|

市場調査レポート

商品コード

1444809

スペシャルティスナック:市場シェア分析、業界動向と統計、成長予測(2024年~2029年)Specialty Snacks - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| スペシャルティスナック:市場シェア分析、業界動向と統計、成長予測(2024年~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

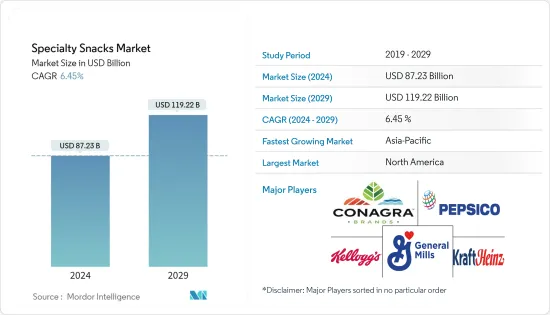

スペシャルティスナック市場規模は、2024年に872億3,000万米ドルと推定され、2029年までに1,192億2,000万米ドルに達すると予測されており、予測期間(2024年~2029年)中に6.45%のCAGRで成長します。

主なハイライト

- 中期的には、消費者の行動パターンのパラダイムシフトに伴い、スナック食品が本格的な食事の代替品として台頭すると予想されています。権限のある消費者が、外出先でのライフスタイルを活性化するために、美味しくて栄養価が高く、持続可能な食品をますます求めるようになっており、スナックの様相は変わりつつあります。利便性と携帯性への需要が消費の増加に拍車をかけているため、間食が増加しています。プレミアム化により、新鮮で体に良い、入手可能なスナックの革新と多様性が促進されています。

- 健康的なライフスタイルへの関心の高まりにより、現代の消費者はよりシンプルで健康的な配合、味、食事形式を求めており、市場の成長に大きく貢献しています。ナッツと種子は、高たんぱく質とエネルギー含有量の両方を提供するという健康的な評判があります。ナッツや種子をベースにしたスナックを提供するブランドの数が増えており、製品ラインに原材料として種子とナッツを組み込むことで製品革新に取り組んでいます。

- 消費者は、繊維質、タンパク質、全粒穀物を豊富に含むスナックなど、より健康的な食材を選ぶことが増えています。消費者の需要に応えるために、メーカーはスナックの脂肪削減に重点を置き、トランスフリーのスナックも提供しています。

- したがって、スナックバー、ビスケット、プロテインバー、エネルギーバー、フルーツベースのスナックなどの栄養食品に移行する人口の割合が大幅に増加しました。これは、ポテトチップスや押し出しスナックなどの風味豊かなスナックの潜在的な代替品となる便利な栄養製品への関心が高まっているためです。さらに、ビスケット、クッキー、クラッカー、ビスケットウエハースなどの焼き菓子には、かなりのカロリーが含まれています。この要因により、消費者はフルーツスナック、グラノーラバー、エネルギーバー、菓子などの健康的な代替製品に移行します。さらに消費者は、揚げ物や焼き製品による健康への悪影響を目の当たりにしており、その結果、世界中の成人と子供の間で肥満や糖尿病が増加しています。したがって、世界的に特殊スナック市場の潜在力は高いです。

スペシャルティスナック市場動向

便利で健康的な間食への需要の高まり

- 社会経済パターンの変化、飲食費の増加、健康食品への意識、食事パターンや既存の食習慣の変化、新製品を味わいたいという欲求の高まりなどにより、世界的にインスタント食品への需要が急速に高まっています。ナッツや種子などのスナックには多くの健康上の利点があるため、消費者にとって人気のある健康的なスナックの選択肢となっています。

- アーモンド、ヘーゼルナッツ、カシューナッツ、クルミ、ピスタチオなどの木の実、チアシードや亜麻仁などの種子は、独特の組成を持つ栄養価の高い食品です。それらは、神聖化に傾いている健康志向の消費者の毎日の食事への主要な追加となっています。

- さらに、ポップコーンや栄養強化チップスのような風味豊かなスナックは、外出先での軽食のコンセプトを簡単に摂取できるものであり、比較的扱いやすいものです。また、ポップコーン、ナッツや種子、押し出し成形されたスナックは、休憩の合間や料理をする時間がないときに理想的な食べ物として役立つため、人々がジャンクフードに飢えすぎてしまうのを防ぐのに役立ちます。

- ナッツや種子のスナックを定期的に摂取すると、心血管疾患や冠状動脈性心疾患を発症するリスクが軽減されます。アーモンドなどの高タンパク食品に対する消費者の需要は高く、現在最もダイナミックな動向である体重管理に向けて急速に勢いを増している栄養特性を備えています。さらに、ナッツは便利で持ち運びが容易で、多用途です。高たんぱく質の動向により、健康的なスナックの代表としてのナッツの地位が高まる可能性があります。

- 西ケープ州政府によると、南アフリカの男性の約31%、女性の68%が肥満であるため、南アフリカの肥満統計は憂慮すべきものです。過体重または肥満は、糖尿病や心臓病などのさまざまな生活習慣病を引き起こす可能性があります。これは大人と子供にとって大きな問題であり、6歳から14歳までの南アフリカの子供の13%以上が過体重または肥満であると考えられています。したがって、消費者は、比較的油分が少なく健康的で、健康的な食生活を維持するのに同様に有益である可能性のあるナッツや種子、焼いたりローストしたスナックを求めています。その結果、企業は、オーツ麦、ドライフルーツ、ベリー、トウモロコシなどの繊維質の成分を含めて食事の質を向上させながら、栄養摂取量を増やし、エネルギーレベルを維持し、消費者に健康的な選択肢を豊富に提供する可能性のある製品を開発することになりました。味に妥協することなく。

北米が市場を独占

- 健康意識の高まりとライフスタイルの変化は、米国の特製スナック市場の成長に寄与する2つの要因であり、北米は特製スナックの主要消費市場の1つとなっています。過去数年間で、米国ではスナックシリアルバーを使用する世帯数が50%増加し、噛み応えのあるグラノーラスナックバーの需要が顕著に増加しています。

- 米国の消費者は食品の製造に使用される原材料の産地や品質に懸念を抱いており、健康志向の消費者の間でオーガニックスナックバーの人気が高まっています。この国でスナックバーを探している消費者のほとんどは、ポリッジポット、シリアルバー、その他の朝食代替品など、特定の朝食オプションを利用する習慣を身につけたミレニアル世代です。これは、多忙なライフスタイル、意識の高まり、若い世代における肥満、糖尿病、アテローム性動脈硬化症、脳卒中などのいくつかのライフスタイル疾患の有病率の増加によるものです。たとえば、HRSA(NSCH)と肥満州が2022年に発表した報告書によると、2019年から2020年にかけて、10歳から17歳までの肥満の児童および青少年の割合が最も多い州は、米国の他の州の中でもケンタッキー州でした。

- したがって、この地域では、メーカーは製品をオンラインで入手できるようにするなど、消費者にとってより便利なショッピングオプションを備えた健康的な製品の革新に焦点を当てています。たとえば、2021年9月、米国に拠点を置くマザーアースズスナック社は、「体に良い」スナックのプレミアムQ-9スーパーフードラインを含む、消費者直販の健康的なスナックラインを発売しました。同社は、Q-9スーパーフードラインの主成分は100%キヌアであると主張しています。このスーパーフードには、体内で生成できない必須アミノ酸9種類すべてが含まれているため、食事から摂取する必要があります。この製品には、ほうれん草パルメザン、クラシックランチ、ゼスティチリライム、ホワイトチェダーの4つのフレーバーがあります。バニラヨーグルト入りのホワイトチョコレートとダークイタリアンチョコレートの両方が、同社の認定オーガニック、クリスピーなスティクス、そして小さめのバイツの詰め物として提供されています。さらに、Mother EarthのQ-9スーパーフードスナックには、その製品がオーガニック、グルテンフリー、コーシャ、非遺伝子組み換え、ベジタリアンフレンドリーであることが認定されており、幅広い食事上の懸念を満たすことが記載されています。したがって、オーガニックおよびクリーンラベルの特製スナックは、この地域で重要な市場を占めています。

スペシャルティスナック業界の概要

世界の特製スナック市場は競争が激しく、ケロッグ、ネスレ、コナグラブランズ、ペプシコ、ゼネラルミルズなどの企業が主要な市場シェアを獲得しています。小規模企業は、競争市場での地位を確立するためにイノベーションを開発し、新製品を発売しています。大手企業は市場リーダーであり続けるために、地理的範囲と製品ポートフォリオを拡大しています。さらに、主要企業は、各製品の機能的利点を提供しながら、革新的でエキゾチックなフレーバーを消費者に提供することに広範囲に焦点を当てています。したがって、イノベーションによる持続的な競争上の優位性は、市場の主要企業が市場シェアを獲得するための主な戦略です。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の成果 と調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 製品タイプ

- スナックバー

- ベーカリーベースのスナック

- ナッツとシードのスナック

- ポップスナック

- その他の製品タイプ

- 流通チャネル

- スーパーマーケット/ハイパーマーケット

- コンビニ/食料品店

- オンライン小売店

- その他の流通チャネル

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- その他北米

- 欧州

- スペイン

- 英国

- ドイツ

- フランス

- イタリア

- ロシア

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- その他アジア太平洋

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- その他中東・アフリカ

- 北米

第6章 競合情勢

- 最も採用されている戦略

- 市場シェア分析

- 企業プロファイル

- The Kraft Heinz Company

- Conagra Brands Inc.(SlimJim)

- General Mills Inc.

- The Kellogg Company

- PepsiCo Inc.

- Mars Incorporated

- Blue Diamond Growers

- Nestle SA

- Mondelez International

- Intersnack Group GmbH

第7章 市場機会と将来の動向

第8章 出版社について

The Specialty Snacks Market size is estimated at USD 87.23 billion in 2024, and is expected to reach USD 119.22 billion by 2029, growing at a CAGR of 6.45% during the forecast period (2024-2029).

Key Highlights

- Over the medium term, snack food is expected to emerge as an alternative to full-fledged meals with a paradigm shift in consumer behavior patterns. The face of snacks is changing as empowered consumers increasingly seek tasty, nutritional, and sustainable foods to fuel their on-the-go lifestyles. Snacking is rising as the demand for convenience and portability has fueled increased consumption, with premiumization spurring innovation and variety in fresh, better-for-you, and available snacks.

- Due to the growing interest in healthy lifestyles, modern consumers are seeking simpler and healthier formulations, flavors, and diet formats, significantly contributing to the market's growth. Nuts and seeds have a healthy reputation for delivering both high protein and energy content. An increasing number of brands that offer nut- and seed-based snacks are engaging in product innovation by integrating seeds and nuts as ingredients in their product lines.

- Consumers are increasingly opting for healthier ingredients, such as snacks high in fiber, protein, and whole grains. To cater to consumer demand, manufacturers are focusing on fat reduction in their snacks and are even offering trans-free snacks.

- Therefore, there has been a significant rise in the percentage of the population shifting toward nutritional food products, such as snack bars, biscuits, protein bars, energy bars, and fruit-based snacks. This has resulted because of the growing interest in convenient nutritional products that can be potential alternatives for savory snacks like potato chips and extruded snacks, among others. Additionally, baked products like biscuits, cookies, crackers, and biscuit wafers, among others, have a significant amount of calories. This factor makes consumers shift to healthy alternative products like fruit snacks, granola bars, energy bars, and confectioneries. Moreover, consumers are witnessing ill effects on health due to fried and baked products, resulting in the rise of obesity and diabetes among adults and children across the globe. Hence, there is high potential for a specialty snacks market globally.

Specialty Snacks Market Trends

Growing Demand for Convenient and Healthy Snacking

- Globally, the demand for convenience foods is growing faster due to changes in social and economic patterns, increased expenditure on food and beverage, awareness of healthy foods, changes in meal patterns and existing food habits, and an increased desire to taste new products. Owing to the numerous health benefits associated with snacks like nuts and seeds, they have become popular and healthy snacking options for consumers.

- Tree nuts, such as almonds, hazelnuts, cashew nuts, walnuts, and pistachios, as well as seeds, such as chia seeds and flaxseeds, are nutrient-dense foods with unique compositions. They have become a major addition to the daily diets of health-conscious consumers inclined toward sanctification.

- Moreover, the on-the-go snacking concept is linked to easy consumption and is relatively easier to handle, which savory snacks like popcorn and fortified chips offer. Also, popcorn, nuts and seeds, and extruded snacks can help prevent people from getting too hungry for junk foods, as these serve as ideal eatables between breaks or when people do not have time to cook.

- Regular consumption of nut and seed snacks reduces the risk of developing cardiovascular diseases or coronary heart diseases. There is high consumer demand for foods high in protein, such as almonds, which have nutritional attributes that are fast gaining momentum for weight management, which is the most dynamic trend currently. In addition, nuts are convenient, portable, and versatile. The high protein trend is likely to boost the position of nuts as a leading healthy snack choice.

- According to Western Cape Government, obesity stats in South Africa are concerning, as roughly 31% of men and 68% of women in the country are obese. Being overweight or obese can lead to various lifestyle diseases, including diabetes and heart disease. This is a big problem in adults and children, with more than 13% of South African children between the ages of 6-14 years considered overweight or obese. Therefore, consumers demand nuts and seeds and baked or roasted snacks that are comparatively less oily and healthier and could be equally beneficial in maintaining a healthy diet. This has resulted in companies creating products with the potential to increase nutritional intakes, sustain energy levels, and offer plenty of healthy options to the consumers while improving the quality of diet with the inclusion of fibrous ingredients like oats, dried fruits, berries, and corn, without compromising on taste.

North America Dominates the Market

- Increasing health consciousness and changing lifestyles are the two factors contributing to the growth of the specialty snacks market in the United States, making North America one of the leading consumer markets for specialty snacks. In the past few years, the United States experienced a 50% increase in the number of households using snack cereal bars, and there has been a noticeable rise in demand for chewy granola snack bars.

- As consumers in the United States are concerned about the origin and quality of ingredients used in the preparation of food products, the popularity of organic snack bars has been increasing among health-conscious consumers. Most consumers looking for snack bars in the country are millennials who have developed a habit of specific breakfast options, including porridge pots, cereal bars, and other breakfast alternatives. This is due to hectic lifestyles, increased awareness, and the rising prevalence of several lifestyle conditions, including obesity, diabetes, atherosclerosis, and stroke among younger generations. For instance, according to a report published in 2022 by HRSA (NSCH) and the State of Obesity, the state with the greatest percentage of obese children and adolescents between the ages of 10 and 17 was Kentucky, among other states in the United States, during 2019-2020.

- Therefore, in this region, manufacturers focus on healthy product innovations with more convenient shopping options for consumers, such as making their products available online. For instance, in September 2021, Mother Earth's Snack launched the Direct-to-consumer healthy snack line, including its premium Q-9 SuperFood line of "better-for-you" snacks. It is a United States-based company. The company claims that the Q-9 SuperFood line has a primary component of 100% quinoa. This superfood contains all nine essential amino acids the body cannot produce and must therefore be obtained through diet. The product is available in four flavors Spinach Parmesan, Classic Ranch, Zesty Chili Lime, and White Cheddar. Both white chocolate with vanilla yogurt and dark Italian chocolate are offered as fillings for the company's Certified Organic, crispy Styx, and smaller Bites. Further, Mother Earth's Q-9 SuperFood snacks state that its products are certified organic, gluten-free, kosher, non-GMO, and vegetarian-friendly to satisfy a wide range of dietary concerns. Hence, organic and clean-label specialty snacks have a significant market in this region.

Specialty Snacks Industry Overview

The global specialty snacks market is highly competitive, with players such as Kellogg's, Nestle, Conagra Brands, PepsiCo, General Mills, and others capturing a major market share. Small players are developing innovations and new product launches to make their mark in the competitive market. Major players are expanding their geographical reach and product portfolio to remain market leaders. Moreover, key players focus extensively on providing consumers with innovative and exotic flavors while offering functional benefits in each product. Thus, a sustainable competitive advantage through innovation is the main strategy for gaining market share by the major players in the market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables and Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Product Type

- 5.1.1 Snack Bars

- 5.1.2 Bakery-based Snacks

- 5.1.3 Nuts and Seeds Snacks

- 5.1.4 Popped Snacks

- 5.1.5 Other Product Types

- 5.2 Distribution Channel

- 5.2.1 Supermarkets/Hypermarkets

- 5.2.2 Convenience/Grocery Stores

- 5.2.3 Online Retailer Stores

- 5.2.4 Other Distribution Channels

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Spain

- 5.3.2.2 United Kingdom

- 5.3.2.3 Germany

- 5.3.2.4 France

- 5.3.2.5 Italy

- 5.3.2.6 Russia

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 South Africa

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 The Kraft Heinz Company

- 6.3.2 Conagra Brands Inc. (SlimJim)

- 6.3.3 General Mills Inc.

- 6.3.4 The Kellogg Company

- 6.3.5 PepsiCo Inc.

- 6.3.6 Mars Incorporated

- 6.3.7 Blue Diamond Growers

- 6.3.8 Nestle SA

- 6.3.9 Mondelez International

- 6.3.10 Intersnack Group GmbH