|

市場調査レポート

商品コード

1686176

軍用航空宇宙シミュレーションおよびトレーニング:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Military Aerospace Simulation And Training - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 軍用航空宇宙シミュレーションおよびトレーニング:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

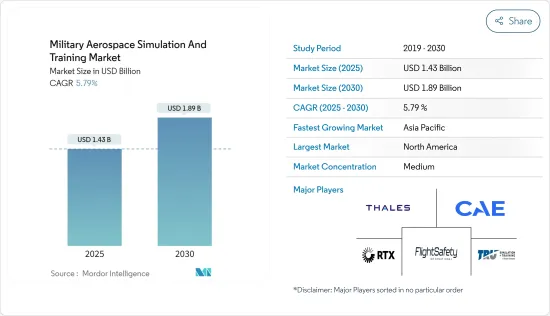

軍用航空宇宙シミュレーションおよびトレーニングの市場規模は2025年に14億3,000万米ドルと推定され、2030年には18億9,000万米ドルに達すると予測され、予測期間(2025-2030年)のCAGRは5.79%です。

世界各国は軍用機の保有を拡大しており、熟練パイロットの需要を促進しています。この訓練されたパイロットに対するニーズの急増が、軍用機シミュレーション・訓練市場の成長を促進する重要な要因となっています。

世界の軍隊は兵器システムへの防衛支出を強化しており、市場の拡大に直接影響を与えています。このような軍事費の増加は、情報・監視から戦闘作戦まで、さまざまな製品を網羅するこれらの国の調達戦略に沿ったものです。

さらに、最先端航空機の導入や、こうした高性能機のパイロットの訓練に関連する費用の高騰も、市場を後押ししています。さらに、厳しい政府規制とそれに伴う高いコンプライアンス・コストは、新規市場参入者にとって大きな参入障壁となっています。これは中小企業や新興企業にとっては特に困難な課題であり、競争を制約し、イノベーションを阻害する可能性があります。

軍用航空宇宙シミュレーションおよびトレーニング市場の動向

予測期間中に最も高い成長が見込まれる固定翼セグメント

固定翼セグメントは現在市場を独占しており、予測期間中に最も高いCAGRを示すと予測されています。この成長の主な要因は、世界の軍隊が新しい航空機モデルの開発と調達に取り組んでいることです。各国政府は、その能力を強化するために、シミュレーターや訓練プロバイダーとの連携を強めています。

近年、世界の防衛費の急増が目立っているが、これはさまざまな要因が重なっているためです。これには、紛争の激化、内外の安全保障上の脅威、世界のテロの増加、特定の国による支配への野心、国境安全保障上の懸念の高まり、緊張した国際関係、防衛における急速な技術進歩などが含まれます。

AIの技術的進歩は、将来の訓練プログラムにおいて極めて重要な役割を果たすことになると思われます。さらに、OEMによる継続的な航空機開発イニシアティブが、固定翼機セグメントの成長を後押ししています。世界的に軍事的緊張が高まる中、より能力の高い戦闘機への需要が高まっています。同様に重要なのは、特に敵対的な地形やシナリオにおいて、これらの航空機を巧みに操縦するパイロットの必要性です。

その結果、固定翼シミュレーターの需要はここ最近、かつてないレベルに達しています。このため、多くの技術メーカーやイノベーターが独自の製品を発表しています。例えば、2024年3月、インド国防省は、Su-30 MKI戦闘機シミュレーターを強化するため、地元企業と契約を結びました。これらのシミュレーターは、パイロット訓練の水準を高める上で極めて重要です。

予測期間中に最も高い成長を遂げるアジア太平洋地域

アジア太平洋地域は、今後数年間、軍用機市場で最も大きな成長を遂げる構えです。アジア太平洋諸国における軍事費の急増が、主にこの成長を後押ししています。この地域における政治的緊張の高まりと領土紛争は、特に国境監視と保護のための航空機とUAVの需要を強化しました。さらに、これらの国々は訓練の効果を高めるために最先端の技術を積極的に取り入れています。このような技術革新の推進と先進的な航空機シミュレータに対するニーズの高まりが、この地域における軍用機訓練とシミュレーションの需要をさらに押し上げています。

特に中国との軍事的緊張が高まる中、アジアの多くの国々が攻撃力と防御力を強化しています。その結果、戦闘機の調達と開発イニシアチブが顕著に増加しています。このジェット機購入の急増は、パイロットを適切に訓練するためのシミュレーターの重要な必要性を強調しています。このことを認識し、多くの政府がシミュレーター技術への投資を強化しています。

2024年2月、シンガポール空軍(RSAF)はスペインの防衛企業インドラと契約を結びました。この契約は、エアバスH225M軍用ヘリコプターに合わせた先進的なミッション・シミュレーターの開発・販売に関わるものです。このシミュレーターは、欧州航空安全機関が定めたレベルDの認定基準を満たすように設計されており、多様で厳しい環境における昼夜の任務を包括的にエミュレートできます。同様の取り組みが台頭していることから、この市場セグメントは今後数年で大きく成長する見通しです。

軍用航空宇宙シミュレーションおよびトレーニング業界の概要

軍用航空宇宙シミュレーションおよびトレーニング市場の有力企業には、CAE Inc.、FlightSafety International Inc.、THALES、RTX Corporation、TRU Simulation+Training Inc.(Textron Inc.)などがあり、市場統合は中程度です。主要なトレーニングおよびシミュレーションメーカーは、ここ数年力強い収益成長を遂げています。

市場のリーダーの多くは、明確なブランド開拓と顧客獲得のためのリーチ拡大に注力しています。そのためには、新製品を発売したり、既存の製品を強化したりして、製品ラインを充実させる必要があります。

同時に、世界の大手航空会社と戦略的パートナーシップを結び、市場での存在感を高めている企業もあります。コスト削減と軍用パイロットの即応性向上のためのシミュレーターへの継続的なニーズにより、この成長は拡大すると予想されます。さらに、新しいシミュレーションや訓練装置の開発は、市場での存在感を高めるのに役立つと期待されています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- シミュレータータイプ別

- フルフライトシミュレータ(FFS)

- フライト訓練装置(FTD)

- その他のシミュレータタイプ

- 航空機タイプ別

- 回転翼機

- 固定翼機

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- フランス

- ドイツ

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 世界のその他の地域

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- L3Harris Technologies, Inc.

- RTX Corporation

- BAE Systems plc

- The Boeing Company

- CACI International Inc.

- CAE Inc.

- Merlin Simulation Inc.

- Lockheed Martin Corporation

- THALES

- TRU Simulation+Training Inc.

- Rheinmetall AG

- Northrop Grumman Corporation

- Flight Safety International Inc.

第7章 市場機会と今後の動向

The Military Aerospace Simulation And Training Market size is estimated at USD 1.43 billion in 2025, and is expected to reach USD 1.89 billion by 2030, at a CAGR of 5.79% during the forecast period (2025-2030).

Countries worldwide are expanding their military aircraft fleets, driving the demand for skilled pilots. This surge in the need for trained pilots is a key factor fueling the growth of the military aircraft simulation and training market.

Global armed forces are bolstering their defense spending on weapon systems, directly influencing market expansion. This heightened military expenditure is in line with these nations' procurement strategies, encompassing a spectrum of products, from intelligence and surveillance to combat operations.

Furthermore, the market is buoyed by the introduction of cutting-edge aircraft and the escalating costs associated with training pilots for these sophisticated machines. Additionally, stringent government regulations, with their associated high costs of compliance, pose a significant entry barrier for new market entrants. This can be particularly challenging for smaller or emerging businesses, constraining competition and potentially stifling innovation.

Military Aircraft Simulation & Training Market Trends

Fixed-wing Segment Anticipated to Experience the Highest Growth During the Forecast Period

The fixed-wing segment currently dominates the market and is poised to exhibit the highest CAGR during the forecast period. This growth is primarily attributed to the global armed forces' initiatives in developing and procuring new aircraft models. Governments are increasingly collaborating with simulators and training providers to bolster their capabilities.

In recent years, there has been a notable surge in global defense expenditures, driven by a confluence of factors. These include escalating conflicts, both internal and external security threats, a rise in global terrorism, ambitions for dominance by certain nations, heightened border security concerns, strained international relations, and rapid technological advancements in defense.

AI's technological strides are set to play a pivotal role in future training programs. Furthermore, OEMs' ongoing aircraft development initiatives are bolstering the fixed-wing segment's growth. With heightened military tensions globally, there's a growing demand for higher-capacity combat aircraft. Equally crucial is the need for pilots to navigate these aircraft adeptly, especially in adversarial terrains and scenarios.

Consequently, the demand for fixed-wing simulators has reached unprecedented levels in recent times. This has prompted numerous technology manufacturers and innovators to introduce tailored products. For example, in March 2024, the Indian Defence Ministry inked a deal with a local firm to enhance its Su-30 MKI fighter aircraft simulator. These simulators are pivotal in elevating pilot training standards.

Asia-Pacific to Experience the Highest Growth During the Forecast Period

The Asia-Pacific region is poised for the most significant growth in the military aircraft market in the coming years. A surge in military spending across Asia-Pacific nations primarily fuels this growth. Heightened political tensions and territorial disputes in the region bolstered the demand for aircraft and UAVs, particularly for border surveillance and protection. Moreover, these nations are actively integrating cutting-edge technologies to enhance training effectiveness. This push for innovation and the rising need for advanced aircraft simulators further propel the demand for military aircraft training and simulation in the region.

Amid escalating military tensions, particularly with China, numerous Asian nations are bolstering their offensive and defensive capabilities. Consequently, there has been a notable uptick in fighter jet procurement and development initiatives. This surge in jet acquisitions has underscored the critical need for simulators to train pilots adequately. Recognizing this, many governments are ramping up their investments in simulator technologies.

Highlighting this trend, in February 2024, the Republic of Singapore Air Force (RSAF) inked a contract with Indra, a Spanish defense company. The deal entails developing and distributing an advanced mission simulator tailored for the Airbus H225M military helicopter. The simulator, designed to meet Level D accreditation standards set by the European Aviation Safety Agency, offers a comprehensive emulation of day and night missions in varied and challenging environments. With similar initiatives rising, this market segment is poised for substantial growth in the coming years.

Military Aircraft Simulation & Training Industry Overview

Some of the few prominent players in the military aircraft simulation and training market are CAE Inc., FlightSafety International Inc., THALES, RTX Corporation, and TRU Simulation + Training Inc. (Textron Inc.), with medium-level market consolidation. The leading training and simulation manufacturers have experienced strong revenue growth in the past few years.

Many market leaders focus on developing distinct brands and expanding their reach to attract customers. They achieve this by enhancing their product lines, either through new launches or by enhancing existing offerings.

Concurrently, some firms are forming strategic partnerships with leading airlines worldwide to bolster their market presence. This growth is expected to increase with a continuous need for simulators to reduce costs and improve the readiness of military pilots. In addition, developing new simulation and training devices is expected to help them increase their market presence.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Simulator Type

- 5.1.1 Full Flight Simulator (FFS)

- 5.1.2 Flight Training Devices (FTD)

- 5.1.3 Other Simulator Types

- 5.2 By Aircraft Type

- 5.2.1 Rotorcraft

- 5.2.2 Fixed-Wing

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 France

- 5.3.2.3 Germany

- 5.3.2.4 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Rest of the World

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 L3Harris Technologies, Inc.

- 6.2.2 RTX Corporation

- 6.2.3 BAE Systems plc

- 6.2.4 The Boeing Company

- 6.2.5 CACI International Inc.

- 6.2.6 CAE Inc.

- 6.2.7 Merlin Simulation Inc.

- 6.2.8 Lockheed Martin Corporation

- 6.2.9 THALES

- 6.2.10 TRU Simulation + Training Inc.

- 6.2.11 Rheinmetall AG

- 6.2.12 Northrop Grumman Corporation

- 6.2.13 Flight Safety International Inc.