|

市場調査レポート

商品コード

1403809

自動車用ピストンエンジンシステム-市場シェア分析、産業動向・統計、2024~2029年成長予測Automotive Piston Engine System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 自動車用ピストンエンジンシステム-市場シェア分析、産業動向・統計、2024~2029年成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 90 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

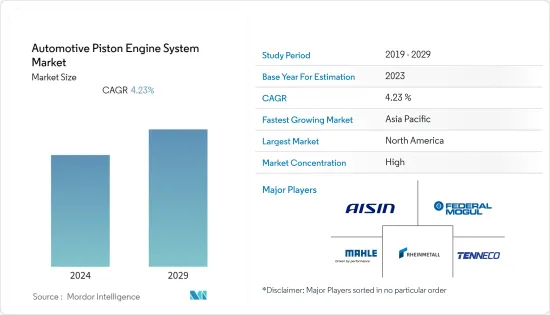

自動車用ピストンエンジンシステム市場は、現在のところ42億6,000万米ドルと評価されています。

今後5年間のCAGRは4.23%で、52億4,000万米ドルに達すると予測されています。

大手自動車メーカーや相手先商標製品メーカー(OEM)によるエンジンの技術革新やプロトタイプが、高性能で低燃費の自動車に対する消費者の嗜好と相まって、市場成長を促進する主要要因の一部となっています。エンジンの小型化動向は増加傾向にあり、自動車メーカーはより優れた燃料噴射システムを備えた小型エンジンを開発しています。さらに、軽量コンポーネントを自動車モデルに組み込むという自動車産業の急速な変革が、自動車用ピストンエンジンシステム市場の成長を後押ししています。これは、自動車効率の向上を支援する先進的なピストンを開発するために、複数の部品メーカーが技術の向上とコミットメントを行っているためです。

二酸化炭素排出対策として電気自動車の普及に力を入れる政府が増える中、燃料自動車の販売動向は大きな影響を受けています。電気自動車にピストンを組み込むことは任意であるため、自動車用ピストンエンジンシステム市場にとって大きな課題となっています。一方、ピストンシステムの生産は、自動車保有台数の増加により、アフターマーケット・チャネルで牽引力を増しています。中古車を購入する消費者は、常に車の部品やコンポーネントのアップグレードを必要としています。これらは、自動車用ピストンエンジンシステム市場の需要にプラスの影響を与えます。

中国、インド、日本は世界の自動車メーカーの拠点として成長しており、アジア太平洋は、液化石油ガス(LPG)、圧縮天然ガス(CNG)、ディーゼルエンジンなどの代替燃料自動車の製造が増加しているため、自動車用ピストンシステムの主要市場として継続すると予想されます。さらに、新興国市場では、自動車の効率と燃費性能を向上させるために、さまざまな軽量ピストン部品の市場開拓が進むと予想されます。

自動車用ピストンエンジンシステム市場の動向

乗用車セグメントが市場を独占すると予測

LPG CNG自動車などの代替燃料自動車を好む消費者の増加が、ピストンエンジンシステム市場の成長を予測しています。様々な自動車メーカーが新時代の自動車を開発するために常に多額の資金を費やしており、自動車に使用される軽量ピストン部品が必要とされています。これと相まって、いくつかの地域では中古車需要が増加しており、自家用交通手段を利用する消費者の嗜好に起因する自動車保有台数の増加が、自動車用ピストンエンジンシステム市場の需要にプラスの影響を与えています。自動車の高年齢化に伴い、常にアップグレードが必要となるため、燃料自動車のアフターマーケットでピストンシステムを変更することが、この分野の市場を牽引すると予想されます。

一方、電気自動車の販売台数の増加が自動車用ピストンシステム市場の成長を妨げています。販売台数の急増は、排ガスレベルを管理し、ゼロ・エミッション車を普及させるために、さまざまな組織や政府による規制基準が強化された結果です。その結果、自動車メーカーは電気自動車の研究開発への支出を増やすことに継続的に取り組み、注力しています。

世界の電気自動車(バッテリー電気自動車、燃料電池電気自動車、プラグインハイブリッド自動車を含む)市場は、2018年以降、販売登録台数が毎年大幅に増加しています。この増加は、乗用車と商用車を含むほぼすべてのセグメントで記録されました。例えば

- バッテリー電気自動車(BEV)の世界販売台数は、2021年の460万台に対し、2022年には730万台に達し、2021年から2022年にかけて前年比58.7%の伸びを示しました。

電気自動車への傾斜が強まり、各国政府が補助金を提供し、自動化と排出量削減のニーズが高まる中、自動車産業の電動化は予測期間中、市場の主要な抑制要因となると思われます。

予測期間中、アジア太平洋が市場を独占する

予測期間中、アジア太平洋が自動車用ピストンエンジンシステム市場の主要地域になると予測されます。これは主に、特に商用車分野で内燃機関に大きく依存しているためです。例えば

- 2022年のインドの商用車販売台数は93万3,000台で、2021年の67万7,000台と比べ、2021年から2022年にかけて前年比37.8%の成長を記録しました。

- 同様に、インドネシアの商用車の新規販売台数は、2021年の22万7,000台に対し、2022年には26万4,000台となり、2021年から2022年にかけて前年比16.3%の伸びを記録しました。

アジア太平洋では近年、電気商用車が牽引役となっているが、2022年時点でも内燃機関商用車市場は堅調を維持しています。しかし、アジア太平洋市場ではICE商用車の普及が進んでいるため、自動車用ピストンエンジンシステム市場は今後数年で成長が鈍化する可能性があります。

都市化率の上昇、自動車保有台数の増加、消費者の一人当たり可処分所得の増加が、アジア太平洋の自動車市場を牽引しています。より良い雇用と経済的機会を求めて都市部に移住する消費者が増えるにつれて、民間輸送を利用することへの嗜好が高まり、この地域の乗用車市場にプラスの影響を与えています。これは、同地域の乗用車市場にプラスの影響を与え、同地域のポジションエンジンシステム市場にもプラスの影響を与えます。

電気自動車の普及が加速しているにもかかわらず、ピストンメーカーは、燃料で動く中古車を利用する消費者に対応するために、アフターマーケットに大きな可能性を残しています。アジア太平洋では、電気自動車への傾斜が強まっているにもかかわらず、従来型のICエンジンの市場が巨大であるため、予測期間中、自動車用ピストンエンジンシステムの成長ポテンシャルは高くなると予想されます。

自動車用ピストンエンジンシステム産業概要

自動車用ピストンエンジンシステム市場は統合され、競争が激しく、市場を独占している企業はわずかです。市場で事業を展開している主要企業には、Aisin Seiki、Federal-Mogul Holding LLC、Mahle GmbH、Tenneco Inc、Rheinmetall Automotive AG、Hitachi Automotive Systems、Riken Corporationなどがあります。これらの参入企業は、ガソリン車やディーゼル車用のさまざまなピストン部品を提供することで、ブランドポートフォリオを強化するために、自動車メーカーとの長期的なパートナーシップの形成に積極的に取り組んでいます。

- 2023年1月、Rheinmetallは大口径ピストンの生産をスウェーデンのヨーテボリにあるKoncentra Verkstads AB(KVAB)に正式に移管しました。2022年10月、ラインメタルはこの売却を発表しました。これは、デュッセルドルフの技術グループが、小口径ピストンの開発に重点を置くという戦略的方向転換を行ったことを反映したものです。

- 2022年8月、Nippon Piston RingとRiken Corporationは、相互株式移転による共同持株会社の設立に関する覚書(MoU)合意を発表。両社を対等の条件で統合するものです。合意に基づき、新合弁会社の商号はNPR-Riken Corporationとなります。同社は、自動車産業向けの高度なポジションソリューションの開発を促進することを目的としています。

市場では今後数年間、様々な先進的軽量ピストン部品の発売が予想され、これらの参入企業は製品ポートフォリオの多様化によって競合を得ようとしています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 軽量ピストンの需要拡大

- 市場抑制要因

- 電気自動車の普及が市場成長を阻害

- 業界の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(市場規模-米ドル)

- 原材料タイプ別

- 鋳鉄

- アルミニウム合金

- その他の原材料(スチールなど)

- 車種別

- 乗用車

- 商用車

- 燃料別

- ガソリン

- ディーゼル

- コンポーネント別

- ピストン

- ピストンリング

- ピストンピン

- 地域別

- 北米

- 米国

- カナダ

- その他の北米

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- その他の欧州

- アジア太平洋

- インド

- 中国

- 日本

- 韓国

- その他のアジア太平洋

- 世界のその他の中東・アフリカ

- 南米

- 中東・アフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Aisin Seiki

- Capricorn Automotive

- Federal Mogul Holding LLC

- Mahle GmbH

- Rheinmetall

- Hitachi Automotive Systems

- Shriram Pistons & Rings Ltd

- Magna International

- Tenneco Inc

- Riken Corporation

- PT Astra Otoparts Tbk

第7章 市場機会と今後の動向

- 中古ガソリン/ディーゼル車の成長によるアフターマーケットでの機会拡大

The automotive piston engine system market is valued at USD 4.26 billion in the current year. It is anticipated to reach a net valuation of USD 5.24 billion within the next five years, registering a CAGR of 4.23% over the forecast period.

Innovations and prototypes of engines from major automakers and original equipment manufacturers (OEMs), coupled with consumer preferences for high-performance and fuel-efficient automobiles, are some of the major factors propelling the market growth. Engine downsizing trends are on the rise, with automakers developing smaller engines with better fuel injection systems. Further, the rapid transformation of the automotive industry in integrating lightweight components in their vehicle models is propelling the growth of the automotive piston engine system market. It is owing to the enhancement in technology and commitment by several parts and component manufacturers to develop advanced pistons, which assist in improving vehicle efficiency.

With the increasing focus of the government to promote the usage of electric vehicles to combat carbon emissions, the sales trends of fuel-operated vehicles are significantly being affected. It poses a major challenge for the automotive piston engine system market, as the integration of pistons in electric vehicles is optional. On the other hand, the production of piston systems is gaining traction in the aftermarket channels, owing to the growth in vehicle parc. Consumers availing of used cars are constantly in need of upgrading their vehicle's parts and components. These positively impact the demand for the automotive piston engine systems market.

With China, India, and Japan growing as global automotive manufacturer hubs, the Asia-Pacific region is expected to continue as a major market for automotive piston systems due to the increase in manufacturing of alternative fuel vehicles such as liquefied petroleum gas (LPG), compressed natural gas (CNG), and diesel engines. Further, the market is anticipated to witness the development of various lightweight piston components to improve the efficiency of vehicles and better fuel consumption capability.

Automotive Piston Engine System Market Trends

Passenger Car Segment is Anticipated to Dominate the Market

Increasing preference of consumers to avail alternative fuel vehicles, such as LPG CNG operated cars, is anticipated the growth of the piston engine system market. Various auto manufacturers are constantly spending hefty sums in developing new-age vehicles, which require lightweight piston components to be utilized in the vehicles. Coupled with that, the growing demand for used cars in several regions and increasing vehicle parc, owing to consumers' preference towards availing private transportation medium, is positively impacting the demand for automotive piston engine system market. The increasing age of vehicles requires constant upgradation, and therefore, changing piston systems in the aftermarket for fuel-operated vehicles is expected to drive this segment of the market.

On the other hand, the rise in sales of electric vehicles is hindering the growth of the automotive piston system market. The spike in sales is the result of an increase in regulatory norms by various organizations and governments to control emission levels and to propagate zero-emission vehicles. As a result, automakers are continually working and focusing on increasing their expenditure on the R&D of electric vehicles, which may aid OEMs in marketing electric vehicles in the future.

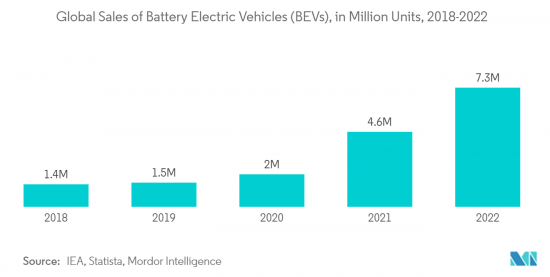

The global electric vehicles (including battery electric vehicles, fuel cell electric vehicles, and plug-in hybrid vehicles) market observed a tremendous increase in the number of sales registered every year since 2018. This increase was registered in almost all segments of vehicles, which include passenger vehicles and commercial vehicles. For instance-

- In 2022, global sales of battery electric vehicles (BEVs) touched 7.3 million units, compared to 4.6 million units in 2021, representing a 58.7% Y-o-Y growth between 2021 and 2022.

With the increased inclination toward electric vehicles, governments of different countries offering subsidies, and the growing need for automation and reduced emissions, the electrification of the automotive industry will serve as a major restraint for the market during the forecast period.

Asia-Pacific to Dominate the Market during the forecast period

Asia-Pacific region is projected to be the leading region for the automotive piston engine system market during the forecast period. It is mainly due to the heavy reliance on internal combustion engines, especially in the commercial vehicles sector. For instance,

- In 2022, India witnessed sales of 933 thousand units of commercial vehicles, compared to 677 thousand units in 2021, recording a Y-o-Y growth of 37.8% between 2021 and 2022.

- Similarly, new sales of commercial vehicles in Indonesia touched 264 thousand units in 2022, compared to 227 thousand units in 2021, representing a 16.3% Y-o-Y between 2021 and 2022.

Although electric commercial vehicles in the Asia-Pacific region gained traction in recent years, the market of ICE commercial vehicles remained strong as of 2022. However, with the increasing penetration of ICE commercial vehicles in the Asia-Pacific market, the automotive piston engine system market might witness falling growth in the coming years.

The increasing urbanization rate, growing vehicle parc, and the rising per capita disposable income of consumers are driving the automotive market in the Asia-Pacific region. As more consumers migrate to urban for better employment and financial opportunities, the preference towards availing private transportation medium shoots up, which positively impacts the passenger car market in the region. It, in turn, positively impacts the position engine system market in this region.

Despite the ramping penetration of electric vehicles at a faster rate, there remains a massive potential in the aftermarket for piston manufacturers to cater to consumers who avail of fuel-operated used cars. With the immense market for conventional IC engines in the regions, despite the growing inclination toward electric vehicles, the growth potential for automotive piston engine systems is expected to be high in Asia-Pacific during the forecast period.

Automotive Piston Engine System Industry Overview

The automobile piston engine system market is consolidated and highly competitive, with only a few companies dominating the market. Some of the major companies operating in the market are Aisin Seiki, Federal-Mogul Holding LLC, Mahle GmbH, Tenneco Inc, Rheinmetall Automotive AG, Hitachi Automotive Systems, and Riken Corporation, among others. These players actively engage in forming long-term partnerships with auto manufacturers to enhance their brand portfolio by offering various piston components for gasoline or diesel vehicles.

- In January 2023, Rheinmetall officially transferred its large-bore pistons production to Koncentra Verkstads AB (KVAB) of Gothenburg, Sweden. In October 2022, Rheinmetall announced the sale, which reflected the Dusseldorf tech group's strategic reorientation towards an improved focus on developing small-bore pistons.

- In August 2022, Nippon Piston Ring and Riken Corporation announced a Memorandum of Understanding (MoU) agreement to establish a joint holding company formed by mutual stock transfer. It is to consolidate the two companies on equal terms. As per the agreement, the trading name of the new joint company will be NPR-Riken Corporation. The company aims to facilitate the development of advanced position solutions for the automotive industry.

The market is anticipated to witness the launch of various advanced lightweight piston components in the coming years as these players try to gain a competitive edge with the diversification of their product portfolio.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Growing Demand for Lightweight Pistons

- 4.2 Market Restraints

- 4.2.1 Increasing Adoption of Electric Vehicles Deters the Growth of the Market

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value - USD)

- 5.1 By Raw Material Type

- 5.1.1 Cast Iron

- 5.1.2 Aluminum Alloy

- 5.1.3 Other Raw Materials (Steel, etc.)

- 5.2 By Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Commerical Vehicles

- 5.3 By Fuel Type

- 5.3.1 Gasoline

- 5.3.2 Diesel

- 5.4 By Component Type

- 5.4.1 Piston

- 5.4.2 Piston Ring

- 5.4.3 Piston Pin

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Spain

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 India

- 5.5.3.2 China

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Rest of the World

- 5.5.4.1 South America

- 5.5.4.2 Middle-East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles*

- 6.2.1 Aisin Seiki

- 6.2.2 Capricorn Automotive

- 6.2.3 Federal Mogul Holding LLC

- 6.2.4 Mahle GmbH

- 6.2.5 Rheinmetall

- 6.2.6 Hitachi Automotive Systems

- 6.2.7 Shriram Pistons & Rings Ltd

- 6.2.8 Magna International

- 6.2.9 Tenneco Inc

- 6.2.10 Riken Corporation

- 6.2.11 PT Astra Otoparts Tbk

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rising Opportunity in the Aftermarket owing to the Growth in Used Gasoline/Diesel Cars