スマート水道メーター市場の機会、成長要因、業界動向分析、および2026年~2035年の予測

Smart Water Meter Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035- 発行日

- ページ情報

- 英文 135 Pages

- 納期

- 2~3営業日

- 商品コード

- 2019158

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

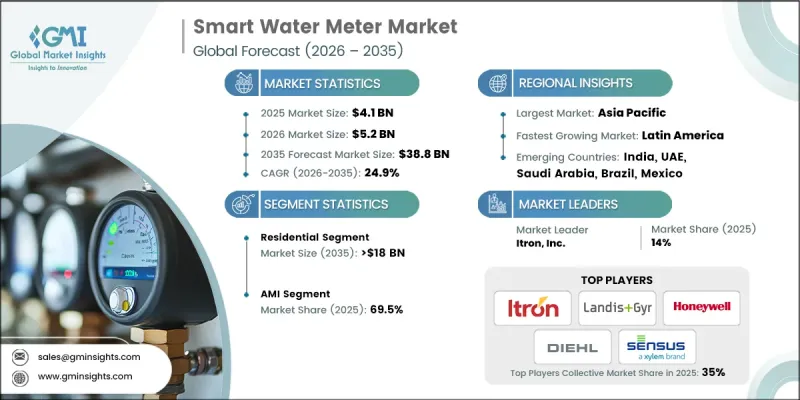

世界のスマート水道メーター市場は、2025年に41億米ドルと評価され、2035年までにCAGR24.9%で成長し、388億米ドルに達すると推定されています。

この急成長は、急速な技術進歩、節水取り組みの拡大、規制上の義務、そしてより効率的な水管理システムの必要性によって牽引されています。世界中の水道事業者や都市は、配水の最適化、浪費の最小化、および運用効率の向上を図るため、スマート水道メーターを導入しています。従来型のメーターは、時間がかかり、誤りの生じやすい手動検針に依存することが多いため、水使用量の正確かつリアルタイムなモニタリングに対する需要が、主要な成長要因となっています。IoT技術と統合されたスマートメーターは、遠隔監視、自動請求、リアルタイムのデータ収集を可能にし、効率とサービス品質を向上させます。特に水不足に悩む地域において、節水や漏水検知を促進する政府の政策やインセンティブプログラムが、導入をさらに加速させています。また、特に水インフラの近代化が不可欠な新興経済国において、デジタル化の取り組みや持続可能性の目標が高まっていることも、市場の成長を支えています。

| 市場の範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測期間 | 2026年~2035年 |

| 開始時点の市場規模 | 41億米ドル |

| 予測額 | 388億米ドル |

| CAGR | 24.9% |

住宅部門は、水やエネルギーの管理改善、正確な請求の実現、再生可能エネルギーの統合を支援するため、スマートメーターの消費者による導入が進むことを背景に、2035年までに180億米ドルに達すると予想されています。家庭用スマートメーターは、正確な使用状況の把握を可能にし、消費者が消費量を管理できるようにするとともに、ホームオートメーションシステムとシームレスに連携することで、市場の成長に寄与しています。

AMI(高度計量インフラ)セグメントは、双方向通信機能を備えていることから、AMR(自動検針)システムを上回り、2025年には69.5%のシェアを獲得しました。AMIにより、公益事業者はリアルタイムデータの収集、メーターの遠隔管理、漏水の迅速な検知、異常への迅速な対応が可能になります。スマートグリッドやデジタル水管理ソリューションとの統合は、その優位性をさらに強固なものにし、効率的な公益事業運営のための最適な技術となっています。

2025年、米国のスマート水道メーター市場規模は7億400万米ドルと評価されました。同国では、人口増加、インフラの老朽化、気候変動の影響により、複数の地域で水不足が深刻化しています。米国の公益事業者は、消費量をリアルタイムで監視し、漏水を特定し、異常な使用パターンを検知するためにスマートメーターの導入を拡大しており、節水と運営効率の向上を図っています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 規制情勢

- 地域別価格動向分析(米ドル/単位)

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

- 新たな機会と動向

- デジタル化とIoTの統合

- 新興市場への進出

- 投資分析と将来展望

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析:地域別

- 北米

- 欧州

- アジア太平洋地域

- 中東・アフリカ

- ラテンアメリカ

- 戦略的取り組み

- 競合ベンチマーキングの図解

- 戦略ダッシュボード

- イノベーションおよび技術動向

第5章 市場規模・予測:用途別、2022-2035

- 住宅用

- 商業用

- 公益事業

- AMI

- AMR

第6章 市場規模・予測:製品別、2022-2035

- 温水メーター

- 冷水メーター

第7章 市場規模・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スウェーデン

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

- エジプト

- ラテンアメリカ

- ブラジル

- アルゼンチン

第8章 企業プロファイル

- ABB

- Apator S.A.

- Arad Group:

- Badger Meter, Inc.

- BMETERS S.r.l

- Diehl Stiftung & Co. KG

- Honeywell International Inc.

- Itron Inc.

- Kamstrup

- Landis+Gyr

- Neptune Technology Group Inc.

- Ningbo Water Meter Co., Ltd.

- Schneider Electric

- Siemens

- Sontex SA

- Xylem(Sensus)

- ZENNER International GmbH & Co. KG

- Suez

- Baylan Water Meters

- BOVE Technology

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 135 Pages

- 納期

- 2~3営業日