|

市場調査レポート

商品コード

1939634

スマート水道メーター:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Smart Water Meter - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| スマート水道メーター:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年02月09日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

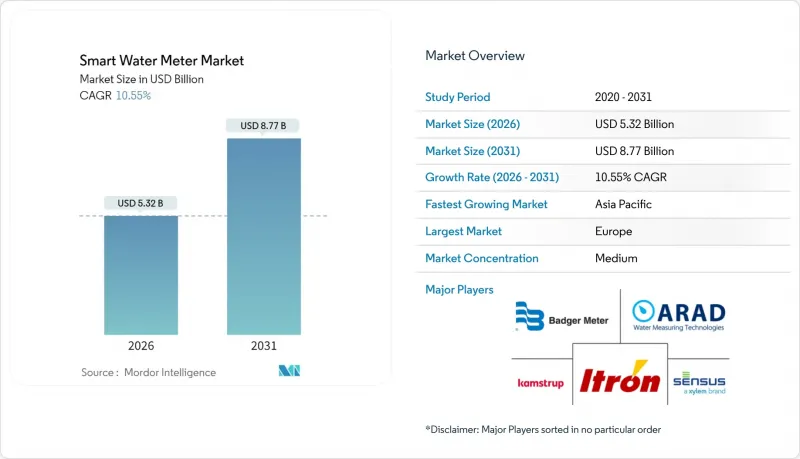

スマート水道メーター市場は、2025年に48億1,000万米ドルと評価され、2026年の53億2,000万米ドルから2031年までに87億7,000万米ドルに達すると予測されています。

予測期間(2026-2031年)におけるCAGRは10.55%と見込まれています。

公益事業者は、機械式メーターから、リアルタイム監視、自動課金、データ駆動型の漏水検知を可能にする接続デバイスへの移行を継続しています。節水に関する規制要件、老朽化した配水設備の交換に対する圧力の高まり、およびモノのインターネット(IoT)プラットフォームの拡大が相まって、公益事業クラス全体での導入を加速させています。ベンダー間の競合は、分析機能と双方向通信の統合に焦点を当てつつ、有利な総所有コスト(TCO)を維持することに集中しています。節約分に応じて支払うモデルなどの資金調達オプションの拡大や、検証済みの漏水削減を評価する実績ベースの規制は、先進国および新興国における需要パイプラインをさらに強化します。

世界のスマート水道メーター市場の動向と洞察

支援的な政府規制

義務的な導入スケジュールと水効率基準は、コンプライアンスと報告要件を満たす先進的な計測ソリューションへの移行を公益事業者に促しています。EU飲料水指令はエンドツーエンドの監視を要求しており、これを受けてドイツとフランスでは新築および大規模改修物件へのスマートメーター設置を規定しています。カリフォルニア州の恒久的な水使用規則は執行のための詳細なデータを要求しており、AMI導入が資金調達適格の前提条件となっています。水道事業者は、漏水削減や顧客エンゲージメント向上の実績を文書化することで費用回収メカニズムを獲得し、投資リスクを低減するとともに全域展開を支援します。ベンダーは大量発注による単価低減の恩恵を受け、政策立案者は節水進捗を追跡する透明性の高いパフォーマンス指標を確保します。自治体、地域、国家レベルを問わず、規制はスマート水道メーター市場の広範な普及に必要な長期的な確実性を保証します。

水利用効率向上の必要性

水不足地域における水道事業者は、接続型メーターを導入することで高消費パターンを特定し、行動変容を支援する時間単位のデータを提供することで顧客の自主性を促進します。連続遠隔計測を利用する産業施設では、漏水箇所の特定とプロセス最適化により20~30%の消費削減が報告されています。土壌水分感知と気象ベースの灌漑スケジュールを組み合わせた農業パイロット事業では最大28%の節水効果を記録し、分野横断的な有用性を実証しています。効率化による利益はエネルギー節約にもつながります。水生産と揚水は大きな運営費を占めるためです。分析アプリケーションによる需要予測により、水道事業者は需要のピークを平準化し、設備拡張を先送りできます。水道事業者が節水と収益の分離を結びつけることで、効率化の利益は安定した財務実績に変換され、スマート水道メーター市場を推進します。

初期費用の高さとサイバーセキュリティリスク

完全なAMI導入にはエンドポイントあたり200~400米ドルの費用がかかり、資本予算が限られる公益事業体にとって課題となります。料金改定の承認には数年を要する場合があり、プロジェクト開始が遅れることがあります。サイバーセキュリティ対策、暗号化、侵入検知、24時間監視により、プロジェクト総費用がさらに15~25%増加します。小規模システム、特に発展途上国では、優遇融資がなければ投資が先送りされることが多々あります。注目を集めるサイバーインシデントは規制当局の監視を強化し、コンプライアンスコストをさらに押し上げます。これらの要因は、資金調達メカニズムが成熟しセキュリティフレームワークが標準化されるまで、スマート水道メーター市場の成長を全体的に抑制します。

セグメント分析

自動検針システム(AMR)は2025年時点でスマート水道メーター市場シェアの57.10%を占め、その確固たる基盤とコスト効率の高い一方向データ伝送を反映しています。多くの公益事業者は近代化の初期段階でAMRを採用します。これは、大規模なネットワーク構築を必要とせず、走行中の検針により人件費を大幅に削減できるためです。AMRに関連するスマート水道メーター市場規模は依然として大きいもの、第二世代の導入では双方向アーキテクチャが優先されるため、その成長は緩やかになっています。

高度計量インフラ(AMI)は、水道事業者がリアルタイム漏水警報、遠隔遮断、時間変動型料金体系を求めることから、2031年までにCAGR11.55%を記録します。セルラー、NB-IoT、LoRaWANモジュールのコスト低下により、AMI導入の主要障壁が解消されました。サービスプロバイダーは、メーター、分析ツール、ソフトウェアサブスクリプションをパッケージ化し、資本コストを運営予算に分散させています。豊富なデータを提供するAMIプラットフォームは節水プログラムとの連携が容易であり、地域的な普及を加速させ、スマート水道メーター市場の拡大に寄与します。

住宅向け導入は、欧州および北米における新規住宅へのスマートメーター設置義務化を受け、2025年にはスマート水道メーター市場規模の58.00%を占めました。消費者は節水目標と具体的な節約効果を結びつける使用量ポータルを活用でき、安定した更新サイクルが維持されています。

商業ビルでは、水道・エネルギー・空調データを連携させる施設管理ソフトウェアの普及により、11.85%のCAGRで最も急速な導入が進んでいます。高層ビルの所有者は、運営費削減とグリーンビル認証取得により投資効果を正当化しています。小売チェーンやホテルグループは、サイト間比較分析、隠れた漏水の発見、灌漑の最適化に分析技術を応用しています。サステナビリティ報告枠組みの強化に伴い、企業ユーザーの導入拡大がスマート水道メーター市場全体の成長を後押ししています。

本スマート水道メーター市場レポートは、技術別(自動検針・高度計量インフラ)、用途別(住宅用など)、メータータイプ別(機械式/タービン式、超音波式、電磁式)、通信技術別(無線周波数、LoRaWAN/その他LPWANなど)、構成要素別(ハードウェア、ソフトウェア・分析、サービス)、導入形態別(新規設置、改修/交換)、地域別に分析しております。

地域別分析

欧州は2025年に36.10%の収益シェアでスマート水道メーター市場を牽引しました。これは、水損失の追跡と透明性のある請求を義務付けるEU指令に支えられています。各国の実施ロードマップにより安定した入札案件が保証され、長期的なベンダー枠組みが調達を効率化しています。公益事業者はまた、気候変動への耐性強化を目的とした復興資金を活用し、地域全体の安定した需要を支えるAMI(高度計量インフラ)の導入を加速させています。

アジア太平洋地域は2031年までに12.05%のCAGRで最速の拡大を記録しています。中国では大規模なスマートシティ実証事業において、地域デジタルツインに計測機能を組み込んでいます。一方、インドの「ジャル・ジーヴァン・ミッション」は、スマート端末を含む農村部接続の資金調達を行っています。インドネシアやベトナムなどの東南アジア諸国では、急速な都市化に伴いレガシー資産のアップグレードが同時進行し、旧式技術に紐づく沈没コストを回避しています。政府補助金、多国間融資、官民連携が相まって設置規模が拡大し、スマート水道メーター市場が成長しています。

北米では老朽化したインフラの更新と州全体の節水義務化が追い風となっています。カリフォルニア州の公益事業会社は、一人当たり使用量制限の実施や遠隔遮断機能による山火事耐性強化のため、AMIを導入しています。カナダでは、非収益水回収に焦点を当てた州レベルの近代化プログラムが推進され、漸進的な成長が見込まれます。ラテンアメリカのブラジルにおけるコンセッション入札は、今後大きな機会が到来することを示唆しています。一方、中東・アフリカの公益事業者は、資金調達状況や通信ネットワークの準備状況により導入進捗は異なりますが、水不足への対応や盗水防止のためにスマートメーターを活用しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 政府の支援的規制

- 水利用効率の向上が必要です

- 非収益水(NRW)損失の削減

- スマートシティとIoTプラットフォームの統合

- 節約分に応じて支払うファイナンスモデル

- 干ばつによる節水義務化

- 市場抑制要因

- 初期費用の高さとサイバーセキュリティリスク

- システム統合の複雑性

- 公益事業データ分析人材の不足

- 超音波式ユニットにおける電池寿命の限界

- 業界バリューチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- スマートメーターの投資利益率(ROI)分析

- プロトコルのベンチマーク比較

- LoRaWANの導入手順と使用事例

- 公益事業デジタル化のメリット

- マクロ経済的要因が市場に与える影響

第5章 市場規模と成長予測

- 技術別

- 自動検針システム(AMR)

- 高度計量インフラ(AMI)

- 用途別

- 住宅

- 商業

- 産業

- 農業

- メータータイプ別

- 機械/タービン

- 超音波

- 電磁気

- 通信技術別

- 無線周波数(独自開発のRF技術)

- LoRaWAN/その他のLPWAN

- セルラー通信(NB-IoT/LTE-M)

- 有線(M-Bus/イーサネット)

- コンポーネント別

- ハードウェア

- ソフトウェアおよびアナリティクス

- サービス

- 展開別

- 新規導入

- 改修/交換

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- チリ

- その他南米

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- マレーシア

- シンガポール

- オーストラリア

- その他アジア太平洋地域

- 中東・アフリカ

- 中東

- アラブ首長国連邦

- サウジアラビア

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- その他アフリカ

- 中東

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Arad Ltd.

- Badger Meter Inc.

- Itron Inc.

- Sensus USA Inc.(Xylem Inc.)

- Kamstrup A/S

- Diehl Stiftung and Co. KG

- Zenner International GmbH and Co. KG

- Landis+Gyr Group AG

- Honeywell International Inc.

- Neptune Technology Group Inc.(Roper)

- Aclara Technologies LLC(Hubbell)

- Apator SA

- Axioma Metering

- B Meters Srl

- Datamatic Inc.

- Maddalena S.p.A.

- Suntront Tech Co., Ltd.

- Mueller Systems LLC

- Waviot

- Watertech S.p.A.(Arad)

- Jiangxi Sanchuan Water Meter Co. Ltd.

- Ningbo Water Meter Co. Ltd.

- BETAR Company

- Integra Metering AG

- IESLab Electronic Co. Ltd.