|

|

市場調査レポート

商品コード

1444573

缶詰スープ:市場シェア分析、業界動向と統計、成長予測(2024-2029)Canned Soup - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 缶詰スープ:市場シェア分析、業界動向と統計、成長予測(2024-2029) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

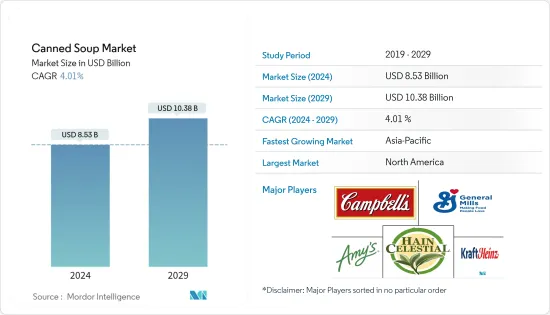

缶詰スープ市場規模は2024年に85億3,000万米ドルと推定され、2029年までに103億8,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に4.01%のCAGRで成長します。

主なハイライト

- 缶詰スープの促進要因としては、食品保存方法の改善による食材の保存期間の延長、都市化率の上昇、多忙なライフスタイル、インスタント食品の需要の急増などが挙げられます。また、核家族化や世帯の可処分所得の増加に伴い、消費者の食習慣も変化しており、インスタント食品への関心が高まっています。

- その結果、メーカーは消費者のニーズに応える革新的な製品を導入しています。たとえば、2022年 1月、レックスキャニングコーポレーションはマレーシアの缶詰スープカテゴリへの新規参入者としてレックスマッシュルームスープを発売しました。本品は凝縮スープなので手早く調理できます。主な原材料には、水、キャノーラ油、小麦粉、ボタンマッシュルーム、粉乳、しいたけフレーク、分離大豆たんぱく、オニオンパウダー、ガーリックパウダー、黒胡椒が含まれます。同社はまた、スープの賞味期限は36か月だと主張しています。

- しかし、市場の成長を妨げる可能性がある最も頻繁に発生する問題は、包装の腐食、過剰な保存料や着色料の含有量、包装から果物への錫やカドミウムなどの物質の移行です。

缶詰スープ市場動向

コンビニエンス製品への支出の増加

- インスタント食品市場は世界中で急速に成長しており、主にミレニアル世代を中心に、月々の支出の3分の1近くをインスタント食品や持ち歩き用のスナック製品に投資する消費者が増えています。堅調な流通チャネルにより、缶詰スープなどのインスタント食品の売上が大幅に増加しており、予測期間中も売上は継続すると予想されます。

- スープは世界中のさまざまな料理の一部であるため、オーガニックや減塩などのさまざまな健康強調表示を記載したRTE缶詰スープは、便利で健康的な食品を求める時間に制約のある消費者の中で強い注目を集めています。この市場は主に、食品および飲料への支出の増加、賞味期限の長い製品の導入、衝動買いの増加、時間不足によるすぐに調理できるインスタント食品の需要の増加によって牽引されています。

- たとえば、2022年9月にパシフィックフーズは、新しいオーガニック缶詰のインスタントスープと植物ベースのチリの発売を発表しました。同社はまた、再活性化されたラインには、野菜レンズ豆やチキン&ワイルドライスなど、再調整されたビーガンおよび非ビーガン品種も含まれていると主張しています。

- 経済の発展、労働者階級の人口の増加、消費者のライフスタイルの進化により、缶詰スープなどのインスタント食品への支出が顕著に増加しています。

- 世界銀行によると、2021年の中国の女性労働参加率は61.61%でした。こうした動向、缶詰スープは世界中の家庭の食料庫に欠かせないものとなっています。さらに、缶詰のフルーツが容易に入手できること、および生のフルーツに比べて缶詰のスープはより安価なコストでより優れた栄養価を提供するという認識により、缶詰スープの需要が高まります。

- 可処分所得のある若い消費者は、新製品(その多くは便利な食品)を試してみる傾向が高く、非伝統的な食習慣を持っているため、主要な市場促進要因力となっています。さらに、新しいハイブリッド勤務パターンは、予見可能な将来に家庭でより多くの缶詰食品が消費されることを示しています。したがって、上記のすべての点は市場にプラスの影響を与えます。

北米が最大の市場として浮上

- 北米などの地域では肥満や健康意識を高めるキャンペーンが増加しており、その結果、保存料の含有量を最小限に抑えた、天然で新鮮な食材を含む包装スープの需要が高まっています。容器入りスープの消費量の増加により、缶詰スープ市場は、主要メーカーが新しいフレーバーや味わいのバリエーション、また健康強調表示に関する新しいバリエーションを発売することで製品範囲を拡大する道を切り開きました。

- 北米のスープ市場は確立されており、この地域の自主的な生産能力により、外国のスープメーカーが缶詰を含むさまざまな包装技術を使用してビジネスを拡大できる潜在的な市場となっています。製品の種類の増加、健康およびウェルネス製品の消費の増加、市場プレーヤーによる積極的なプロモーションにより、予測期間中に缶詰スープ市場の成長が促進されると予測されます。

- さらに、多くの消費者は、持続可能性を促進し、オーガニックおよび天然成分を含み、クリーンでより正確なラベルが付いている製品を積極的に探しています。その結果、メーカーはヴィーガンで持続可能な製品の発売を計画しています。たとえば、2022年12月、Modern Plant Based Foodsのポートフォリオ企業であるKitskitchen Health Foods Inc.は、植物ベースのスープラインのプレミアム乾燥および缶詰バリエーションの初期研究開発を開始しました。同社によれば、この製品によりキットキッチンは28億米ドル規模の缶詰スープ市場に参入できるようになるといいます。

- さらに、この地域の市場成長は主に、急速な経済発展、顧客の食習慣や好みの変化、風味豊かで便利な食品への需要の増加による缶詰スープ産業への投資の増加によるものです。こうして、北米アメリカ地域全体で缶詰スープ市場を牽引しました。

缶詰スープ業界の概要

缶詰スープ市場は、世界市場の大きなシェアを占める世界および地域プレーヤーの数が増加しているため、細分化されています。多様な製品ポートフォリオには、濃縮スープ、電子レンジ対応、すぐに食べられるスープ、オーガニックスープなどがあります。キャンベルスープカンパニーは基準年の缶詰スープ市場で最大のシェアを占めました。過去数年間、新興国での事業拡大が同社の成長を促進してきました。市場の他の主要企業には、ConAgra Foods、General Mills、Subo Foods、The Kraft Heinz Company、General Mills、Unilever、およびAmy's Kitchenが含まれます。

さらに、各企業は、既存の製品とは異なる独自の製品にするために、天然由来の成分を含む新しい革新的な製品を導入してきました。急速に発展する市場の性質により、新製品のイノベーションは、市場の消費者の変化するニーズを理解するのに役立つため、最も一般的に使用される戦略となっています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- インスタント食品への支出の増加

- ビーガン食品の成長傾向が植物ベースの缶詰スープ市場を牽引

- 市場抑制要因

- 缶詰スープ製品に含まれる食品添加物は市場の成長を妨げる可能性があります

- 業界の魅力- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- タイプ

- 濃縮

- RTE

- カテゴリー

- 従来型

- オーガニック

- 流通チャネル

- スーパーマーケット/ハイパーマーケット

- コンビニ/食料品店

- 食品専門店

- オンライン小売店

- その他の流通チャネル

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- その他北米

- 欧州

- スペイン

- 英国

- ドイツ

- フランス

- イタリア

- ロシア

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東とアフリカ

- 南アフリカ

- アラブ首長国連邦

- その他中東およびアフリカ

- 北米

第6章 競合情勢

- 最も採用されている戦略

- 市場シェア分析

- 企業プロファイル

- Campbell Soup Company

- General Mills Inc.

- Hain Celestial Group Inc.

- The Kraft Heinz Company

- Unilever PLC

- Amy's Kitchen Inc.

- Baxters Food Group Limited

- Bar Harbor Foods

- BCI Foods Inc.

- Sprague Foods Ltd

- F Whitlock &Sons

第7章 市場機会と将来の動向

The Canned Soup Market size is estimated at USD 8.53 billion in 2024, and is expected to reach USD 10.38 billion by 2029, growing at a CAGR of 4.01% during the forecast period (2024-2029).

Key Highlights

- The driving factors for canned soups include the increased shelf life of ingredients due to better usage of food preservation methods, an increase in the rate of urbanization, busy lifestyles, and a surge in demand for convenience foods, among other factors. Also, an increase in nuclear households and rising disposable incomes of households have led to changes in the food consumption habits of consumers, with convenience foods finding a major inclination among consumers.

- As a result, manufacturers are introducing innovative products to address consumer needs. For instance, in January 2022, Rex Canning Corporation launched Rex Mushroom Soup as a new entrant in the canned soup category in Malaysia. The product is a condensed soup and can be prepared quickly. The key ingredients include water, canola oil, wheat flour, button mushroom, milk powder, shitake flakes, isolated soy protein, onion powder, garlic powder, and black pepper. The company also claims that the soup has a shelf life of 36 months.

- However, the most frequent problems that have the potential to hamper the growth of the market are corrosion of packaging, excessive content of preservatives and coloring, as well as migration of materials from the packaging into the fruit, such as tin or cadmium.

Canned Soup Market Trends

Rise in Spending on Convenience Products

- The convenience food products market has been growing rapidly worldwide, with an increasing number of consumers, primarily millennials, investing nearly a third of their monthly expenditure on ready-to-eat or on-the-go snack products. Robust distribution channels have strongly augmented the sales of convenience foods, including canned soups, which are expected to continue during the forecast period.

- As soups are a part of several cuisines worldwide, canned ready-to-serve soups with various health claims, such as organic and low-sodium, have gained strong attention among the growing number of time-constrained consumers who are seeking convenient yet healthy food products. The market is primarily driven by rising expenditure on food and beverage, introducing products with longer shelf life, increasing impulse purchasing, and growing demand for convenience foods that can be prepared quickly due to a shortage of available time.

- For instance, in September 2022, Pacific Foods announced the launch of its New Organic Canned Ready-to-Serve Soups and Plant-Based Chilis. The company also claims that its reinvigorated line also features reformulated vegan and non-vegan varieties, such as Vegetable Lentils and Chicken and Wild Rice.

- The rise in the economy, growing working-class population, and evolving consumer lifestyle show a notable rise in the expenditure on convenience food products, such as canned soups.

- According to the World Bank, China had 61.61% female labor participation in 2021. These trends have made canned soups a vital part of the pantries of families worldwide. Additionally, the easy availability of canned fruits and the perception that canned soups deliver better nutritional value at cheaper costs in contrast to fresh fruits enhance the demand for canned soups.

- Younger consumers with disposable incomes are more likely to try new products (many of which are convenient food products) and have non-traditional eating habits, hence acting as major market drivers. Additionally, the new hybrid working patterns point to a larger number of canned meals being consumed at home for the foreseeable future. Therefore, all the above-mentioned points positively affect the market.

North America Emerges as the Largest Market

- The increasing instances of obesity and health awareness campaigns in regions such as North America have resulted in the demand for packaged soups that contain natural and fresh ingredients with minimum preservative content. Owing to the increasing consumption of packaged soups, the canned soup market has paved the way for key manufacturers to expand their product range by launching new flavor and taste variants and new variants concerning health claims.

- As the North American soup market is well established, the region's autonomous production capabilities have made it a potential market for foreign soup manufacturers to expand their business using different packaging techniques, including canned. Increasing product varieties, increasing consumption of health and wellness products, and active promotions by the players in the market are projected to propel the growth of the canned soup market during the forecast period.

- Furthermore, many consumers are actively seeking out products that promote sustainability, contain organic and natural ingredients, and have clean and more precise labels. As a result, manufacturers are planning to launch products that are vegan and sustainable. For instance, in December 2022, Modern Plant Based Foods' portfolio company, Kitskitchen Health Foods Inc., commenced initial R&D for premium dried and canned variations of its plant-based soups line. As per the company, the product will allow Kitskitchen to tap into the USD 2.8 billion-dollar canned soup market.

- Additionally, the region's market growth is mainly attributed to the growing investment in the canned soup industry due to the rapid economic development, changing customer dietary habits and preferences, and increasing demand for flavorful, convenient food products. Thus, driving the canned soup market across the North AAmericanregion.

Canned Soup Industry Overview

The canned soup market is fragmented due to a growing number of global and regional players accounting for a major share of the global market. The diversified product portfolio includes condensed, microwavable, ready-to-eat, and organic soups. Campbell Soup Company accounted for the largest share of the canned soup market in the base year. Over the last few years, expanding in emerging economies has helped boost the company's growth. The other key players in the market include ConAgra Foods, General Mills, Subo Foods, The Kraft Heinz Company, General Mills, Unilever, and Amy's Kitchen.

Further, the companies have been introducing new and innovative products with the inclusion of naturally derived ingredients so as to make their product unique from the existing products. Owing to the rapidly developing nature of the market, new product innovation has become the most commonly used strategy among all, as it helps in understanding the changing needs of the consumers in the market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Increasing Expenditure on Convenience Food Products

- 4.1.2 The Growing Trend of Vegan Food Products Drives the Market of Plant-based Canned Soup Market

- 4.2 Market Restraints

- 4.2.1 Food additives present in Canned Soup products can hinder the market growth

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Condensed

- 5.1.2 Ready-to-Eat

- 5.2 Category

- 5.2.1 Conventional

- 5.2.2 Organic

- 5.3 Distribution Channel

- 5.3.1 Supermarkets/Hypermarkets

- 5.3.2 Convenience/Grocery Stores

- 5.3.3 Food Specialty Stores

- 5.3.4 Online Retail Stores

- 5.3.5 Other Distribution Channels

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Spain

- 5.4.2.2 United Kingdom

- 5.4.2.3 Germany

- 5.4.2.4 France

- 5.4.2.5 Italy

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 South Africa

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Campbell Soup Company

- 6.3.2 General Mills Inc.

- 6.3.3 Hain Celestial Group Inc.

- 6.3.4 The Kraft Heinz Company

- 6.3.5 Unilever PLC

- 6.3.6 Amy's Kitchen Inc.

- 6.3.7 Baxters Food Group Limited

- 6.3.8 Bar Harbor Foods

- 6.3.9 BCI Foods Inc.

- 6.3.10 Sprague Foods Ltd

- 6.3.11 F Whitlock & Sons