濃縮缶スープ市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Condensed Canned Soups Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 210 Pages

- 納期

- 2~3営業日

- 商品コード

- 1797698

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

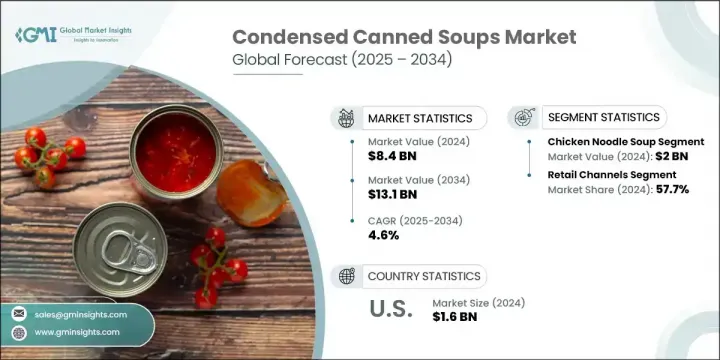

世界の濃縮缶スープ市場は2024年に84億米ドルと評価され、CAGR 4.6%で成長し、2034年には131億米ドルに達すると推定されています。

これらのスープは、手頃な価格、調理のしやすさ、長期保存安定性により、包装食品分野の定番商品であり続けています。しかし、消費者の嗜好は大きく変化しており、各ブランドは提供する商品を再考する必要に迫られています。よりクリーンなラベル、天然素材、健康志向のバリエーションを選ぶ消費者が増えており、減塩、オーガニック認証、植物性原料を強調する製品改良につながっています。食品メーカーは、利便性以上のものを提供する、栄養豊富でタンパク質を強化した濃縮スープの革新をますます進めています。

こうした製品は現在、RTE食事としてだけでなく、家庭料理レシピのベースとして多用途に使えるという位置付けにもなっています。より多くの消費者が健康志向の食事にシフトするにつれて、濃厚でカスタマイズ可能な食事成分の需要が加速しています。この動向は、急速に都市化が進む地域、特にアジア太平洋地域で顕著であり、そこでは中間層の増加とペースの速いライフスタイルが、栄養価が高く時間を節約できる食事への需要を高めています。この地域の国々は、進化する食生活に沿った便利な食品オプションへの幅広いシフトの一環として、コンデンススープ消費の力強い増加を目の当たりにしています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 84億米ドル |

| 予測金額 | 131億米ドル |

| CAGR | 4.6% |

チキンヌードルスープ分野は、2024年に20億米ドルを生み出しました。その他の人気品種には、トマトベース、マッシュルームクリーム、チキンクリームなどのスープがあり、これらは単体の食事としても、より幅広い食事作りの材料としても信頼できることが証明されています。体に良いものへの関心の高まりも、野菜や牛肉をベースにしたスープの成長を後押ししています。現代の消費者の期待に応えるため、各ブランドは従来の処方を見直し、オーガニック、アレルゲンフレンドリー、減塩レシピを導入し、風味や食感を損なうことなく健康志向の消費者への訴求を拡大しています。

小売店セグメントは2024年に57.7%のシェアを占めました。スーパーマーケット、ハイパーマーケット、近所の食料品店が依然として支配的な流通チャネルであり、消費者に様々なブランド、価格、味へのアクセスを提供しています。これらの店舗は、目立つ商品の配置、季節的なプロモーション、強力なプライベートブランド競争などの恩恵を受け、購買行動に影響を与え、このチャネルは主流購買者にとって非常に重要な位置を占めています。

北米の濃縮缶スープ市場は2024年に16億米ドルを創出したが、これは缶入りスープに対する文化的な親しみが強いことが要因です。食習慣の変化と健康志向の高まりにより、米国市場はクリーンラベル、オーガニック、植物性スープへの強い意欲を示しています。高度な食品加工と技術への投資とともに、確立された小売ネットワークにより、米国企業は新たな動向に迅速に対応することができ、米国はこの分野における技術革新の最前線にあり続けています。

濃縮缶スープの世界市場に貢献している主要企業は、Nestle S.A.、Amy's Kitchen Inc.、BCI Foods Inc.、The Kraft Heinz Company、Unilever(Knorr)、Campbell Soup Company、General Mills Inc.、ConAgra Brands Inc.、Baxters Food Group、Vanee Foods Companyなどです。濃縮缶スープ市場の主要ブランドは、減塩、オーガニック、グルテンフリー、植物由来の品種を導入するなど、改良による製品の多様化を優先しています。多くの企業が持続可能なパッケージングに投資し、進化する消費者の嗜好に対応するために風味プロファイルを強化しています。イノベーションは、スーパーフード、植物性タンパク質、アレルゲンフレンドリーな原材料を統合する研究開発によっても促進されています。さらに、各ブランドはサプライチェーンを最適化し、棚の視認性を高めるために小売店との提携を拡大しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 市場機会

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 製品タイプ別の動向

- 流通チャネルの動向

- 包装形態の動向

- 地域別

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)

(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- 濃縮スープの種類

- チキンヌードルスープ

- トマトスープ

- クリームマッシュルームスープ

- チキンクリームスープ

- 野菜スープ

- 牛肉ベースのスープ

- クリームベースの特製スープ

第6章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 小売チャネル

- スーパーマーケットとハイパーマーケット

- コンビニエンスストア

- ディスカウント小売業者

- 専門食品店

- オンライン小売とeコマース

- 食品サービスチャネル

- レストランとクイックサービス

- 施設内フードサービス

- ヘルスケアおよび教育施設

- 消費者直販チャネル

第7章 市場推計・予測:包装形態別、2021年~2034年

- 主要動向

- 従来の金属缶

- 標準サイズの缶(10.5~11オンス)

- ファミリーサイズの缶(18~23オンス)

- 業務用サイズの缶

- 代替パッケージ形式

- フレキシブルパウチとスタンドアップパウチ

- アセプティックカートンとテトラパック

- 電子レンジ対応容器

- シングルサーブカップとボウル

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ地域

第9章 企業プロファイル

- Campbell Soup Company

- General Mills Inc.(Progresso)

- The Kraft Heinz Company

- Nestle S.A.

- Unilever(Knorr)

- ConAgra Brands Inc.

- Baxters Food Group

- BCI Foods Inc.

- Vanee Foods Company

- Amy’s Kitchen Inc

目次

The Global Condensed Canned Soups Market was valued at USD 8.4 billion in 2024 and is estimated to grow at a CAGR of 4.6% to reach USD 13.1 billion by 2034. These soups remain a staple in the packaged food space due to their affordability, ease of preparation, and extended shelf stability. However, consumer preferences have evolved significantly, pushing brands to reimagine their offerings. A growing number of consumers are opting for cleaner labels, natural ingredients, and health-focused variants, leading to product reformulations that emphasize low-sodium content, organic certification, and plant-based ingredients. Food manufacturers are increasingly innovating with nutrient-rich, protein-enhanced condensed soups that offer more than just convenience.

These products are now positioned not only as ready-to-eat meals but also as versatile bases for home-cooked recipes. As more consumers shift toward health-conscious eating, the demand for enriched, customizable meal components has accelerated. This trend is particularly prominent in rapidly urbanizing areas, especially across the Asia-Pacific region, where a growing middle class and fast-paced lifestyles are fueling increased demand for nutritious, time-saving meals. Countries in the region are witnessing a strong uptake in condensed soup consumption as part of the broader shift toward convenient food options that align with evolving dietary habits.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.4 Billion |

| Forecast Value | $13.1 Billion |

| CAGR | 4.6% |

The chicken noodle soup segment generated USD 2 billion in 2024. Other popular varieties include tomato-based, cream of mushroom, and cream of chicken soups, which have proven to be reliable both as standalone meals and as ingredients in broader meal preparation. Rising interest in better-for-you options is also driving growth in vegetable and beef-based soups, while plant-forward and high-protein selections are gaining traction. To align with modern consumer expectations, brands are revisiting traditional formulations to introduce organic, allergen-friendly, and reduced-sodium recipes, expanding their appeal to health-conscious audiences without compromising flavor or texture.

The retail outlets segment held a 57.7% share in 2024. Supermarkets, hypermarkets, and neighborhood grocery stores remain the dominant distribution channels, offering consumers access to various brands, prices, and flavors. These stores benefit from prominent product placement, seasonal promotions, and strong private-label competition, which influence purchasing behavior and keep this channel highly relevant for mainstream buyers.

North American Condensed Canned Soups Market generated USD 1.6 billion in 2024, driven by strong cultural familiarity with canned soups. With changing eating habits and increasing health awareness, the U.S. market shows a solid appetite for clean-label, organic, and plant-based soups. A well-established retail network, along with investments in advanced food processing and technology, allows American companies to respond quickly to emerging trends, keeping the U.S. at the forefront of innovation in this sector.

Key players contributing to the Global Condensed Canned Soups Market include Nestle S.A., Amy's Kitchen Inc., BCI Foods Inc., The Kraft Heinz Company, Unilever (Knorr), Campbell Soup Company, General Mills Inc., ConAgra Brands Inc., Baxters Food Group, and Vanee Foods Company. Leading brands in the condensed canned soups market are prioritizing product diversification through reformulation, introducing low-sodium, organic, gluten-free, and plant-based varieties. Many companies are investing in sustainable packaging and enhancing flavor profiles to meet evolving consumer preferences. Innovation is also fueled by R&D to integrate superfoods, plant proteins, and allergen-friendly ingredients. In addition, brands are optimizing supply chains and expanding retail partnerships for better shelf visibility.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Product type trends

- 2.2.2 Distribution channel trends

- 2.2.3 Packaging format trends

- 2.2.4 Regional

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By product type trends

- 3.8.2 By distribution channel trends

- 3.8.3 By packaging format trends

- 3.8.4 By region

- 3.9 Future market trends

- 3.10 Technology and Innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Patent Landscape

- 3.12 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only)

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021-2034 (USD Billion) (Units)

- 5.1 Key trends

- 5.2 Condensed soup varieties

- 5.2.1 Chicken noodle soup

- 5.2.2 Tomato soup

- 5.2.3 Cream of mushroom soup

- 5.2.4 Cream of chicken soup

- 5.2.5 Vegetable soup

- 5.2.6 Beef-based soups

- 5.2.7 Cream-based specialty soups

Chapter 6 Market Estimates and Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Units)

- 6.1 Key trends

- 6.2 Retail channels

- 6.2.1 Supermarkets and hypermarkets

- 6.2.2 Convenience stores

- 6.2.3 Discount retailers

- 6.2.4 Specialty food stores

- 6.2.5 Online retail and e-commerce

- 6.3 Foodservice channels

- 6.3.1 Restaurants and quick service

- 6.3.2 Institutional foodservice

- 6.3.3 Healthcare and educational facilities

- 6.4 Direct-to-consumer channels

Chapter 7 Market Estimates and Forecast, By Packaging Format, 2021-2034 (USD Billion) (Units)

- 7.1 Key trends

- 7.2 Traditional metal cans

- 7.2.1 Standard size cans (10.5-11 oz)

- 7.2.2 Family size cans (18-23 oz)

- 7.2.3 Institutional size cans

- 7.3 Alternative packaging formats

- 7.3.1 Flexible pouches and stand-up pouches

- 7.3.2 Aseptic cartons and tetra packs

- 7.3.3 Microwaveable containers

- 7.3.4 Single-serve cups and bowls

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Campbell Soup Company

- 9.2 General Mills Inc. (Progresso)

- 9.3 The Kraft Heinz Company

- 9.4 Nestle S.A.

- 9.5 Unilever (Knorr)

- 9.6 ConAgra Brands Inc.

- 9.7 Baxters Food Group

- 9.8 BCI Foods Inc.

- 9.9 Vanee Foods Company

- 9.10 Amy’s Kitchen Inc

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 210 Pages

- 納期

- 2~3営業日