戦闘機シミュレーションの世界市場:2025年~2035年

Global Fighter Aircraft Simulation Market 2025-2035- 発行日

- ページ情報

- 英文 150+ Pages

- 納期

- 3営業日

- 商品コード

- 1727194

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

- 航空宇宙/防衛関連専門 航空宇宙/防衛関連専門を専門とする市場調査会社です。

概要

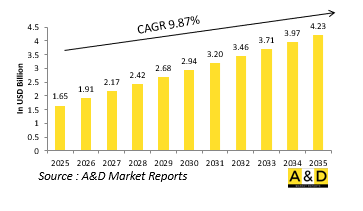

世界の戦闘機シミュレーションの市場規模は、2025年に16億5,000万米ドルと推定され、2035年までに42億3,000万米ドルに成長すると予測されており、予測期間の2025年~2035年の年間平均成長率(CAGR)は9.87%と見込まれています。

戦闘機シミュレーション市場のイントロダクション:

戦闘機シミュレーションは、現代空軍の訓練と作戦準備に不可欠な要素となっています。これらのシステムは、実世界の飛行環境、戦闘シナリオ、複雑な任務を再現するもので、パイロットは実際の飛行のリスクやコストを負うことなく技能を開発し、磨くことができます。シミュレーションは、基本的な飛行指導から高度な戦闘行動、電子戦、統合部隊の調整まで、幅広い訓練ニーズに対応しています。これらのツールにより、航空機乗務員はコントロールされた環境でリスクの高いミッションを繰り返し練習することができ、装備を保全し安全を確保しながらパフォーマンスを向上させることができます。さらにシミュレーターは、チームがさまざまな脅威の状況下でさまざまなシナリオをリハーサルできるようにすることで、意思決定や戦術立案に貢献しています。シミュレーターの高性能化により、特定の敵の戦術、空域構成、環境課題を模倣できるようになっています。このリアリズムは、パイロットの能力を高めるだけでなく、あらゆる指揮官レベルにわたって戦略的思考とミッションのリハーサルを支援します。戦闘機シミュレーションは、理論的知識と実戦経験とのギャップを埋める、戦力準備の重要な要素です。現代の航空戦闘が技術的に高度化し、予測不可能なものとなる中、シミュレーションは、熟練した適応力を持ち、任務に即応できる搭乗員を育成するための重要なリソースであり続けています。

戦闘機シミュレーション市場における技術の影響:

技術の進歩は戦闘機シミュレーションの能力を劇的に拡大し、忠実度の高い訓練および作戦計画ツールへと変貌させました。強化されたビジュアルシステムは、風景、天候、空中の脅威を正確に表現し、超リアルな3D環境を提供します。モーション・プラットフォームは飛行の身体感覚を再現し、高解像度のコックピット・ディスプレイと触覚コントロールは現実の状況に近い没入感を提供します。人工知能は、リアルな敵の行動を生成することでシミュレーションをさらに向上させ、訓練生にダイナミックで反応性の高いシナリオを課しています。デジタルツインモデルとの統合により、特定の航空機システムを再現し、技術訓練や性能分析を行うことができます。さらに、ネットワーク化されたシミュレーションにより、複数のパイロットや部隊が同期した大規模な戦闘シナリオで一緒に訓練できるようになり、合同演習や連合演習を支援できるようになりました。また、拡張現実や仮想現実の応用も台頭してきており、高い双方向性を維持しつつ、費用対効果の高い可搬型の訓練オプションが可能になっています。これらのシステムの接続が進むにつれて、ライブ・フライト・データやミッション報告ツールとの統合が進み、継続的なフィードバックと改善がサポートされるようになっています。このようなデジタル技術の融合により、シミュレーションは補助的なツールから、現代の空軍にとって中核的な能力へと変貌を遂げています。シミュレーションは、ミッションのリハーサルを強化し、航空機の摩耗を軽減し、複雑で変化の激しい戦闘環境における適応性を促進します。

戦闘機シミュレーション市場の主な促進要因:

さまざまな作戦上、戦略上、経済上の要因によって、世界の防衛軍全体で戦闘機シミュレーションが重視されるようになっています。最も影響力のある要因の1つは、費用対効果の高い訓練ソリューションの必要性です。実飛行訓練には、燃料、整備、空域調整など、多大な資源が費やされるのに対し、シミュレータは同じような後方支援の負担なしに、繰り返し、拡張可能な訓練を行うことができます。シミュレーションは、人員や航空機を実際の危険にさらすことなく、緊急手順や戦闘行為、複雑な操縦を練習するための安全な空間を提供します。現代の航空戦闘では、電子戦スイート、目視範囲を超えるミサイル、統合センサーなど、高度なシステムの導入が進んでいるため、シミュレーションは、パイロットがこれらの技術を統合的に使用する訓練を行うための重要なプラットフォームとなります。また、他部門や同盟軍との合同演習を可能にすることで、マルチドメイン作戦の準備も支援します。さらに、世界の脅威は予測不可能であるため、定期的な訓練の更新とシナリオの柔軟性が必要となるが、シミュレーションは現実の演習よりもはるかに迅速に対応できます。最後に、シミュレーションは新人パイロットの搭乗とスキルアップにおいて重要な役割を果たし、座学と実飛行のギャップを埋める。こうした複合的な圧力により、シミュレーションは現代空軍の作戦準備態勢と技術的能力を維持するための戦略的優先事項へと高められています。

戦闘機シミュレーション市場の地域動向:

戦闘機シミュレーションシステムの地域的な導入と進化は、各地域の防衛戦略、訓練理念、技術インフラを反映しています。北米、特に米国では、シミュレーションはパイロット育成と任務リハーサルプログラムに深く組み込まれており、現実とシミュレーションの要素をシームレスに移行できるライブ・バーチャル・コンストラクティブ(LVC)訓練フレームワークの統合に重点が置かれています。欧州諸国は、特にNATO加盟国間の連合ベースの作戦を支援するため、モジュール式で相互運用可能なシステムを優先し、共有訓練環境と標準化されたミッション・プロトコルを育成しています。アジア太平洋では、航空戦力の野心と地域の緊張の高まりから、インド、日本、オーストラリアなどの国々が、現地の空域と脅威シナリオを再現する高度なシミュレータに多額の投資を行っています。これらのシステムは、国産航空機の開発など、より広範な防衛近代化目標と連携していることが多いです。中東では、実戦訓練のための空域が限られた厳しい環境にもかかわらず、戦闘態勢の構築と維持にシミュレーションが重要な役割を果たしています。ラテンアメリカとアフリカでの導入はより選択的であり、特定の近代化プログラムや外国の防衛サプライヤーとのパートナーシップに関連することが多いです。どの地域でも、訓練だけでなく、作戦計画やシステムテスト、進化する戦闘教義への将来能力の統合にもシミュレーションを活用する方向へのシフトが進んでいます。

主要戦闘機シミュレーションプログラム:

日本は、世界・コンバット・エア・プログラム(GCAP)の下で英国、イタリアと共同開発中の次世代戦闘機のオーストラリアへの輸出を検討していると報じられています。先月、東京はインドにもGCAP構想への参加を呼びかけました。2024年3月、日本の内閣は防衛装備品輸出に関する厳しい規制を緩和し、将来的な次世代戦闘機輸出の道筋を作っています。この規制緩和は、そのような輸出を、日本と既存の防衛装備品および技術移転協定を結んでいる国に限定するという条件に基づいています。さらに、輸出の可能性は個別に評価され、連立与党内の協議に従って決定されます。

当レポートでは、世界の戦闘機シミュレーション市場について調査し、10年間のセグメント別市場予測、技術動向、機会分析、企業プロファイル、国別データなどをまとめています。

目次

戦闘機シミュレーション市場 - 目次

戦闘機シミュレーション市場レポートの定義

戦闘機シミュレーション市場セグメンテーション

地域別

技術別

用途別

タイプ別

今後10年間の戦闘機シミュレーション市場分析

この章では、10年間の戦闘機シミュレーション市場分析によって、戦闘機シミュレーション市場の成長、変化する動向、技術採用の概要、および全体的な市場の魅力に関する詳細な概要が説明されます。

戦闘機シミュレーション市場の市場技術

このセグメントでは、この市場に影響を与えると予想される上位10の技術と、これらの技術が市場全体に与える可能性のある影響について説明します。

世界の戦闘機シミュレーション市場予測

この市場の10年間の戦闘機シミュレーション市場予測は、上記のセグメント全体で詳細にカバーされています。

地域別戦闘機シミュレーション市場の動向と予測

このセグメントでは、地域別の戦闘機シミュレーション市場の動向、促進要因、抑制要因、課題、そして政治、経済、社会、技術といった側面を網羅しています。また、地域別の市場予測とシナリオ分析も詳細に取り上げています。地域分析の最後には、主要企業のプロファイリング、サプライヤーの情勢、企業ベンチマークが含まれています。現在の市場規模は、通常のシナリオに基づいて推定されています。

北米

促進要因、抑制要因、課題

PEST

市場予測とシナリオ分析

主要企業

サプライヤー階層の情勢

企業ベンチマーク

欧州

中東

アジア太平洋

南米

アクセス制御市場の国別分析

この章では、この市場における主要な防衛プログラムを取り上げ、この市場で申請された最新のニュースや特許についても解説します。また、国レベルの10年間の市場予測とシナリオ分析についても解説します。

米国

防衛プログラム

最新ニュース

特許

この市場における現在の技術成熟度

市場予測とシナリオ分析

カナダ

イタリア

フランス

ドイツ

オランダ

ベルギー

スペイン

スウェーデン

ギリシャ

オーストラリア

南アフリカ

インド

中国

ロシア

韓国

日本

マレーシア

シンガポール

ブラジル

戦闘機シミュレーション市場の機会マトリックス

戦闘機シミュレーション市場レポートに関する専門家の意見

結論

航空・防衛市場レポートについて

図表

List of Tables

- Table 1: 10 Year Market Outlook, 2025-2035

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2025-2035

- Table 18: Scenario Analysis, Scenario 1, By Type, 2025-2035

- Table 19: Scenario Analysis, Scenario 1, By Technology, 2025-2035

- Table 20: Scenario Analysis, Scenario 1, By Application, 2025-2035

- Table 21: Scenario Analysis, Scenario 2, By Region, 2025-2035

- Table 22: Scenario Analysis, Scenario 2, By Type, 2025-2035

- Table 23: Scenario Analysis, Scenario 2, By Technology, 2025-2035

- Table 24: Scenario Analysis, Scenario 2, By Application, 2025-2035

List of Figures

- Figure 1: Global Fighter Aircraft Simulation Market Forecast, 2025-2035

- Figure 2: Global Fighter Aircraft Simulation Market Forecast, By Region, 2025-2035

- Figure 3: Global Fighter Aircraft Simulation Market Forecast, By Type, 2025-2035

- Figure 4: Global Fighter Aircraft Simulation Market Forecast, By Technology, 2025-2035

- Figure 5: Global Fighter Aircraft Simulation Market Forecast, By Application, 2025-2035

- Figure 6: North America, Fighter Aircraft Simulation Market, Market Forecast, 2025-2035

- Figure 7: Europe, Fighter Aircraft Simulation Market, Market Forecast, 2025-2035

- Figure 8: Middle East, Fighter Aircraft Simulation Market, Market Forecast, 2025-2035

- Figure 9: APAC, Fighter Aircraft Simulation Market, Market Forecast, 2025-2035

- Figure 10: South America, Fighter Aircraft Simulation Market, Market Forecast, 2025-2035

- Figure 11: United States, Fighter Aircraft Simulation Market, Technology Maturation, 2025-2035

- Figure 12: United States, Fighter Aircraft Simulation Market, Market Forecast, 2025-2035

- Figure 13: Canada, Fighter Aircraft Simulation Market, Technology Maturation, 2025-2035

- Figure 14: Canada, Fighter Aircraft Simulation Market, Market Forecast, 2025-2035

- Figure 15: Italy, Fighter Aircraft Simulation Market, Technology Maturation, 2025-2035

- Figure 16: Italy, Fighter Aircraft Simulation Market, Market Forecast, 2025-2035

- Figure 17: France, Fighter Aircraft Simulation Market, Technology Maturation, 2025-2035

- Figure 18: France, Fighter Aircraft Simulation Market, Market Forecast, 2025-2035

- Figure 19: Germany, Fighter Aircraft Simulation Market, Technology Maturation, 2025-2035

- Figure 20: Germany, Fighter Aircraft Simulation Market, Market Forecast, 2025-2035

- Figure 21: Netherlands, Fighter Aircraft Simulation Market, Technology Maturation, 2025-2035

- Figure 22: Netherlands, Fighter Aircraft Simulation Market, Market Forecast, 2025-2035

- Figure 23: Belgium, Fighter Aircraft Simulation Market, Technology Maturation, 2025-2035

- Figure 24: Belgium, Fighter Aircraft Simulation Market, Market Forecast, 2025-2035

- Figure 25: Spain, Fighter Aircraft Simulation Market, Technology Maturation, 2025-2035

- Figure 26: Spain, Fighter Aircraft Simulation Market, Market Forecast, 2025-2035

- Figure 27: Sweden, Fighter Aircraft Simulation Market, Technology Maturation, 2025-2035

- Figure 28: Sweden, Fighter Aircraft Simulation Market, Market Forecast, 2025-2035

- Figure 29: Brazil, Fighter Aircraft Simulation Market, Technology Maturation, 2025-2035

- Figure 30: Brazil, Fighter Aircraft Simulation Market, Market Forecast, 2025-2035

- Figure 31: Australia, Fighter Aircraft Simulation Market, Technology Maturation, 2025-2035

- Figure 32: Australia, Fighter Aircraft Simulation Market, Market Forecast, 2025-2035

- Figure 33: India, Fighter Aircraft Simulation Market, Technology Maturation, 2025-2035

- Figure 34: India, Fighter Aircraft Simulation Market, Market Forecast, 2025-2035

- Figure 35: China, Fighter Aircraft Simulation Market, Technology Maturation, 2025-2035

- Figure 36: China, Fighter Aircraft Simulation Market, Market Forecast, 2025-2035

- Figure 37: Saudi Arabia, Fighter Aircraft Simulation Market, Technology Maturation, 2025-2035

- Figure 38: Saudi Arabia, Fighter Aircraft Simulation Market, Market Forecast, 2025-2035

- Figure 39: South Korea, Fighter Aircraft Simulation Market, Technology Maturation, 2025-2035

- Figure 40: South Korea, Fighter Aircraft Simulation Market, Market Forecast, 2025-2035

- Figure 41: Japan, Fighter Aircraft Simulation Market, Technology Maturation, 2025-2035

- Figure 42: Japan, Fighter Aircraft Simulation Market, Market Forecast, 2025-2035

- Figure 43: Malaysia, Fighter Aircraft Simulation Market, Technology Maturation, 2025-2035

- Figure 44: Malaysia, Fighter Aircraft Simulation Market, Market Forecast, 2025-2035

- Figure 45: Singapore, Fighter Aircraft Simulation Market, Technology Maturation, 2025-2035

- Figure 46: Singapore, Fighter Aircraft Simulation Market, Market Forecast, 2025-2035

- Figure 47: United Kingdom, Fighter Aircraft Simulation Market, Technology Maturation, 2025-2035

- Figure 48: United Kingdom, Fighter Aircraft Simulation Market, Market Forecast, 2025-2035

- Figure 49: Opportunity Analysis, Fighter Aircraft Simulation Market, By Region (Cumulative Market), 2025-2035

- Figure 50: Opportunity Analysis, Fighter Aircraft Simulation Market, By Region (CAGR), 2025-2035

- Figure 51: Opportunity Analysis, Fighter Aircraft Simulation Market, By Type (Cumulative Market), 2025-2035

- Figure 52: Opportunity Analysis, Fighter Aircraft Simulation Market, By Type (CAGR), 2025-2035

- Figure 53: Opportunity Analysis, Fighter Aircraft Simulation Market, By Technology (Cumulative Market), 2025-2035

- Figure 54: Opportunity Analysis, Fighter Aircraft Simulation Market, By Technology (CAGR), 2025-2035

- Figure 55: Opportunity Analysis, Fighter Aircraft Simulation Market, By Application (Cumulative Market), 2025-2035

- Figure 56: Opportunity Analysis, Fighter Aircraft Simulation Market, By Application (CAGR), 2025-2035

- Figure 57: Scenario Analysis, Fighter Aircraft Simulation Market, Cumulative Market, 2025-2035

- Figure 58: Scenario Analysis, Fighter Aircraft Simulation Market, Global Market, 2025-2035

- Figure 59: Scenario 1, Fighter Aircraft Simulation Market, Total Market, 2025-2035

- Figure 60: Scenario 1, Fighter Aircraft Simulation Market, By Region, 2025-2035

- Figure 61: Scenario 1, Fighter Aircraft Simulation Market, By Type, 2025-2035

- Figure 62: Scenario 1, Fighter Aircraft Simulation Market, By Technology, 2025-2035

- Figure 63: Scenario 1, Fighter Aircraft Simulation Market, By Application, 2025-2035

- Figure 64: Scenario 2, Fighter Aircraft Simulation Market, Total Market, 2025-2035

- Figure 65: Scenario 2, Fighter Aircraft Simulation Market, By Region, 2025-2035

- Figure 66: Scenario 2, Fighter Aircraft Simulation Market, By Type, 2025-2035

- Figure 67: Scenario 2, Fighter Aircraft Simulation Market, By Technology, 2025-2035

- Figure 68: Scenario 2, Fighter Aircraft Simulation Market, By Application, 2025-2035

- Figure 69: Company Benchmark, Fighter Aircraft Simulation Market, 2025-2035

目次

The Global Fighter Aircraft Simulation market is estimated at USD 1.65 billion in 2025, projected to grow to USD 4.23 billion by 2035 at a Compound Annual Growth Rate (CAGR) of 9.87% over the forecast period 2025-2035.

Introduction to Fighter Aircraft Simulation Market:

Fighter aircraft simulation has become an essential element in the training and operational readiness of modern air forces. These systems replicate real-world flying environments, combat scenarios, and mission complexities, allowing pilots to develop and refine skills without the risks and costs of actual flight. Simulation supports a wide spectrum of training needs-from basic flight instruction to advanced combat maneuvers, electronic warfare, and joint-force coordination. These tools enable aircrews to repeatedly practice high-risk missions in a controlled setting, improving performance while preserving equipment and ensuring safety. Additionally, simulators contribute to decision-making and tactical planning by allowing teams to rehearse various scenarios under different threat conditions. With increasing sophistication, they can now mimic specific enemy tactics, airspace configurations, and environmental challenges. This realism not only enhances pilot competence but also supports strategic thinking and mission rehearsal across all levels of command. Fighter aircraft simulation is a critical component of force preparedness, bridging the gap between theoretical knowledge and live operational experience. As modern air combat grows more technologically advanced and unpredictable, simulation continues to be a key resource for cultivating skilled, adaptive, and mission-ready aircrews worldwide.

Technology Impact in Fighter Aircraft Simulation Market:

Technological advancement has dramatically expanded the capabilities of fighter aircraft simulation, turning it into a high-fidelity training and operational planning tool. Enhanced visual systems now provide ultra-realistic 3D environments, accurately representing landscapes, weather, and aerial threats. Motion platforms replicate the physical sensations of flight, while high-resolution cockpit displays and tactile controls provide immersion that closely mirrors real-world conditions. Artificial intelligence has further improved simulations by generating realistic adversary behaviors, challenging trainees with dynamic, responsive scenarios. Integration with digital twin models enables the replication of specific aircraft systems for technical training and performance analysis. Furthermore, networked simulations now allow multiple pilots and units to train together in synchronized, large-scale combat scenarios, supporting joint and coalition exercises. Augmented and virtual reality applications are also gaining ground, enabling cost-effective, portable training options that retain high interactivity. As these systems become more connected, they are increasingly integrated with live flight data and mission debriefing tools, supporting continuous feedback and improvement. This convergence of digital technologies has transformed simulation from a supplemental tool into a core capability for modern air forces. It enhances mission rehearsal, reduces wear on aircraft, and fosters adaptability in complex, fast-changing combat environments.

Key Drivers in Fighter Aircraft Simulation Market:

A range of operational, strategic, and economic factors is driving the growing emphasis on fighter aircraft simulation across global defense forces. One of the most influential drivers is the need for cost-effective training solutions. Live flight training involves significant resource expenditure, including fuel, maintenance, and airspace coordination, whereas simulators offer repeated, scalable training without the same logistical burden. Safety is another compelling factor; simulation provides a secure space to practice emergency procedures, combat engagements, and complex maneuvers without exposing personnel or aircraft to actual risk. As modern air combat increasingly incorporates advanced systems-such as electronic warfare suites, beyond-visual-range missiles, and integrated sensors-simulation offers a vital platform for pilots to train in using these technologies cohesively. It also supports preparation for multi-domain operations by enabling joint exercises with other branches or allied forces. Additionally, the unpredictability of global threats necessitates regular training updates and scenario flexibility, something simulation can accommodate much faster than real-world exercises. Lastly, simulation plays a crucial role in onboarding and upskilling new pilots, bridging the gap between classroom learning and live flight. These combined pressures have elevated simulation to a strategic priority in sustaining operational readiness and technological competence in modern air forces.

Regional Trends in Fighter Aircraft Simulation Market:

Regional adoption and evolution of fighter aircraft simulation systems reflect each area's defense strategies, training philosophies, and technological infrastructure. In North America, particularly within the United States, simulation is deeply embedded in pilot development and mission rehearsal programs, with a focus on integrating live-virtual-constructive (LVC) training frameworks that allow seamless transition between real and simulated elements. European nations prioritize modular and interoperable systems to support coalition-based operations, especially among NATO members, fostering shared training environments and standardized mission protocols. In the Asia-Pacific region, growing airpower ambitions and regional tensions have led countries like India, Japan, and Australia to invest heavily in advanced simulators that replicate local airspace and threat scenarios. These systems are often aligned with broader defense modernization goals, including indigenous aircraft development. In the Middle East, simulation plays a key role in building and maintaining combat readiness despite challenging environments and limited airspace for live training. Adoption in Latin America and Africa is more selective, often tied to specific modernization programs or partnerships with foreign defense suppliers. Across all regions, there is a growing shift toward using simulation not just for training but also for operational planning, system testing, and integrating future capabilities into evolving combat doctrines.

Key Fighter Aircraft Simulation Program:

Japan is reportedly considering the export of its next-generation fighter aircraft-currently being co-developed with the UK and Italy under the Global Combat Air Programme (GCAP)-to Australia. Last month, Tokyo also extended an invitation to India to join the GCAP initiative. In March 2024, the Japanese cabinet eased the country's strict regulations on defense equipment exports, creating a pathway for the future export of next-gen fighter jets. The relaxation of these rules is based on the condition that such exports will be limited to nations that have existing defense equipment and technology transfer agreements with Japan. Additionally, each potential export will be assessed individually, with decisions made following internal consultations within the ruling coalition.

Table of Contents

Fighter Aircraft SIMULATION Market - Table of Contents

Fighter Aircraft SIMULATION market Report Definition

Fighter Aircraft SIMULATION market Segmentation

By Region

By Technology

By Application

By Type

Fighter Aircraft SIMULATION market Analysis for next 10 Years

The 10-year Fighter Aircraft SIMULATION market analysis would give a detailed overview of Fighter Aircraft SIMULATION market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Fighter Aircraft SIMULATION market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Fighter Aircraft SIMULATION market Forecast

The 10-year Fighter Aircraft SIMULATION market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Fighter Aircraft SIMULATION market Trends & Forecast

The regional Fighter Aircraft SIMULATION market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Access Control Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Fighter Aircraft SIMULATION market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Fighter Aircraft SIMULATION market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

- 発行日

- 発行

- Aviation & Defense Market Reports (A&D)

- ページ情報

- 英文 150+ Pages

- 納期

- 3営業日