|

|

市場調査レポート

商品コード

1686578

シリコンメタル:市場シェア分析、産業動向・統計、成長予測(2025~2030年)Silicon Metal - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| シリコンメタル:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

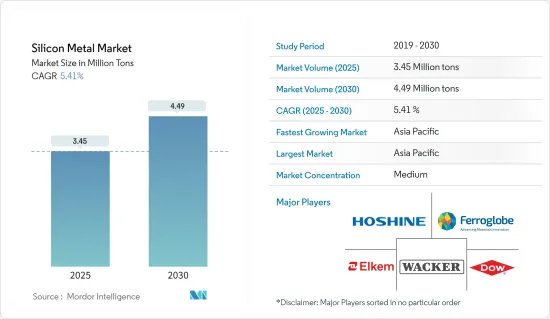

シリコンメタルの市場規模は2025年に345万トンと推定され、予測期間(2025~2030年)のCAGRは5.41%で、2030年には449万トンに達すると予測されています。

COVID-19はシリコンメタル市場の妨げとなりました。自動車、建設、エレクトロニクスなど、シリコンメタルを利用する多くの産業は、パンデミックの間、景気後退、個人消費の減少、生産とサプライチェーンの混乱により需要が減少しました。しかし、操業停止や規制が緩和されるにつれて、シリコンメタルを利用する産業は回復し、インフラプロジェクト、自動車生産、半導体製造、再生可能エネルギー設備からの需要が増加し、シリコンメタルの需要を押し上げました。

主なハイライト

- 自動車産業からの需要の急増、ソーラー電池産業での使用の増加、その他様々なエンドユーザーからの需要の増加が、シリコンメタルの世界の市場拡大につながると予想されます。

- しかし、エネルギーコストの変動がシリコンメタル市場の成長を妨げています。

- 現在の技術を改善することで生産コストを削減するいくつかの方策と、再生可能エネルギー部門からの需要の増加が、今後一定期間、市場関係者に成長機会をもたらすと予想されます。

- アジア太平洋は最も高い市場シェアを保持しており、予測期間中、シリコンメタル市場を独占する可能性が高いです。

シリコンメタル市場動向

市場を独占するソーラーパネルセグメント

- 現在販売されているモジュールの約95%を占めるシリコンは、ソーラー発電で最も広く使用されている半導体材料です。冶金用シリコンは、精製過程で半導体やソーラー電池の材料となる高純度シリコンに変換できます。そのため、ソーラー電池の製造に適しています。

- ソーラーエネルギーは、世界最大かつ急成長している分野のひとつです。国際エネルギー機関(IEA)によれば、このセクターは世界の純エネルギー容量の3分の2近くを占めています。

- 国際エネルギー機関(IEA)が発表したデータによると、2022年、ソーラー発電の生産量は過去最高の270TWh増加し、26%増の約1300TWhに達しました。ソーラー発電は、2022年にすべての再生可能技術の中で最も大幅な絶対的発電量の伸びを示し、史上初めて風力を上回りました。

- 米国は、2022年に導入されたインフレ削減法(IRA)にソーラー発電への手厚い新資金を盛り込みました。投資税額控除と生産税額控除は、ソーラー発電の設備容量とサプライチェーンの成長を大幅に後押しすると思われます。

- 国際エネルギー機関(IEA)が発表したデータによると、2022年にブラジルは約11ギガワットのソーラー発電容量を追加し、2021年の成長率を倍増させました。産業界や電力小売業者からの再生可能エネルギーに対する継続的な需要を考慮し、導入量は中期的にこの水準を維持すると予測されています。

- 新・再生可能エネルギー省(MNRE)が発表したデータによると、2022年末時点で、インドはソーラー発電の導入量において世界第4位の地位を占めています。ソーラー発電の累積設備容量は、2022年11月時点で約720万kWに達しています。現在、インドのソーラー発電料金は非常に競争力があり、グリッドパリティも達成されています。

- 上記の開発により、予測期間を通じてソーラー産業におけるシリコンメタルの市場が牽引されると予想されています。

アジア太平洋地域が市場を独占

- アジア太平洋、特に中国は世界最大のシリコンメタル生産国です。この地域は、石英や石炭のような原材料の豊富な埋蔵量と、低コストの労働力へのアクセスの恩恵を受け、大規模なシリコンメタル生産施設の設立を支えています。

- シリコンメタルの最も重要な用途は、シリコン接着剤、シーリング剤、潤滑剤、化学物質、その他の物質、アルミニウム合金です。自動車、建築・建設、工業、その他のエンドユーザー部門が、これらの製品の主な用途です。

- 中国では新エネルギー車の生産と販売が大幅に増加し、販売台数は2022年までに722万台に達し、世界のEV販売台数の64%を占めました。

- 予測期間中は、政府によるEV、ハイブリッド車、燃料電池車の普及促進が市場を牽引すると予測されます。この国での電気自動車需要の高まりは、半導体、アルミニウム合金、シリコン接着剤の必要性を高めています。

- 中国汽車工業協会(CAAM)が発表した報告書によると、2022年、中国は乗用車253万台、商用車58万台を含む311万台を輸出し、2021年比で54.4%増加しました。

- JinkoSolar、Trina Solar、JA Solarなど、世界のソーラー発電製造のトップ企業は中国に本社を置いています。中国でのソーラー電池製造は過去2年間で大幅に増加しています。国際エネルギー機関(IEA)が発表したデータによると、2022年に追加されるソーラー発電の容量は100GWで、2021年に比べて60%近く増加しており、中国はソーラー発電の容量追加という点でリードし続けています。

- 携帯電話、ノートパソコン、その他の電化製品の製造への投資は、中国における重要な投資分野です。今後の需要増に対応するため、世界中の大手メーカーが中国市場に多額の資本を投じています。

- これらの要因から、アジア太平洋地域の中国がシリコンメタル市場を独占すると予想されます。

シリコンメタル産業の概要

シリコンメタル市場は部分的に統合されています。主なプレーヤー(順不同)には、Hoshine Silicon Industry、Ferroglobe、Elkem ASA、Dow、Wacker Chemie AGなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 自動車産業からの需要急増

- ソーラー電池産業での使用の増加

- さまざまなエンドユーザーからのシリコン需要の増加

- 抑制要因

- エネルギーコストの変動

- その他の抑制要因

- 業界バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- 製品タイプ別

- 冶金グレード

- 化学グレード

- 用途別

- アルミニウム合金

- 半導体

- ソーラーパネル

- シリコン誘導体

- その他の用途(建設・インフラ)

- 地域別

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- マレーシア

- インドネシア

- タイ

- ベトナム

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- スペイン

- フランス

- トルコ

- ロシア

- ノルディック

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- ナイジェリア

- カタール

- エジプト

- アラブ首長国連邦

- その他中東とアフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Anyang Huatuo Metallurgy Co., Ltd.

- Dow

- Elkem ASA

- Ferroglobe

- Hoshine Silicon Industry Co., Ltd.

- Liasa

- Minasligas

- Mississipi Silicon

- PCC SE

- RIMA INDUSTRIAL

- RusAL

- Shin-Etsu Chemical Co., Ltd.

- Wacker Chemie AG

- Zhejiang kaihua yuantong silicon industry co. LTD.

第7章 市場機会と今後の動向

- 既存技術の革新による生産コスト削減への取り組み

- 再生可能エネルギー分野からの需要増加

The Silicon Metal Market size is estimated at 3.45 million tons in 2025, and is expected to reach 4.49 million tons by 2030, at a CAGR of 5.41% during the forecast period (2025-2030).

The COVID-19 hampered the silicone metal market. Many industries that utilize silicone metal, such as automotive, construction, and electronics, experienced decreased demand during the pandemic due to economic downturns, reduced consumer spending, and disruptions in production and supply chains. However, as lockdowns and restrictions eased, industries that utilize silicone metal recovered, and there was increased demand for silicone from infrastructure projects, automotive production, semiconductor manufacturing, and renewable energy installations, which boosted the demand for silicone metals.

Key Highlights

- Surging demand for silicone from the automotive industry, increasing use in the solar industry, and increasing demand for silicones from various other end users are expected to increase the market for silicone metal globally.

- However, volatility in energy costs is hindering the growth of the silicon metal market.

- Several measures to reduce production costs by improving current technologies and increasing demand from the renewable energy sector are expected to create growth opportunities for the market players in the upcoming period.

- The Asia-Pacific holds the highest market share and is likely to dominate the silicon metal market during the forecast period.

Silicon Metal Market Trends

Solar Panels Segment to Dominate the Market

- Silicon, which accounts for about 95% of the modules sold today, is the most extensively used semiconductor material in photovoltaics. In the process of purification, metallurgical silicon can be transformed into high-purity silicon that is used to make semiconductors and solar cells. Therefore, it is suitable for the manufacture of photovoltaic cells.

- Solar energy is one of the largest and fastest-growing sectors worldwide. The sector is responsible for nearly two-thirds of global net energy capacity, according to the International Energy Agency.

- According to the data published by the International Energy Agency (IEA), in 2022, solar PV production increased by a record 270 TWh, which increased by 26%, reaching almost 1300 TWh. It demonstrated the most considerable absolute generation growth of all renewable technologies in 2022, surpassing wind for the first time in history.

- The United States included generous new funding for solar PV in the Inflation Reduction Act (IRA) introduced in 2022. Investment and production tax credits will likely significantly boost the growth of PV capacity and supply chains.

- According to the data published by the International Energy Agency (IEA), in 2022, Brazil added almost 11 gigawatts of solar PV capacity, doubling its growth rate for 2021. In view of the continued demand for renewable energy from industry and power retailers, deployment is projected to be maintained at this level over the medium term.

- According to the data published by the Ministry of New and Renewable Energy (MNRE), India held the fourth position in solar PV deployment worldwide as of the end of 2022. The Cumulative installed capacity of solar power reached around 7.2 GW as of November 2022. Today, India's solar tariffs are very competitive, and grid parity has been achieved.

- The developments mentioned above are expected to drive the market for silicone metal in the solar industry through the forecast period.

Asia-Pacific to Dominate the Market

- Asia-Pacific, particularly China, is the largest producer of silicone metal globally. The region benefits from abundant reserves of raw materials like quartz and coal, as well as access to low-cost labor, which supports the establishment of large-scale silicon metal production facilities.

- The most critical applications of silicon metal are silicone adhesives, sealants, lubricants, chemicals, and other substances, as well as aluminum alloys. The automotive, building and construction, industrial, and other end-user sectors are the primary uses of these products.

- The production and sales of new energy vehicles increased significantly in China, with the number of units sold reaching 7.22 million by 2022, representing 64 % of all EV sales worldwide.

- The market is projected to be driven by the government's promotion of EVs, hybrids, and fuel-cell vehicles in the forecast period. The rising demand for electric vehicles in this country increases the need for semiconductors, aluminum alloys, and silicon adhesives.

- According to the report released by the China Association of Automobile Manufacturers (CAAM), in 2022, China exported 3.11 million vehicles, including 2.53 million passenger cars and 580,000 commercial vehicles, an increase of 54.4 % compared to 2021.

- The top global solar PV manufacturing companies, such as JinkoSolar, Trina Solar, and JA Solar, are headquartered in China. Solar cell manufacturing in China has been increasing significantly in the past two years. According to the data published by the International Energy Agency (IEA), with 100 GW capacity of solar PV added in 2022, almost 60% more than in 2021, China continues to lead in terms of solar PV capacity additions.

- Investment in the manufacture of mobile phones, laptops, and other electrical appliances is a significant area for investment in China. In order to meet the upcoming increase in demand, large manufacturers from around the world have invested substantial capital into China's market.

- Due to these factors, Asia-Pacific region China is expected to dominate the silicon metal market.

Silicon Metal Industry Overview

The silicon metal market is partially consolidated. The major players (not in any particular order) include Hoshine Silicon Industry Co., Ltd, Ferroglobe, Elkem ASA, Dow, and Wacker Chemie AG, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Surging Demand from the Automotive Industry

- 4.1.2 Increasing Use in the Solar Industry

- 4.1.3 Increasing Demand for Silicones from Different End Users

- 4.2 Restraints

- 4.2.1 Volatility in Energy Costs

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Product Type

- 5.1.1 Metallurgy Grade

- 5.1.2 Chemical Grade

- 5.2 Application

- 5.2.1 Aluminum Alloys

- 5.2.2 Semiconductors

- 5.2.3 Solar Panels

- 5.2.4 Silicone Derivatives

- 5.2.5 Other Applications (Construction and Infrastructure)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Indonesia

- 5.3.1.7 Thailand

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 Spain

- 5.3.3.5 France

- 5.3.3.6 Turkey

- 5.3.3.7 Russia

- 5.3.3.8 NORDIC

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Nigeria

- 5.3.5.4 Qatar

- 5.3.5.5 Egypt

- 5.3.5.6 UAE

- 5.3.5.7 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Anyang Huatuo Metallurgy Co., Ltd.

- 6.4.2 Dow

- 6.4.3 Elkem ASA

- 6.4.4 Ferroglobe

- 6.4.5 Hoshine Silicon Industry Co., Ltd.

- 6.4.6 Liasa

- 6.4.7 Minasligas

- 6.4.8 Mississipi Silicon

- 6.4.9 PCC SE

- 6.4.10 RIMA INDUSTRIAL

- 6.4.11 RusAL

- 6.4.12 Shin-Etsu Chemical Co., Ltd.

- 6.4.13 Wacker Chemie AG

- 6.4.14 Zhejiang kaihua yuantong silicon industry co. LTD.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Efforts to Reduce the Cost of Production by Innovating the Existing Technology

- 7.2 Increasing Demand from Renewable Energy Sector