release of the first 176-layer NAND SSD for data centers to be vertically integrated. The Micron 7450 SSD with NVMeTM satisfies the requirements of the most demanding data center workloads with a quality-of-service (QoS) latency of fewer than two milliseconds (ms), a wide capacity range, and the most form factors. Other storage-class memory (SCM), including 3D Xpoint.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Introduction to Market Drivers and Restraints

- 4.3 Market Drivers

- 4.3.1 Increased Performance and Reliability by Combining NAND and DRAM Features

- 4.3.2 Faster Computing Power with More Memory

- 4.4 Market Challenges

- 4.4.1 High Manufacturing Costs

- 4.5 Industry Value Chain Analysis

- 4.6 Industry Attractiveness - Porter's Five Force Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Impact of COVID-19 on the Industry

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 SSD

- 5.1.1.1 Client SSD

- 5.1.1.2 Enterprise SSD

- 5.1.2 Persistent Memory

- 5.1.2.1 Data Center

- 5.1.2.2 Workstation

- 5.1.1 SSD

- 5.2 Geography

- 5.2.1 North America

- 5.2.2 Europe

- 5.2.3 Asia Pacific

- 5.2.4 Rest of the World

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles*

- 6.1.1 Crossbar Inc.

- 6.1.2 Hewlett Packard Enterprise

- 6.1.3 Everspin Technologies Inc.

- 6.1.4 Western Digital Corporation

- 6.1.5 Micron Technology Inc.

- 6.1.6 Samsung Electronics Co. Ltd

- 6.1.7 Intel Corporation

- 6.1.8 Toshiba Memory Holding Corporation (Kioxia)

- 6.1.9 MemVerge