|

市場調査レポート

商品コード

1851333

石油・ガスオートメーション:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Oil & Gas Automation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 石油・ガスオートメーション:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年07月03日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

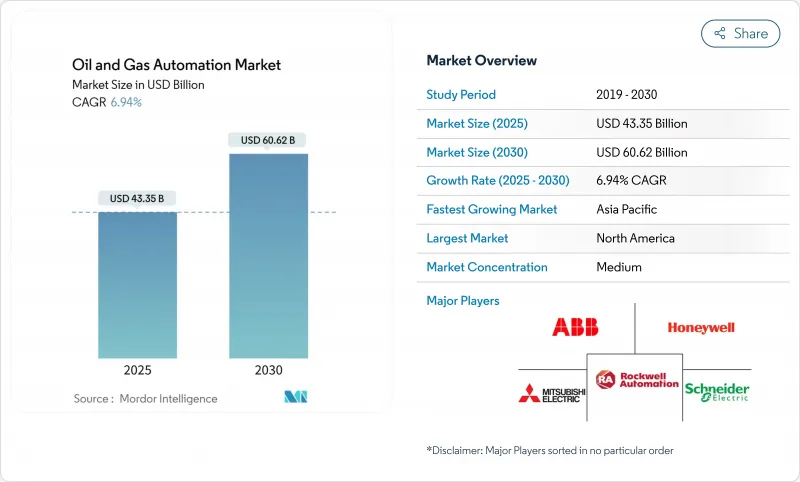

石油・ガスオートメーション市場規模は、2025年に433億5,000万米ドルに達し、2030年には606億2,000万米ドルに上昇し、予測期間中のCAGRは6.9%を記録する見込みです。

事業者は、サプライチェーンが逼迫し、エネルギー移行目標が強化される中、ダウンタイムを抑制し、生産性を向上させるために、インテリジェントフィールドプラットフォーム、エッジAI分析、自律検査ツールを導入しています。特にIEC 61511とISA-84に沿った安全規制が義務化され、ミリ秒単位で危険に対応する安全計装システムの導入が加速しています。アジア太平洋とアフリカにおけるLNGインフラの拡大は、高圧、-160℃の環境に対応する極低温グレードの制御システムに対する新たな需要を引き出しています。最後に、事業者がランサムウェアや国家による攻撃に対して運用技術(OT)環境を強化するにつれて、サイバーセキュリティ予算が増加し、現在ではオートメーション総支出の15~20%を占めるようになり、プロジェクトの経済性が再構築されつつあります。

世界の石油・ガスオートメーション市場の動向と洞察

デジタル油田プラットフォームの採用増加

リアルタイムデジタルプラットフォームは、IoTセンサー、機械学習モデル、クラウド分析を統合ダッシュボードに融合し、意思決定サイクルを数分から数秒に短縮します。デボン・エナジー社は、AIによる掘削調整を導入した後、坑井の寿命を25%延ばしました。ライブの操業データと同期したバーチャルツインにより、エンジニアは物理的な資産を危険にさらすことなくシナリオをテストすることができます。このアプローチは、ダウンホールの状態が刻々と変化する非従来型の貯留層で特に有効です。

遠隔監視と予知保全のための近代化CAPEX

オペレーターは、現場への訪問を減らし、安全への露出を減らす遠隔監視ツールに資本を振り向けています。エンブリッジのAzureベースのパイプライン分析では、脅威の検出が30%改善されました。予測アルゴリズムが振動や熱の動向を調査し、数週間前に故障を発見することで、信頼性を高めながら定期点検コストを最大50%削減しました。

原油価格の変動がOPEXとCAPEXサイクルに影響

原油価格の変動と支出シフトの間に6ヶ月のタイムラグがあるため、小規模の生産者は、キャッシュフローが逼迫しているときにオートメーションのアップグレードを遅らせざるを得ません。料金体系を生産量に合わせるサブスクリプションベースの自動化サービスは、先行リスクを低減し、不況時の流動性を維持するため、支持を集めています。

セグメント分析

ソフトウェアは、2024年の売上高の66.7%を占め、予知保全と自律的オペレーションを強化する分析エンジンによって石油・ガスオートメーション市場を支えています。金額ベースでは、このコンポーネントは2024年の石油・ガスオートメーション市場規模の289億米ドルを占めました。サービスは、規模は小さいもの、事業者がAIの設定やサイバーセキュリティの強化をアウトソーシングするため、CAGRは8.5%と予測されています。

ソフトウェアの成長は、掘削の普及率を35~45%引き上げるエッジAIパッケージによって強化されます。一方、24時間モニタリングと成果ベースの保証をバンドルしたサービス契約は、プロバイダーを製品サプライヤーからパフォーマンス・パートナーへと移行させる。ハードウェアは、センサーグリッドや堅牢なエッジデバイスに不可欠であることに変わりはないが、仮想化された制御ロジックがソフトウェア層に移行するにつれて、そのシェアは徐々に低下すると予想されます。

上流工程では、自律掘削・生産最適化プラットフォームがシェール井の何千ものダウンホールパラメータを較正したため、2024年のプロセス収益の59.1%を稼いです。これは石油・ガスオートメーション市場規模のおよそ256億米ドルに相当します。中流事業は、世界的なLNGターミナルの建設とパイプラインのデジタル化により、規模は小さいがCAGR 8.3%で成長しています。

SLBのような上流企業は、1ラテラルで25回の自動ジオステアリング補正を実演し、完全自律型リグへのシフトを示唆しました。中流企業では、クラウドリンクされたSCADAシステムによって、数千キロメートルに及ぶリアルタイムの漏水検知とバルブの遠隔操作が可能になり、事故対応時間が数時間から数分に短縮されます。下流の事業所では、エネルギー使用量を削減し、排出量を削減するAI指向の蒸留塔を試験的に導入しています。

地域分析

北米が2024年の収益シェア37.1%で石油・ガスオートメーション市場をリードし、AI主導の掘削とパッドの最適化の先駆者であるシェール開発企業に支えられています。リグ数が変動しても、学習と適用のサイクルが持続することで、この地域の生産性は高く維持されています。この地域のサイバーセキュリティ体制も成熟しており、事業者は連邦政府のガイドラインで義務付けられたゼロトラストOTフレームワークを採用しています。

アジア太平洋地域の2030年までのCAGRは7.5%になる見込みです。中国はよりクリーンな燃料を生産するために製油所の近代化を進めており、インドは深海鉱区で上流のデジタル化を加速させています。東南アジアの大規模なLNG輸入プロジェクトは、供給を確保し、断続的な再生可能エネルギーとの電力網のバランスをとるために、AIを活用した低温制御を頼りにしています。各国政府は、排出量抑制と安全性強化のためにデジタルツインを支援し、技術採用を推進しています。

欧州は厳しい安全・環境規制の下、安定した支出を維持。ドイツとフィンランドの新しいLNG再ガス化ユニットは、SIL-3安全レイヤとNIS 2.0サイバーセキュリティ指令を満たすDCSプラットフォームを統合しています。中東の国営石油会社は政府系ファンドの支援を受け、ADNOCの9億2,000万米ドルのENERGYaiプログラムに代表されるように、成熟した炭酸塩貯留層全体でAI主導の坑井モニタリングを拡大しています。アフリカと南米は依然として新興の採用企業であり、技術移転と資金調達のために合弁パートナーを活用することが多いです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- デジタル油田プラットフォームの採用増加

- 遠隔監視と予知保全のための近代化CAPEX

- 安全システム規制の義務化

- APACとアフリカにおけるLNGとミッドストリーム建設

- 危険な現場でのリアルタイム分析のためのエッジAIの展開

- オフショア資産向け自律点検ドローンとロボティクス

- 市場抑制要因

- 原油価格の変動がOPEXとCAPEXサイクルに与える影響

- サイバーリスクとOTセキュリティ・コンプライアンス・コストの増大

- 高額な自動化初期投資とROIの不確実性

- レガシーシステムの相互運用性

- バリューチェーン分析

- テクノロジーの展望

- 規制情勢

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 投資分析

- マクロ経済動向の市場への影響評価

第5章 市場規模と成長予測

- コンポーネント別

- ハードウェア

- ソフトウェア

- サービス

- プロセス別

- 上流

- 中流

- 川下

- 技術別

- センサーとトランスミッター

- 分散型制御システム(DCS)

- プログラマブルロジックコントローラ(PLC)

- 監視制御およびデータ収集(SCADA)

- 安全計装システム(SIS)

- その他のテクノロジー

- 用途別

- 掘削と完成

- 生産と坑井の最適化

- パイプラインと輸送

- 精製・石油化学

- LNGターミナルと貯蔵

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- 中東

- サウジアラビア

- アラブ首長国連邦

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- エジプト

- ナイジェリア

- その他アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- ABB Ltd.

- Honeywell International Inc.

- Siemens AG

- Schneider Electric SE

- Emerson Electric Co.

- Rockwell Automation Inc.

- Mitsubishi Electric Corp.

- Yokogawa Electric Corp.

- Eaton Corp.

- Dassault Systemes SE

- Bosch Rexroth AG

- Texas Instruments Inc.

- Johnson Controls International plc

- Halliburton Co.

- Schlumberger NV

- Baker Hughes Co.

- Weatherford International plc

- AVEVA Group plc

- Aspen Technology Inc.

- Flowserve Corp.