クリーンラベル原料:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)

Clean Label Ingredient - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)- 発行日

- ページ情報

- 英文 135 Pages

- 納期

- 2~3営業日

- 商品コード

- 1939066

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

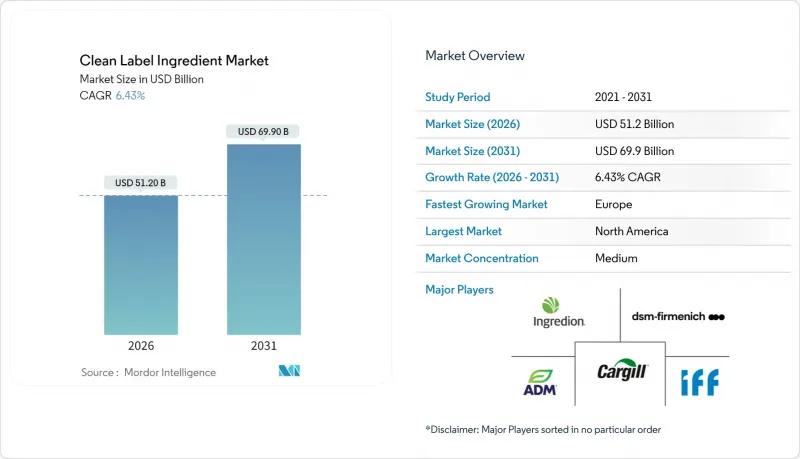

クリーンラベル原料市場は、2025年に481億1,000万米ドルと評価され、2026年の512億米ドルから2031年までに699億米ドルに達すると予測されています。

予測期間(2026年~2031年)におけるCAGRは6.43%と見込まれています。

この成長は、シンプルで認識しやすい原材料に対する消費者需要の高まり、パンデミック後の健康意識の向上、小売業者の原材料リスト簡素化の取り組みによって牽引されています。米国食品医薬品局(FDA)による石油系染料の段階的廃止などの規制イニシアチブは、天然着色料、香料、保存料の採用をさらに促進しています。これに対応し、メーカー各社は透明性の確保とクリーンラベル表示の検証を目的として、植物抽出技術、発酵プロセス、トレーサビリティ技術に焦点を当てた研究開発に投資しています。天然原料は現在、合成原料よりも高コスト(天然着色料は合成品より25~35%高価)ですが、生産規模の拡大と供給契約の強化に伴い価格差は縮小傾向にあります。さらに、小売業のプライベートブランドプログラムや電子商取引プラットフォームの拡大が採用を促進しており、クリーンラベル原料がニッチ市場から様々な地域における主流の動向へと移行していることを示しています。

世界の・クリーンラベル原料市場の動向と洞察

人工食品添加物に関連する健康問題

科学的な証拠により、人工食品添加物が健康への悪影響と関連付けられるケースが増加しており、消費者はよりクリーンな表示の代替品を求め始めています。米国国立医学図書館による2024年の画期的な研究では、合成食品着色料と呼吸器疾患(特に小児の肺機能障害)との強い関連性が確認されました。食と健康の関連性に対する認識の高まりを受け、消費者は加工食品に一般的に含まれる人工添加物や保存料を積極的に避けています。この消費者意識の変化は、国際食品情報評議会(IFIC)の2024年調査でも裏付けられています。同調査では、米国回答者の26%が「ナチュラル」を健康食品の主要指標と評価し、16%が「非遺伝子組み換え」表示を優先しました。こうした傾向は、天然素材と最小限の加工を重視するクリーンラベル原則との明確な一致を示しています。この消費者動向と科学的根拠の高まりを受け、規制当局も対応を強化しています。2025年4月、米国食品医薬品局(FDA)は食品供給網から石油由来の合成着色料を段階的に廃止する主要な取り組みを開始しました。これは規制面での重要な転換点であり、公衆衛生に対する政府の取り組みを強調するものです。こうした規制面、科学的、消費者主導の動向が相まって、食品安全基準の再構築、業界の透明性向上、そして現代の食品生産におけるクリーンラベル運動の重要性の確立が進んでいます。

植物由来・有機原料への移行

クリーンラベル運動は勢いを増し、植物由来革命と融合することで、世界の食品産業におけるイノベーション戦略を再構築しています。この連携は、食事と健康の関連性への認識の高まり、環境問題への懸念、倫理的な消費への移行によって推進されています。消費者は現在、原料調達における透明性を求め、合成添加物よりも自然由来で最小限の加工を施した植物由来の代替品を好む傾向にあります。この傾向は特に香料・増強剤分野で顕著です。メーカーは人工化合物から天然由来原料への移行を迅速に進めています。企業は精密発酵、酵素抽出、無溶媒処理といった先端技術へ投資を集中させています。これらの進歩は、機能性・安定性・保存性を高めた天然風味調整剤の開発を目指しています。例えば2024年3月、BASFアロマイングリディエンツ社は「Isobionics Naturalβーカリオフィレン80」の発売によりIsobionics製品群を強化しました。純度80%を誇る本原料は、飲食品・香料など多様な用途に対応し、業界のクリーンラベルおよび植物由来イノベーションへの取り組みを浮き彫りにしています。こうした進展は、両潮流の結びつきが深まり、将来の製品開発に相互に影響を与え合うことを強調しています。

クリーンラベル原料の高コスト化

メーカーは、クリーンラベル原料の高価格化という課題に直面しており、消費者の期待に応えつつ経済的な実現可能性を確保すべく取り組んでおります。天然着色料を例にとりますと、合成品と比較して25~35%高い価格が設定されており、バリューチェーン全体で利益率が圧迫されております。この価格差には複数の要因が寄与しています:複雑な調達ネットワーク、天然抽出物の低い収率、天然原料に対する厳格な品質管理などです。例えば、ビートルートやターメリックといった天然着色料の調達には、季節的な収穫時期の調整や加工時の非汚染確保が必要であり、これがコスト増につながります。さらに、天然原料の生産には拡張性の限界があり、原材料が季節的にしか入手できないことも、コスト格差を拡大させる要因です。例えば、コチニール虫から得られる天然赤色着色料であるカルミンの生産は、労働集約的であり、虫の入手可能性の変動の影響を受けます。この格差は、クリーンラベル製品のプレミアム価格を合理化するために、戦略的な価格設定と消費者教育の必要性を浮き彫りにしています。

セグメント分析

2025年現在、食品用香料・増強剤はクリーンラベル原料市場において32.78%という圧倒的なシェアを占めております。これは製品の嗜好性確保と消費者受容の獲得において、同セグメントが果たす極めて重要な役割を裏付けるものです。この分野の顕著な存在感は、メーカーがよりクリーンな配合への移行を進めつつ、感覚的魅力を維持するという戦略的焦点を示しております。ジボダン、センシエント・テクノロジーズ、シンライズといった企業は、クリーンラベル製品への需要急増に対応し、天然香料ソリューションに多額の投資を行っています。例えば2024年3月、センシエント・フレーバーズ・アンド・エクストラクツは、高級料理製品で求められる人気のスモーキーな香りの全スペクトルを捉えた、新たな天然クリーンラベル香料シリーズ「スモークレス・スモーク」を発表しました。

一方、食品用着色料は急速に成長しており、2026年から2031年にかけてCAGR7.74%と予測される最も成長の速いセグメントとして注目されています。この急成長は主に、FDAが最近承認した3つの天然着色添加物--ガルディエリア抽出物ブルー、バタフライピー花抽出物、リン酸カルシウム--によるものです。さらに、飲料、菓子類、乳製品における天然着色料の採用増加が、このセグメントの拡大を後押ししています。同時に、食品保存料は革新的な植物由来の抗菌ソリューションへの顕著な移行を伴い、再興の兆しを見せています。例えば、ローズマリー抽出物や柑橘由来化合物が効果的な天然保存料として台頭しています。この移行により、製造業者は合成保存料に代わる選択肢を得ると同時に、保存安定性を損なうことなく製品を提供することが可能となります。

地域別分析

2025年、北米はクリーンラベル原料市場において34.78%のシェアを占めております。これは消費者の意識向上と厳格な規制状況によって支えられております。FDA(米国食品医薬品局)が石油由来の合成着色料の排除や食品表示の透明性向上に向けた最近の動きは、同地域の優位性をさらに確固たるものとしております。カナダでは健康志向の消費者による成長が見られる一方、メキシコでは急成長する中産階級と高まる健康意識が拡大を牽引しております。

欧州は2026年から2031年にかけてCAGR6.51%が見込まれ、最も成長が速い地域となる見込みです。これは厳格な規制基準と、自然派製品への強い消費者志向によるものです。欧州委員会の「クリーン産業協定」は、持続可能な生産を推進し行政負担を軽減することで、クリーンラベル製造業者の競争力を強化しています。英国とドイツが欧州市場を牽引しており、英国はブレグジット後の規制を乗り越え、食品原料の高水準を維持しています。一方、フランス、スペイン、イタリアでは、品質を重視する食文化の伝統を背景に堅調な成長が見られます。ロシアをはじめとする欧州諸国も、消費者の意識向上に伴い、徐々に市場シェアを拡大しつつあります。

消費者意識や規制の明確化における課題はあるもの、アジア太平洋地域はクリーンラベル原料市場において顕著な存在感を示しつつあります。中国とインドは膨大な中産階級人口を背景に、食品安全と品質への懸念の高まりを原動力として成長の基盤が整っています。洗練された食文化を持つ日本と、厳格な規制と健康志向の消費者を背景とするオーストラリアが主導的な役割を果たしています。採用率は地域によって異なり、先進国が最前線に立っています。都市化、可処分所得の増加、健康意識の高い若年層が、この地域の成長を後押ししています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 人工食品添加物に関連する健康問題

- 植物由来および有機原料への移行

- アレルゲンフリーおよびグルテンフリー製品への需要増加

- ビーガンおよびベジタリアン向け製品ラインの拡充

- 世界の健康危機がより健康的な食品選択の必要性を強調

- クリーンラベル製剤における企業の研究開発投資の増加

- 市場抑制要因

- クリーンラベル原料の高コスト

- 新興国における認知度の低さ

- 複雑な規制要件が市場参入を妨げる

- 安価な従来型原料との競合

- サプライチェーン分析

- 規制の見通し

- ポーターのファイブフォース

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 成分タイプ別

- 食品保存料

- 食品用甘味料

- 食品着色料

- 食品用水溶性多糖類

- 食品用香料および調味料

- その他の原材料の種類

- 形態別

- ドライ

- 液体

- 用途別

- ベーカリーおよび菓子類

- 乳製品および冷凍デザート

- 飲料

- 食肉および食肉製品

- ソースおよび調味料

- その他の用途

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- チリ

- ペルー

- その他南米

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- オランダ

- ポーランド

- ベルギー

- スウェーデン

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- インドネシア

- 韓国

- タイ

- シンガポール

- その他アジア太平洋地域

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- ナイジェリア

- エジプト

- モロッコ

- トルコ

- その他中東・アフリカ地域

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場ランキング分析

- 企業プロファイル

- Cargill Incorporated

- Archer Daniels Midland Company

- Ingredion Incorporated

- Tate and Lyle PLC

- Kerry Group PLC

- DSM-Firmenich

- International Flavors & Fragrances Inc.(IFF)

- Sensient Technologies Corporation

- Ajinomoto Co. Inc.

- Corbion N.V.

- Givaudan S.A.

- Roquette Freres S.A.

- Dohler GmbH

- Kalsec Inc.

- CP Kelco(J.M. Huber Corp.)

- Puratos Group

- Sudzucker AG

- Nexira SAS

- Limagrain Ingredients

- Camlin Fine Sciences Ltd.

第7章 市場機会と将来の展望

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 135 Pages

- 納期

- 2~3営業日