|

市場調査レポート

商品コード

1851236

植物油:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Vegetable Oil - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 植物油:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年07月21日

発行: Mordor Intelligence

ページ情報: 英文 140 Pages

納期: 2~3営業日

|

概要

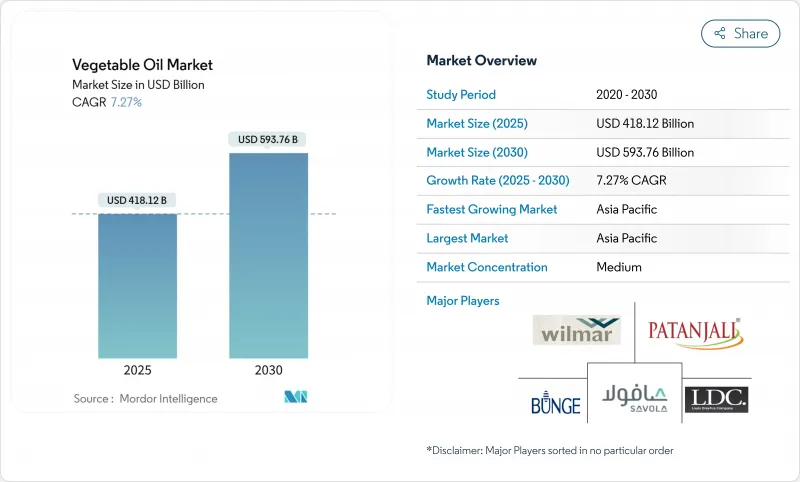

植物油市場の2025年の市場規模は4,181億2,000万米ドルで、CAGR 7.27%で推移し、2030年には5,937億6,000万米ドルに達すると予測されています。

人口増加、食品加工の拡大、バイオベースの産業用途の台頭により、需要は堅調に推移し、主要な油種で数量増加が見込まれます。持続可能性目標が原料調達の形を変え、企業に認証サプライ・チェーンの採用や土地効率の高い作物への投資を促しています。心臓に優しく、クリーンラベルの製品に対する消費者の関心は、ヒマワリ、オリーブ、その他のプレミアムオイルへの切り替えを加速させています。圧搾、精製、包装を一貫して行う生産者は、規模の大きさを活かして価格変動に対処し、利幅を確保しており、この優位性が植物油市場における継続的な統合を促しています。

世界の植物油市場の動向と洞察

健康志向の高まりにより、オリーブ油やヒマワリ油など、より健康的な油への嗜好がシフト

消費者の健康意識の高まりが、植物油市場におけるオリーブ油やヒマワリ油など、より健康的な油の需要を促進しています。例えば、米国農務省(USDA)は、心臓の健康をサポートする一価不飽和脂肪を多く含むオリーブ油の栄養的利点を強調しています。同様に、欧州食品安全機関(EFSA)は、抗酸化物質として働くビタミンEを豊富に含むヒマワリ油を推奨しています。世界保健機関(WHO)によれば、飽和脂肪酸をオリーブ油やひまわり油に含まれるような不飽和脂肪酸に置き換えることで、心血管疾患のリスクを減らすことができるといいます。さらに、米国農務省(USDA)による「マイプレート」ガイドラインのような、健康的な食生活を推進する政府の取り組みも、より健康的な食用油の使用を奨励しています。こうした支持は、消費者の意識の高まりと相まって、購買決定に大きな影響を与え、より健康的な代替品へと嗜好をシフトさせています。

食品加工とファーストフード産業の拡大が油の消費を押し上げる

食品加工およびファーストフード産業の成長は、植物油市場の重要な促進要因です。例えば米国農務省(USDA)によると、植物油の世界消費量は2023/24年に約2億1,841万トンに達し、食品メーカーやクイックサービス・レストランからの需要増が牽引しています。特に新興経済国での加工食品やコンビニエンス・フードの人気の高まりが、この需要にさらに拍車をかけています。さらに、インドの食品加工部門に対する生産連動奨励金(PLI)制度など、食品加工を促進する政府の取り組みが植物油の需要をさらに押し上げています。例えば、PLIスキームは、財政的インセンティブを提供することで食品加工産業の競争力を強化することを目的としており、製造に使用される植物油の消費を間接的に増加させています。同様に米国では、食品安全近代化法(FSMA)が食品加工施設への投資を促し、植物油の利用率向上につながりました。こうした動きは、フライ、ベーキング、その他の食品調理工程に不可欠な原料である植物油が、これらの産業で高まる消費ニーズを満たす上で重要な役割を担っていることを明確に示しています。

合成油脂や代替油脂との競合が需要に影響

市場は、合成油脂や代替油脂との競争激化による大きな抑制要因に直面しています。高度な技術によって開発されることが多いこれらの代替油脂は、植物油と同様の機能性と利点を提供するため、食品、化粧品、バイオ燃料を含む様々な産業にとって魅力的です。さらに、合成油脂はしばしば費用対効果が高く持続可能な選択肢として市場に出回り、競争をさらに激化させています。革新的で環境に優しい製品に対する消費者の嗜好の高まりも、代替油脂へのシフトに寄与しています。この動向は植物油市場の成長可能性に課題を投げかけており、メーカーは市場シェアを維持しながらこうした競合圧力に対処しなければならないです。

セグメント分析

パーム油は土地利用効率が高く、小売・外食産業全体の消費に適していることを反映して、2024年の植物油市場に28.56%寄与しています。インドネシアとマレーシアの主要生産者は、農地管理と工場の近代化を通じて安定した生産量を提供しているが、バイヤーは持続可能な認証量を求めるようになっています。森林破壊をめぐる継続的な議論がトレーサビリティ要件の強化に拍車をかけているが、コスト競争力のある収量により輸出は堅調を維持しています。ヒマワリ油は、東欧の作柄回復に支えられ、2025年から2030年にかけて最も急速にCAGR 7.27%を記録します。大豆油は、破砕マージンと飼料用の高タンパク質ミール需要との連関に支えられ、南北アメリカで強い存在感を維持しています。オリーブ油とココナッツ油は、それぞれプレミアムとニッチのニーズに対応し、植物油市場に多様性をもたらしています。

パーム由来油の植物油市場規模は、間接的な土地利用の変化を警戒する市場での採用の遅れを相殺し、一部のアジア諸国でバイオディーゼル義務化が拡大するにつれて着実に成長すると予測されます。ヒマワリ油のシェア拡大は、気候の安定と黒海回廊の物流再開にかかっています。大豆油の数量は、再生可能ディーゼル燃料の生産能力が急速に拡大している米国のバイオ燃料混合割当量と密接に関連しています。高オレイン酸菜種を含むスペシャリティオイルは、乳児用栄養剤やベーカリー用ショートニングでプレミアム価格が設定されており、機能性特性がサブセグメントのシェアをいかに獲得できるかを示しています。

2024年の植物油市場の93.52%を占める在来型油は、確立された供給ネットワーク、1ヘクタール当たりの高生産量、および大衆市場向け食品カテゴリーにおける価格敏感性によって支えられています。統合型アグリビジネスは、物流を合理化する複数の種子複合体を運営し、単価を引き下げています。しかし、森林破壊規制の強化や顧客監査によってコンプライアンス支出が増加し、精製業者をトレーサブル原料プログラムに向かわせる。オーガニック・セグメントは、現在の生産量のごく一部に過ぎないが、2030年までCAGR 9.10%で拡大し、より広範な植物油市場規模を上回ると予測されます。転換助成金と割高な小売マージンが生産者の関心を高めているが、3年間の移行期間があるため、作付面積の急速な拡大には制約があります。

需要が持続することで、加工業者は、有機大豆油で加工されたコールドプレスひまわり、エクストラバージンココナッツ、牧草飼育ギーの代用品などの有機製品ラインで、トン当たりより高いマージンを獲得することができます。都市部の消費者は、オーガニックのラベルを、農薬の使用量削減や土壌の健康に役立つものとみなし、ブランド・ロイヤリティを高めています。供給逼迫が在庫配給につながることもあり、年末年始のピーク時にはプレミアムの差が拡大します。これと並行して、従来のサプライヤーは、完全な認証を必要としない環境意識の高いバイヤーを引き留めるため、再生農業プログラムを試験的に導入しています。

地域分析

2024年には、アジア太平洋地域が植物油市場で48.7%の圧倒的シェアを占め、CAGR 8.96%(2025~2030年)という驚異的な地域最高の成長率を誇る。この勢いは、企業が同地域の成長ポテンシャルを活用し続けることで、投資と拡大の自己強化サイクルを促進します。2023年、世界有数のパーム油生産・輸出国であるインドネシアのアブラヤシ生産量は4,708万トンに達すると農業省は予測しています。インドと中国は、それぞれ大豆油とピーナッツ油の主要生産国として際立っており、国内外の需要に対応しています。この地域の力強い成長の原動力となっているのは、急増する人口、可処分所得の増加、バイオ燃料生産や化粧品など、単なる食品加工にとどまらない産業用途の急増です。

欧州の情勢は、成熟した消費習慣と、国内生産と輸入の両方を管理する厳しい規制によって形作られています。特にマーガリンの消費動向は欧州がトップであり、これは主要原料として植物油に大きく依存する食品加工部門が大きく後押ししています。トランス脂肪酸の段階的廃止に向けた取り組みは、公衆衛生上の取り組みやより健康的な代替品を求める消費者の嗜好に合致し、この市場の成長をさらに後押ししています。欧州では持続可能性の問題が大きな影響力を持っており、欧州森林破壊規制などの規制が輸入油のサプライチェーン慣行の再評価を促しています。これらの規制は、トレーサビリティの確保と環境基準の遵守を目的としており、市場力学を再構築しています。

南米は、大豆生産における農業の強みを生かし、ブラジルとアルゼンチンが主要な輸出国として台頭し、世界の植物油分野で重要な地位を確保しています。世界のバイヤーが環境に配慮した調達を求める中、持続可能性への懸念がますますこの地域の生産状況を形作っています。大手アグリビジネス企業は現在、こうした期待に応えるため、特にブラジルのセラード地域で生産される森林破壊のない大豆を優先的に調達しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 健康志向の高まりにより、オリーブ油やひまわり油のようなヘルシー志向にシフト

- 食品加工とファーストフード産業の拡大が油消費を押し上げる

- 有機・非遺伝子組み換え油への需要の高まりが植物油消費を促進する

- 都市人口の増加により、消費ニーズの高まりから食用油の需要が高まる

- 植物油の使用を支援する政府の政策が市場の成長を促進する

- バイオ燃料産業の拡大が市場成長を促進する

- 市場抑制要因

- 合成・代替油脂との競合が需要に影響

- 原料価格の変動が市場の安定に影響

- トランス脂肪酸と表示に関する政府の厳しい規制は、コンプライアンス・コストを増加させる。

- 市場成長を阻む不純物の懸念

- バリューチェーン分析

- 規制の見通し

- テクノロジーの見通し

- ポーターのファイブフォース

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- タイプ別

- パーム油

- 大豆油

- 菜種油

- ひまわり油

- ピーナッツオイル

- ココナッツオイル

- オリーブオイル

- その他のタイプ

- 由来別

- 従来型

- オーガニック

- パッケージング別

- ボトル

- パウチ

- ジャー

- 缶

- その他

- 流通チャネル別

- HoReCa/フードサービス

- 小売り

- スーパーマーケット/ハイパーマーケット

- コンビニエンスストア/食料品店

- オンライン小売店

- その他流通チャネル

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 欧州

- ドイツ

- フランス

- 英国

- スペイン

- オランダ

- イタリア

- スウェーデン

- ポーランド

- ベルギー

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ベトナム

- インドネシア

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- チリ

- ペルー

- その他南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- ナイジェリア

- エジプト

- モロッコ

- トルコ

- その他中東・アフリカ地域

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的な動き(M&A、JV、能力拡張)

- Market Positioning Analysis

- 企業プロファイル

- The Savola Group

- Bunge Limited

- Patanjali Ayurveda Limited

- Louis Dreyfus Company B.V.

- Wilmar International Ltd.

- IFFCO Group

- Sime Darby Plantation Berhad

- Fuji Oil Holdings Inc.

- Marico Ltd.

- PT Astra Agro Lestari Tbk

- The Nisshin Oillio Group, Ltd.

- Pompeian

- KTC

- Ottogi Co., Ltd.

- Bhushan Oils & Fats Pvt. Ltd.

- Agro Tech Foods Limited

- Avril Group

- Golden Agri-Resources

- Kuala Lumpur Kepong Berhad

- PT Indofood Sukses Makmur Tbk