|

|

市場調査レポート

商品コード

1403874

家庭用電化製品:市場シェア分析、産業動向と統計、2024~2029年の成長予測Home Appliances - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

|

|

|||||||

|

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。 |

|||||||

| 家庭用電化製品:市場シェア分析、産業動向と統計、2024~2029年の成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

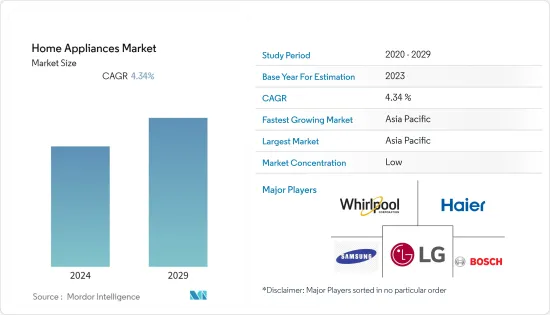

家庭用電化製品市場規模は2024年に5,372億8,000万米ドルと推定・予測され、予測期間中のCAGRは4.34%を記録し、2029年には6,645億3,000万米ドルに達すると予測されます。

技術の進歩はスマート家庭用電化製品の開拓につながり、予測期間中の市場成長を促進すると予想されます。スマート家庭用電化製品は高度な機能を提供し、エネルギー効率も高いです。消費者の可処分所得の増加、高い生活水準、快適さへのニーズは、消費者が既存の家庭用電化製品をよりスマートなバージョンにアップグレードすることを促し、これがさらに市場需要に影響を与えると予想されます。消費者が家庭用電化製品を購入するのは、手間を省き、時間を節約するためです。製品革新、新製品開拓、製品差別化、多数の付加価値機能の統合が、今後数年間の市場需要をさらに押し上げると予想されます。同市場は、家庭用電化製品の有効性、多様性、持続可能性、スタイリッシュなデザイン、スマート機能といった動向によって大きく牽引されています。家庭用電化製品は使いやすく、生活の質の向上に役立つため、市場は大きな成長機会を提供しています。さらに、市場は持続可能性とエネルギー効率の面で新たな動向を見せつつあり、それによって、幸福を支持しつつ、いくつかの家事作業を簡素化しています。高品質の素材と審美的に美しいデザインが、革新的で多様な機能性と組み合わされることで、市場成長の道が開かれます。デザインは白物家庭用電化製品の重要な側面です。

Wi-FiやBluetoothのような無線技術は、スマートフォンやタブレットで使用したり、アクセスしたりすることができます。しかし、こうした技術を家庭用電化製品(エアコンなど)に搭載することは、メーカーによる製品差別化の手段であり、ハイテクに敏感な消費者を魅了しています。ネットワーク・インフラの改善は、ブロードバンドとインターネットの普及率の向上につながった。そのため、消費者は利便性を求めて、ワイヤレスで技術的に先進的な製品を選ぶようになっています。特に新興経済諸国では、白物家庭用電化製品の所有に関連するコストが低いことも、市場成長の機会となっています。さらに、先進地域での買い替え販売の増加も市場需要を牽引すると予想されます。これは、急速な都市化と相まって一人当たり所得が上昇していることに起因していると考えられます。

家庭用電化製品の動向

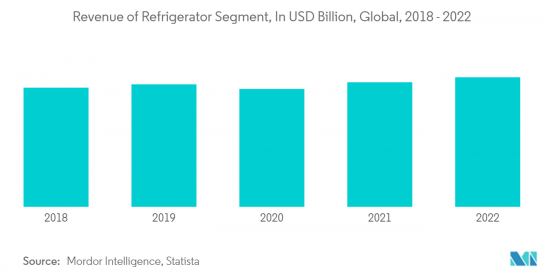

冷蔵庫セグメントが大きな市場シェアを占める

冷蔵庫は、食品や食材を保存するための安全で簡単かつ便利な方法と考えられています。可処分所得の増加、スマートでエネルギー効率の高い冷蔵庫ユニットの入手可能性、核家族化の進展などが、家庭用冷蔵庫の需要急増につながっています。シングルドア冷蔵庫は、コスト効率が高く、使いやすく、冷凍庫が内蔵されている場合とされていない場合があるため、最も広く使用されているドアタイプです。一方、フレンチドア冷蔵庫は、使いやすさとスマートな機能により急速に普及しています。とはいえ、市場関係者は環境への影響を最小限に抑えた新モデルを出そうとしています。古い冷蔵庫の使用をやめ、定期的なメンテナンスを行うことで、有害な排出物を減らし、環境汚染を抑制することができると思われます。

アジア太平洋地域が家庭用電化製品市場を独占している

中国のハイアール、Midea、Gree、Hisense、韓国のサムスン、LG、日本のパナソニック、シャープ、日立、インドのVideoconなどの地域ブランドが、アジア太平洋地域の家庭用電化製品市場をほぼ独占しています。アジア太平洋地域のスマート家庭用電化製品市場は急成長が見込まれています。日本、シンガポール、香港、インドネシアなどの新興諸国は、エネルギーコストや人件費の上昇、消費者の高い購買力、スマートシティやスマート家庭用電化製品に対する意識の高まりなどを背景に、スマート家庭用電化製品の販売台数の増加が見込まれています。中国は、省エネ家庭用電化製品を優遇する政府の政策、不動産市場の成長、暑い気候により、従来型エアコンの需要が数量ベースで世界最高となっています。

家庭用電化製品産業の概要

家庭用電化製品市場は非常に細分化されており、多くのプレーヤーが存在します。市場シェアでは、ワールプール、ハイアール、サムスン電子、LG電子、ボッシュが家庭用電化製品市場を独占しています。しかし、技術の進歩や製品の革新に伴い、中堅・中小企業は新規契約を獲得し、新市場を開拓することで、市場での存在感を高めています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場の洞察と力学

- 市場概要

- 市場促進要因

- 利便性と自動化のためのコネクテッド家庭用電化製品の採用増加

- 市場抑制要因

- 消費者の嗜好とライフスタイル動向の変化が家庭用電化製品の需要に影響

- 市場機会

- IoTや音声制御などのスマートホーム技術の家庭用電化製品への統合

- バリューチェーン/サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 市場における技術的進歩に関する洞察

- COVID-19の市場への影響

第5章 市場セグメンテーション

- 製品別

- 主要家庭用電化製品

- 冷蔵庫

- 冷凍庫

- 食器洗い機

- 洗濯機

- オーブン

- エアコン

- その他主要家庭用電化製品

- 小型家庭用電化製品

- コーヒー/ティーメーカー

- フードプロセッサー

- グリル&ロースター

- 掃除機

- その他小型家庭用電化製品

- 主要家庭用電化製品

- 流通チャネル別

- マルチブランドストア

- 専門店

- オンライン

- その他の流通チャネル

- 地域別

- 北米

- 南米

- 欧州

- アジア太平洋

- 中東・アフリカ

第6章 競合情勢

- 企業プロファイル

- Haier

- Whirlpool Corporation

- Samsung Electronics

- LG Electronics

- Bosch

- Sony

- Midea

- Electrolux

- Philips

- Panasonic Corporation*

第7章 今後の動向

第8章 免責事項

The Home Appliances Market size is estimated at USD 537.28 billion in 2024 and is expected to reach USD 664.53 billion by 2029, registering a CAGR of 4.34% during the forecast period.

Technological advancements have led to the development of smart appliances and are expected to drive market growth over the forecast period. Smart appliances offer advanced features and are more energy-efficient. The rise in consumer disposable income, high living standards, and the need for comfort encourage consumers to upgrade their existing appliances to smarter versions, which is further expected to impact the market demand. Consumers widely purchase home appliances as they offer ease, diminish efforts, and save time. Product innovation, new product development, product differentiation, and integration of numerous value-added features are further expected to catapult the market demand over the next few years. The market is considerably driven by trends such as effectiveness, diversity, sustainability, stylish design, and smart functionality of home appliances. The home appliance market offers significant growth opportunities as they are easy to use and help improve the quality of life. Moreover, the market is beholding new trends in terms of sustainability and energy efficiency, thereby simplifying several household tasks while endorsing well-being. High-quality materials and aesthetically pleasing designs combined with innovative and diverse functionalities offer avenues for market growth. Design is an important aspect of these white goods.

Wireless technologies like Wi-Fi and Bluetooth can be used in or accessed by smartphones and tablets. But the inclusion of these technologies in home appliances (like air conditioners) is a means of product differentiation by manufacturers that is enticing tech-savvy consumers. The improvement in network infrastructure has translated into better broadband and internet penetration. Therefore, consumers are increasingly opting for wireless and technologically advanced products, mostly for the convenience they offer. The low cost associated with the ownership of white goods, particularly in developing economies, also provides opportunities for market growth. Furthermore, a rise in replacement sales in developed regions is also expected to drive the market demand. This may be attributed to a rise in per capita income, coupled with rapid urbanization.

COVID-19 disrupted the global supply chain of the major home appliances and consumer electronic brands. China was one of the largest consumers and producers of various home appliances and consumer electronics products, but it also catered to a wide range of countries by exporting several input supplies that were essentially used to produce finished goods. The shutdown of the production in China forced other consumer electronics makers based in the United States and Europe to temporarily hold the production of the finished goods. This led to an increase in the supply and demand gap.

Home Appliance Market Trends

The Refrigerators Segment Accounts for a Significant Market Share

Refrigerators are considered a safe, easy, and convenient way to preserve food and food products. Rising disposable income, availability of smart and energy-efficient refrigerator units, and a widening base of nuclear families are leading to an upsurge in demand for refrigerators for household applications. Single-door refrigerators are the most widely used door type as they are cost-efficient, easy to use, and may or may not contain an inbuilt freezer. The French door refrigerators, on the other hand, are rapidly gaining popularity owing to the ease of usability and smart features introduced in these refrigerators. Nevertheless, market players are trying to come up with new models that have a minimum impact on the environment. Abandoning the use of old refrigerators and regular servicing are likely to reduce harmful emissions, thereby curtailing environmental pollution.

Asia-Pacific is Dominating the Home Appliances Market

Regional brands, including Haier, Midea, Gree, Hisense from China, Samsung, LG from Korea, Panasonic, Sharp, Hitachi from Japan, and Videocon from India, largely dominate the market for home appliances in the Asia-Pacific region. The smart appliances market in Asia-Pacific is expected to grow at a rapid rate. Developed countries like Japan, Singapore, Hong Kong, and Indonesia are expected to register an increase in the sales of smart appliances, mostly owing to the rising energy and labor costs, the high purchasing power of consumers, and greater awareness about smart cities and smart integrated appliances. China has the highest demand for conventional air conditioners, by volume, across the globe, owing to government policies that favor energy-saving appliances, a growing property market, and hot weather.

Home Appliance Industry Overview

The Home Appliance market is highly fragmented, with many players. In terms of market share, some major international players dominating the home appliances market are Whirlpool, Haier, Samsung Electronics, LG Electronics, and Bosch. However, with technological advancements and product innovations, mid-size to smaller companies are increasing their market presence by securing new contracts and tapping into new markets.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS AND DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Adoption of Connected Home Appliances for Convenience and Automation

- 4.3 Market Restraints

- 4.3.1 Changing Consumer Preferences and Lifestyle Trends Influencing Demand for Certain Appliances

- 4.4 Market Opportunities

- 4.4.1 Integration of Smart Home Technology, such as IoT and Voice Control, in Appliances

- 4.5 Value Chain/Supply Chain Analysis

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Insights on Technological Advancements in the Market

- 4.8 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Product

- 5.1.1 Major Appliances

- 5.1.1.1 Refrigerators

- 5.1.1.2 Freezers

- 5.1.1.3 Dishwashing Machines

- 5.1.1.4 Washing Machines

- 5.1.1.5 Ovens

- 5.1.1.6 Air Conditioners

- 5.1.1.7 Other Major Appliances

- 5.1.2 Small Appliances

- 5.1.2.1 Coffee/Tea Makers

- 5.1.2.2 Food Processors

- 5.1.2.3 Grills and Roasters

- 5.1.2.4 Vacuum Cleaners

- 5.1.2.5 Other Small Appliances

- 5.1.1 Major Appliances

- 5.2 By Distribution Channel

- 5.2.1 Multi-Branded Stores

- 5.2.2 Specialty Stores

- 5.2.3 Online

- 5.2.4 Other Distribution Channels

- 5.3 Geography

- 5.3.1 North America

- 5.3.2 South America

- 5.3.3 Europe

- 5.3.4 Asia-Pacific

- 5.3.5 Middle-East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Haier

- 6.1.2 Whirlpool Corporation

- 6.1.3 Samsung Electronics

- 6.1.4 LG Electronics

- 6.1.5 Bosch

- 6.1.6 Sony

- 6.1.7 Midea

- 6.1.8 Electrolux

- 6.1.9 Philips

- 6.1.10 Panasonic Corporation*