|

市場調査レポート

商品コード

1693451

トマト種子:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Tomato Seed - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| トマト種子:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 465 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

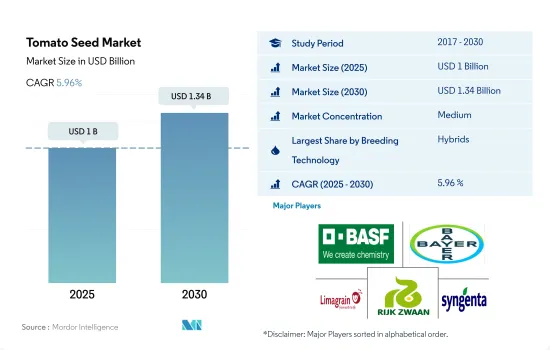

トマト種子市場規模は2025年に10億米ドルと推計され、2030年には13億4,000万米ドルに達し、予測期間中(2025-2030年)のCAGRは5.96%で成長すると予測されます。

高収量と耐病性特性によりハイブリッドが市場を席巻

- トマトは世界的に栽培されている主要な野菜作物のひとつです。加工用および生食用トマトの需要の結果、2022年には世界の野菜種子市場の12.4%を占めました。

- 2022年には、開放受粉品種とハイブリッド派生品種が世界のトマト種子市場の27.2%を占めました。これは有機栽培の増加や在来品種への嗜好により増加すると予想されます。

- アジア太平洋は、開放受粉品種とハイブリッド派生品種を用いたトマト栽培の最大地域で、2022年には58.3%を占めました。これは新興諸国における露地受粉品種の使用の増加と、ハイブリッド品種よりもその味と品質が好まれた結果です。

- ハイブリッド・セグメントは世界のトマト種子市場の72.8%を占め、消費量の増加と加工産業からの需要により、OPVと比較して速いペースで成長しています。また、保護された構造において、適応性の高いハイブリッドの使用も増加しています。

- アジア太平洋地域は世界のハイブリッドトマト種子市場で最大のシェアを占めており、2022年には約43%を占めたが、これは同地域で利用可能な新しい先端技術が理由です。中国は保護栽培の世界的リーダーであり、保護栽培に使用できるのはハイブリッド種子のみです。

- Syngenta、Bayer AG、Rijk Zawannなどの大手企業は、耐病性形質、貯蔵期間の延長、幅広い適応性、高収量、強靭な茎、耐亀裂性、高樹勢を備えた新しいハイブリッドを開発しています。有機栽培と生鮮部門の消費の増加も、予測期間中、開放受粉品種トマト種子市場を牽引すると予想されます。

アジア太平洋は栽培面積の多さと保護栽培の採用によりトマト種子の主要市場となっている

- トマトは世界的に最も人気のある野菜であり、2021年の総生産量は約1億8,910万トンでした。世界の野菜生産量の約16.4%を占めています。2022年には、トマト種子市場は世界の野菜種子市場の12.4%を占め、これは世界最大の野菜種子市場の1つと考えられています。これはトマトが様々な調理法で最も消費される野菜であることと関連しています。

- 2022年には、アジア太平洋が最大のトマト種子市場であり、世界のトマト種子市場の47.3%を占めました。国内および国際市場における消費と市場価値の増加により、さらに成長すると予想されます。この地域では、中国がトマト種子市場の最大国で、2022年には世界のトマト種子市場の23.5%を占める。ハイブリッドの利用可能性の増加に伴い、トマトのほとんどは温室で栽培されており、2022年の中国のトマト総生産量の50%以上を占めています。

- 北米はトマト種子市場において2番目に大きな地域で、2022年には世界のトマト種子市場の21.4%を占める。米国は世界最大のトマト消費国です。

- 世界中でトマトの生産にハイブリッド種子が使用されるようになり、ハイブリッドトマト種子の需要が増加しました。2022年、ハイブリッド種子は世界のトマト種子市場の72.7%を占める。

- 主要生産国における保護栽培面積の増加、加工産業および消費用需要の増加が世界のトマト種子市場を牽引し、予測期間中にCAGR 6.1%を記録すると予測されます。

世界のトマト種子市場の動向

様々な産業からのトマト需要の増加と消費の拡大がトマト栽培面積を牽引

- トマトは世界的に栽培・消費されている主要な野菜作物の1つです。トマトの栽培面積は2017年から2022年の間に全体で8.0%増加しました。この増加は主に、様々な食品加工産業からの需要の増加と世界の消費の増加に起因しています。

- アジア太平洋は260万haと最大のトマト栽培面積を有し、2022年の世界のトマト栽培面積の約47.1%を占める。この地域で主要なトマト栽培面積を持つ国のトップは中国とインドで、2022年にはそれぞれ110万haと80万haとなります。中国とインドはトマト生産量世界トップであり、膨大な国内需要と輸出需要があります。アフリカは第2位の地域で、2022年の世界のトマト栽培面積の28.7%を占める。アフリカでは、2017年から2022年にかけて栽培面積が14.5%増加しました。ナイジェリアは、同国での需要の高まりにより、2022年に同地域のトマト栽培面積全体の54.8%を占めました。

- 2022年、欧州は世界のトマト作付面積の10.6%を占めました。最大の国はトルコで、同年の欧州全体のトマト作付面積の28.2%を占めています。トルコは世界最大級のトマト生産国です。さらに、北米は2022年に世界のトマト作付面積の4.1%を占めました。米国が主要国で、同年の同地域のトマト栽培面積の約49.4%を占めています。南米は2022年に世界のトマト栽培面積の2.2%を占めました。ブラジルのみで、同年の同地域のトマト総栽培面積の42%以上を占めています。様々な産業からのトマト需要の増加が、予測期間中のトマト作付面積を世界的に牽引すると予想されます。

拡大するトマト種子市場の原動力は、耐病性で適応性の広い種子品種に対する需要の増加

- トマトは高付加価値作物であり、トマトピューレ、ケチャップなどの加工産業による需要が高いため、野菜の中でも最大級のセグメントです。Syngenta、Rijk Zwaan、Enza Zadenなどの大手企業は、葉巻ウイルスなどのウイルス性病害に耐性を持つトマトの種子品種を世界中で40%以上販売しています。

- トマトモザイクウイルス、トマト黄化葉巻ウイルス、花終腐敗病、うどんこ病、萎凋病、線虫などのウイルス性病害に対する抵抗性を持つ形質が、栽培に広く利用されています。アジア太平洋は最大のトマト生産地域の一つであり、Rijk Zwaan、East-West Seed、Namdhari Seedsなどの主要企業は、葉巻ウイルスなどのウイルス性病害に耐性を持つトマト種子品種をこの地域に保有しています。例えば、2022年にはRijk Zwaanがトマト茶色果実ウイルス(ToBRFV)に耐性を持つ新しいトマト種子品種を発売しました。さらに2022年には、HM.Limagrainの事業部門であるClauseは、伝播性の高いToBRFVに耐性のあるトマト品種を発表しました。

- 貯蔵期間の延長、均一性、割れ耐性、異なる土壌や気候条件への幅広い適応性を持つトマト品種は需要が高いです。バイエル、シンジェンタ、Rijk Zwaanなどの企業は、Kierano、Aurea、Angelle、Tontolle、Cheramy RZ F1などの種子品種を提供し、さまざまな農業条件で高品質のトマトを生産しています。

- 各社による、ウイルスに対する高い耐性、異なる気象条件への適応性、加工産業による高い需要を備えた新しいハイブリッド種子品種の導入は、予測期間中のトマト種子市場の成長に役立つと予想される要因です。

トマト種子産業の概要

トマト種子市場は適度に統合されており、上位5社で57.41%を占めています。この市場の主要企業は以下の通りです。 BASF SE, Bayer AG, Groupe Limagrain, Rijk Zwaan Zaadteelt en Zaadhandel BV and Syngenta Group(アルファベット順)

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 栽培面積

- 最も人気のある形質

- 育種技術

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 育種技術

- 雑種

- 開放受粉品種とハイブリッド派生品種

- 栽培メカニズム

- 露地栽培

- 保護栽培

- 地域

- アフリカ

- 育種技術別

- 栽培メカニズム別

- 国別

- エジプト

- エチオピア

- ガーナ

- ケニア

- ナイジェリア

- 南アフリカ

- タンザニア

- その他のアフリカ

- アジア太平洋

- 育種技術別

- 栽培メカニズム別

- 国別

- オーストラリア

- バングラデシュ

- 中国

- インド

- インドネシア

- 日本

- ミャンマー

- パキスタン

- フィリピン

- タイ

- ベトナム

- その他アジア太平洋地域

- 欧州

- 育種技術別

- 栽培メカニズム別

- 国別

- フランス

- ドイツ

- イタリア

- オランダ

- ポーランド

- ルーマニア

- ロシア

- スペイン

- トルコ

- ウクライナ

- 英国

- その他欧州

- 中東

- 育種技術別

- 栽培メカニズム別

- 国別

- イラン

- サウジアラビア

- その他中東

- 北米

- 育種技術別

- 栽培メカニズム別

- 国別

- カナダ

- メキシコ

- 米国

- 北米その他

- 南米

- 育種技術別

- 栽培メカニズム別

- 国別

- アルゼンチン

- ブラジル

- その他南米

- アフリカ

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Advanta Seeds-UPL

- BASF SE

- Bayer AG

- Bejo Zaden BV

- East-West Seed

- Groupe Limagrain

- Rijk Zwaan Zaadteelt en Zaadhandel BV

- Sakata Seeds Corporation

- Syngenta Group

- Yuan Longping High-Tech Agriculture Co. Ltd

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 世界市場規模とDRO

- 情報源と参考文献

- 図表リスト

- 主要洞察

- データパック

- 用語集

目次

Product Code: 92513

The Tomato Seed Market size is estimated at 1 billion USD in 2025, and is expected to reach 1.34 billion USD by 2030, growing at a CAGR of 5.96% during the forecast period (2025-2030).

Hybrids dominated the market due to the higher yield and disease resistance traits

- Tomato is one of the major vegetable crops cultivated globally. It accounted for 12.4% of the global vegetable seed market in 2022 as a result of the demand for tomatoes in processing and fresh consumption.

- In 2022, open pollinated varieties and hybrid derivatives accounted for 27.2% of the global tomato seed market. This is expected to increase due to the increase in organic cultivation and preference for native varieties.

- Asia-Pacific was the largest region for the cultivation of tomatoes by using open pollinated varieties and hybrid derivatives, accounting for 58.3% in 2022. This is a result of an increase in the usage of open pollinated varieties in developing countries and the preference for their taste and quality over hybrids.

- The hybrid segment accounted for 72.8% of the global tomato seed market, and it is growing at a faster rate compared to OPVs due to the increase in consumption and demand from processing industries. The usage of hybrids, which have higher adaptability, is also increasing in the protected structures.

- Asia-Pacific had the largest share of the global hybrid tomato seed market, and it accounted for about 43% in 2022 because of the new advanced technologies available in the region. China is a global leader in protected cultivation, and only hybrid seeds can be used for protected cultivation.

- Major companies, such as Syngenta, Bayer AG, and Rijk Zawann, are developing new hybrids with disease-resistant traits, increasing shelf life, wider adaptability, high yield, strong stem, crack resistance, and high vigor. The increase in organic cultivation and fresh segment consumption is also expected to drive the open pollinated varieties tomato seed market during the forecast period.

Asia-Pacific is the major market for tomato seeds due to high area under cultivation and the adoption of protected cultivation

- Tomato is the most popular vegetable globally, with an overall production of around 189.1 million metric ton in 2021. It represented around 16.4% of the global vegetable production. In 2022, the tomato seeds market accounted for 12.4% of the global vegetable seed market, which is considered to be one of the largest vegetable seed markets in the world. This is associated with tomatoes being the most consumed vegetable in various preparations.

- In 2022, Asia-Pacific was the largest tomato seed market, accounting for 47.3% of the global tomato seed market. It is expected to grow further due to the increase in consumption and market value in the domestic and international markets. In the region, China was the largest country in the tomato seed market, accounting for 23.5% of the global tomato seed market in 2022. With the increase in hybrid availability, most of the tomatoes are grown in greenhouses, which accounted for more than 50% of China's total tomato production in 2022.

- North America is the second-largest region in the tomato seed market, accounting for 21.4% of the global tomato seed market in 2022. The United States is the largest consumer of tomatoes globally.

- With the increased usage of hybrids in the production of tomatoes worldwide, the demand for hybrid tomato seeds increased. In 2022, hybrid seeds accounted for 72.7% of the global tomato seed market.

- An increase in protected cultivation acreage in major producing countries and an increase in the demand from processing industries and for consumption are anticipated to drive the global tomato seed market, registering a CAGR of 6.1% during the forecast period.

Global Tomato Seed Market Trends

The increase in demand for tomatoes from various industries and the growing consumption are driving the tomato cultivation area

- Tomato is one of the major vegetable crops cultivated and consumed globally. The overall area under cultivation of tomatoes increased by 8.0% between 2017 and 2022. This increase is mainly attributed to the growing demand from the various food processing industries and increasing consumption worldwide.

- Asia-Pacific holds the largest area under tomato cultivation with 2.6 million ha, accounting for about 47.1% of the global tomato acreage in 2022. China and India were the top countries with major tomato-cultivated areas in the region, with 1.1 million and 0.8 million ha, respectively, in 2022. China and India are the world's top countries in tomato production, and they have huge domestic and export demand. Africa is the second-largest region, accounting for 28.7% area of the world's tomato acreage in 2022. In Africa, the cultivated area increased by 14.5% between 2017 and 2022. Nigeria accounted for 54.8% of the total tomato acreage in the region in 2022 due to higher demand in the country.

- In 2022, Europe held 10.6% of the global tomato acreage. Turkey is the largest country, with 28.2% of the total European tomato acreage in the same year. Turkey is one of the largest producers of tomatoes in the world. Moreover, North America accounted for 4.1% of the world's tomato acreage in 2022. The United States is the major country, which held about 49.4% of the region's tomato area in the same year. South America accounted for 2.2% of the world's tomato acreage in 2022. Brazil alone held more than 42% of the total tomato acreage in the region during the same year. The increase in demand for tomatoes from various industries is anticipated to drive tomato acreage globally during the forecast period.

The expanding tomato seed market is driven by the increasing demand for disease-resistant and widely adaptable seed varieties

- Tomato is one of the largest segments of vegetables because of the high-value crop and high demand by processing industries for tomato puree, ketchup, and others. Major companies, such as Syngenta, Rijk Zwaan, and Enza Zaden, have more than 40% tomato seed varieties available globally that are resistant to viral diseases such as the leaf curl virus.

- Traits with resistance to viral diseases such as tomato mosaic virus, tomato yellow leaf curl virus, blossom end rot, powdery mildew, wilt diseases, and nematodes are popularly used for cultivation. Asia-Pacific is one of the largest tomato-producing regions, and major companies such as Rijk Zwaan, East-West Seed, and Namdhari Seeds have tomato seed varieties in the region that are resistant to viral diseases such as leaf curl virus. For instance, in 2022, Rijk Zwaan launched new tomato seed varieties resistant to the Tomato Brown Rugose Fruit Virus (ToBRFV). Moreover, in 2022, HM. Clause, a business unit of Limagrain, introduced a tomato variety that is resistant to the highly transmissible ToBRFV.

- Tomato varieties with extended shelf life, uniformity, cracking tolerance, and wider adaptability to different soils and climatic conditions are in high demand. Companies such as Bayer, Syngenta, and Rijk Zwaan offer seed varieties such as Kierano, Aurea, Angelle, Tontolle, and Cheramy RZ F1 to produce high-quality tomatoes in different agro conditions.

- The introduction of new hybrid seed varieties by companies with higher resistance to viruses, adaptability to different weather conditions, and high demand by processing industries are the factors expected to help in the growth of the tomato seed market during the forecast period.

Tomato Seed Industry Overview

The Tomato Seed Market is moderately consolidated, with the top five companies occupying 57.41%. The major players in this market are BASF SE, Bayer AG, Groupe Limagrain, Rijk Zwaan Zaadteelt en Zaadhandel BV and Syngenta Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Cultivation

- 4.2 Most Popular Traits

- 4.3 Breeding Techniques

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Breeding Technology

- 5.1.1 Hybrids

- 5.1.2 Open Pollinated Varieties & Hybrid Derivatives

- 5.2 Cultivation Mechanism

- 5.2.1 Open Field

- 5.2.2 Protected Cultivation

- 5.3 Region

- 5.3.1 Africa

- 5.3.1.1 By Breeding Technology

- 5.3.1.2 By Cultivation Mechanism

- 5.3.1.3 By Country

- 5.3.1.3.1 Egypt

- 5.3.1.3.2 Ethiopia

- 5.3.1.3.3 Ghana

- 5.3.1.3.4 Kenya

- 5.3.1.3.5 Nigeria

- 5.3.1.3.6 South Africa

- 5.3.1.3.7 Tanzania

- 5.3.1.3.8 Rest of Africa

- 5.3.2 Asia-Pacific

- 5.3.2.1 By Breeding Technology

- 5.3.2.2 By Cultivation Mechanism

- 5.3.2.3 By Country

- 5.3.2.3.1 Australia

- 5.3.2.3.2 Bangladesh

- 5.3.2.3.3 China

- 5.3.2.3.4 India

- 5.3.2.3.5 Indonesia

- 5.3.2.3.6 Japan

- 5.3.2.3.7 Myanmar

- 5.3.2.3.8 Pakistan

- 5.3.2.3.9 Philippines

- 5.3.2.3.10 Thailand

- 5.3.2.3.11 Vietnam

- 5.3.2.3.12 Rest of Asia-Pacific

- 5.3.3 Europe

- 5.3.3.1 By Breeding Technology

- 5.3.3.2 By Cultivation Mechanism

- 5.3.3.3 By Country

- 5.3.3.3.1 France

- 5.3.3.3.2 Germany

- 5.3.3.3.3 Italy

- 5.3.3.3.4 Netherlands

- 5.3.3.3.5 Poland

- 5.3.3.3.6 Romania

- 5.3.3.3.7 Russia

- 5.3.3.3.8 Spain

- 5.3.3.3.9 Turkey

- 5.3.3.3.10 Ukraine

- 5.3.3.3.11 United Kingdom

- 5.3.3.3.12 Rest of Europe

- 5.3.4 Middle East

- 5.3.4.1 By Breeding Technology

- 5.3.4.2 By Cultivation Mechanism

- 5.3.4.3 By Country

- 5.3.4.3.1 Iran

- 5.3.4.3.2 Saudi Arabia

- 5.3.4.3.3 Rest of Middle East

- 5.3.5 North America

- 5.3.5.1 By Breeding Technology

- 5.3.5.2 By Cultivation Mechanism

- 5.3.5.3 By Country

- 5.3.5.3.1 Canada

- 5.3.5.3.2 Mexico

- 5.3.5.3.3 United States

- 5.3.5.3.4 Rest of North America

- 5.3.6 South America

- 5.3.6.1 By Breeding Technology

- 5.3.6.2 By Cultivation Mechanism

- 5.3.6.3 By Country

- 5.3.6.3.1 Argentina

- 5.3.6.3.2 Brazil

- 5.3.6.3.3 Rest of South America

- 5.3.1 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Advanta Seeds - UPL

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Bejo Zaden BV

- 6.4.5 East-West Seed

- 6.4.6 Groupe Limagrain

- 6.4.7 Rijk Zwaan Zaadteelt en Zaadhandel BV

- 6.4.8 Sakata Seeds Corporation

- 6.4.9 Syngenta Group

- 6.4.10 Yuan Longping High-Tech Agriculture Co. Ltd

7 KEY STRATEGIC QUESTIONS FOR SEEDS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Global Market Size and DROs

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms