|

市場調査レポート

商品コード

1687240

食品包装検査:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Food Packaging Testing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 食品包装検査:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 90 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

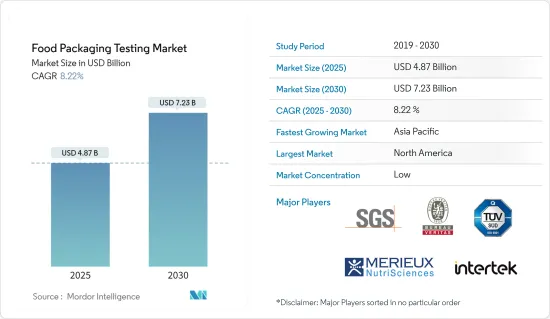

食品包装検査の市場規模は2025年に48億7,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは8.22%で、2030年には72億3,000万米ドルに達すると予測されます。

主なハイライト

市場の主な原動力は、食品を安全に届けることを目的とした食品包装材料の品質に対する意識の高まりであり、移行による食品の組成の許容できない変化を回避し、食品の香りや味を損なわないようにすることです。また、消費者の間でパッケージから食品への化学物質の移行による健康被害に対する懸念が高まっていることや、食品の安全性を規制するための包装試験要件を遵守するための規制がますます厳しくなっていることも、市場を牽引する大きな要因となっています。しかし、先端技術による検査コストが高いことが市場成長の妨げになると予想されます。

包装材料別のセグメンテーションフォントでは、テトラパックの需要は、高保存期間の食品の需要の増加により、近年大幅に増加しています。飲料用包装は、包装された飲料製品の消費量が多いことから、包装試験市場において支配的な用途となっています。また、食品包装用プラスチックの使用増加により、包装検査材料タイプではプラスチックが大きなシェアを占めています。食品包装に使用されるPETとLLDPEは、フレキシブル包装のため、より速いペースで成長しています。

食品包装検査市場の動向

食品の安全性を得るための先進パッケージング材料への需要の増加

製品は包装された形で顧客の手元に届くため、その安全性は重要な関心事です。有毒な汚染物質や有害な汚染物質が存在すると、製品自体に影響を及ぼす可能性があります。汚染物質の存在は製品の品質を大幅に低下させる可能性があり、市場における包装検査の重要性が強調されています。そのため、インテリジェント包装、アクティブ包装、スマート包装、ガス置換包装といった先進的な包装方法が、食品の品質に有害な影響を与えない従来の方法に取って代わりつつあり、こうした包装商品を効果的に検査する必要性をさらに高めています。Organic Trade Associationによると、ラテンアメリカ、アルゼンチンにおける有機食品パッケージ消費の売上は、2020年には650万米ドルに達すると予測されている、

北米と欧州が食品包装検査市場を牽引

食品包装検査市場の世界シェアは北米が最も大きく、次いで欧州が続きます。EUと北米における毒性試験、暴露評価、リスク評価を含む食品包装の厳格な安全性評価が市場を牽引しています。これらの地域を支配している主要国際企業には、SGS SA、Bureau Veritas Group、Intertek Group plc、Merieux NutriSciences Corporationなどがあります。

食品包装検査業界の概要

食品包装検査の世界市場は、各国の地域および国内の大手企業の存在により断片化されています。消費者の間でブランドプレゼンスを高めるために主要企業が採用する戦略的アプローチとして、新製品の開発とともに企業の合併、拡大、買収、提携が重視されています。例えば、2019年4月、DDLは、ニュージャージー州エジソンのCryopak本社にある6,000平方フィートの独立研究所であるCryopak Testing Centerが、環境調整、流通シミュレーション、完全性と強度試験、熱性能、貯蔵寿命試験にわたるパッケージ試験を提供するDDLの試験所としてリブランドされたと発表しました。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 検査タイプ別

- フィジカル試験

- 耐久性試験

- 耐熱性試験

- 水蒸気・ガス透過性試験

- ケミカル試験

- 移行試験

- 抽出性試験

- 浸出性試験

- その他

- フィジカル試験

- 包装材料別

- プラスチック

- ガラス

- 金属

- 紙・板

- レイヤー包装

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 欧州

- スペイン

- 英国

- ドイツ

- フランス

- イタリア

- ロシア

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- その他中東とアフリカ

- 北米

第6章 競合情勢

- 最も活発な企業

- 最も採用されている戦略

- 市場シェア分析

- 企業プロファイル

- SGS SA

- Bureau Veritas Group

- Intertek Group plc

- Merieux NutriSciences Corporation

- TUV SUD South Asia Pvt. Ltd.

- Eurofins Scientific

- Microbac Laboratories Inc.

第7章 市場機会と今後の動向

The Food Packaging Testing Market size is estimated at USD 4.87 billion in 2025, and is expected to reach USD 7.23 billion by 2030, at a CAGR of 8.22% during the forecast period (2025-2030).

Key Highlights

The market is mainly driven by its rising awareness for the quality of the food packaging material aiming to deliver food safely to avoid unacceptable change in the composition of the food through migration and keeping the aroma or taste of the food intact. Also, growing concern over the health hazard of chemical migrants from package to food products among consumers and increasingly strict regulation to comply with packaging testing requirements to regulate food safety is another major factor driving the market. However, the high cost of testing by advanced technology is expected to impede the market growth.

On the segmentation font by packaging material, the demand for tetra pack has increased significantly in recent years, due to the increased demand for high shelf life food products. Beverage packaging is the dominant application in the packaging testing market, owing to the high consumption of packaged beverage products. Also, plastic holds a major share in the packaging testing material type, driven by the increased use of plastic for food packaging. PET and LLDPE used for food packaging are growing at a faster pace, due to flexible packaging.

Food Packaging Testing Market Trends

Increasing demand for advanced packaging material to obtain food safety

As products reach customers in the packaged form, their safety is an important concern; the presence of any toxic or damaging contaminant could affect the product itself. The presence of contaminants could decrease the quality of the product substantially, which emphasizes the importance of package testing in the market. Therefore, advanced packaging methods, such as intelligent packaging, active, smart packaging, and modified atmosphere packaging, are replacing traditional methods, which deliver no toxic effects on the food quality and are further driving the need to effectively test these packaged goods. According to the Organic Trade Association, sales of organic food package consumption in Latin America Nation, Argentina are forecasted to reach USD 6.5 million in 2020,

North America and Europe to drive the food packaging testing market

North America has the largest share in the global market of food packaging testing market, which was followed by Europe. Strict safety evaluation of food packaging, which includes toxicology testing, exposure assessment, and risk assessment in EU and North America, is driving the market. A few of the leading international companies dominating these regions include SGS SA, Bureau Veritas Group, Intertek Group plc and Merieux NutriSciences Corporation among others.

Food Packaging Testing Industry Overview

The global market for food packaging testing is fragmented, owing to the presence of large regional and domestic players in different countries. Emphasis is given on the merger, expansion, acquisition, and partnership of the companies along with new product development as strategic approaches adopted by the leading companies to boost their brand presence among consumers. For instance, in April 2019, DDL announced that the Cryopak Testing Center, a 6,000 square foot independent laboratory located at Cryopak's Headquarters in Edison, NJ, has been rebranded as a DDL testing laboratory offering package testing across environmental conditioning, distribution simulation, integrity and strength testing, thermal performance, and shelf-life testing.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Testing Type

- 5.1.1 Physical Testing

- 5.1.1.1 Durability Testing

- 5.1.1.2 Heat Resistance Testing

- 5.1.1.3 Water Vapor /Gas Permeability Testing

- 5.1.2 Chemical Testing

- 5.1.2.1 Migration Testing

- 5.1.2.2 Extractable Testing

- 5.1.2.3 Leachable Testing

- 5.1.2.4 Others

- 5.1.1 Physical Testing

- 5.2 By Packaging Material

- 5.2.1 Plastic

- 5.2.2 Glass

- 5.2.3 Metal

- 5.2.4 Paper & Board

- 5.2.5 Layer Packaging

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Spain

- 5.3.2.2 United Kingdom

- 5.3.2.3 Germany

- 5.3.2.4 France

- 5.3.2.5 Italy

- 5.3.2.6 Russia

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 South Africa

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Active Companies

- 6.2 Most Adopted Strategies

- 6.3 Market Share Analysis

- 6.4 Company Profiles

- 6.4.1 SGS SA

- 6.4.2 Bureau Veritas Group

- 6.4.3 Intertek Group plc

- 6.4.4 Merieux NutriSciences Corporation

- 6.4.5 TUV SUD South Asia Pvt. Ltd.

- 6.4.6 Eurofins Scientific

- 6.4.7 Microbac Laboratories Inc.