|

市場調査レポート

商品コード

1850094

農業用界面活性剤:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Agricultural Surfactant - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 農業用界面活性剤:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月25日

発行: Mordor Intelligence

ページ情報: 英文 144 Pages

納期: 2~3営業日

|

概要

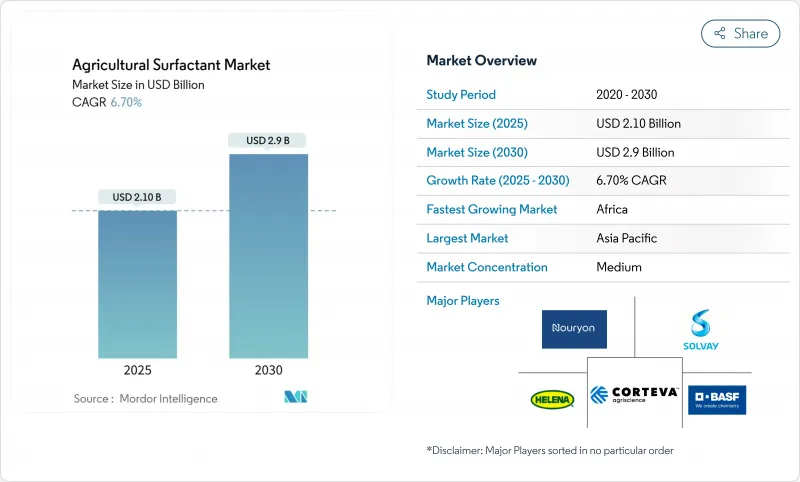

農業用界面活性剤市場は、2025年に21億米ドルと評価され、予測期間中にCAGR 6.7%で成長し、2030年には29億米ドルに達すると予測されています。

市場成長の原動力となっているのは、自律型ドローンや静電噴霧器などの精密農業機器の導入が増加していることで、液滴サイズを最適化し、ドリフトを低減し、圃場での散布効率を向上させるために、特定の界面活性剤処方が必要とされています。業界は合成化合物から両性および有機シリコーン製剤への移行を進めており、特に微生物の有効性を維持し吸収を高めるために界面活性剤を必要とする生物学的作物保護製品の拡大がその理由となっています。EUのFarm-to-Forkイニシアチブは、2030年までに合成農薬の使用量を50%削減することを目標としており、低用量適用のためのナノ界面活性剤技術の研究開発を推進しています。市場が細分化された構造であるため、専門企業が地域特化型や作物特化型のソリューションを通じて市場シェアを獲得する機会があります。しかし、原料価格の上昇と残留規制の強化が課題となっており、持続可能で経済的に実行可能な代替物質の開発が重要視されています。

世界の農業用界面活性剤市場の動向と洞察

農薬需要の増加による作物収量の増加

農業用界面活性剤は、農薬の送達効率を高めることで農作物の収量増加をサポートし、食糧安全保障と一人当たり耕地面積の減少という課題に対処します。インドでは、多機能湿潤剤が農薬散布の効果を維持しながら散布量を15~20%削減することが実地試験で実証されています。ブラジルのバイオ投入物市場は10億米ドルと評価されており、微生物剤とメチル化種子油を組み合わせて根域への浸透性を高めています。ビオネマのソイルジェットBSP100の圃場試験では、最適化されたアジュバント製剤によって生物学的効果が30%向上することが実証されています。天候に関連した病害虫の課題がますます蔓延していることから、小規模な農業経営も大規模な農業経営も、費用対効果の高い作物保護ソリューションとして界面活性剤を採用するようになっています。

精密農業の採用が界面活性剤の使用率を上げる

農業用ドローンによる散布は、2024年中にカンザス州で1,030万エーカー以上をカバーし、プロペラの乱流の中でも液滴サイズを一定に保つ特殊な両性界面活性剤を利用しています。葉の裏に液滴を付着させることができる静電散布システムは、水の消費量を60%削減したが、特定の導電率バランスの添加剤が必要でした。ブラジルのゴイアス州では、可変レート散布で大豆畑の100%をカバーしており、農学者はリアルタイムでタンクミックスを調整する際に有効成分の安定性を維持するため、pH安定製剤を選択しています。エボニックのような企業は、ドローンスプレーシステム用に特別に設計されたブレイクツルーMSO MAX 522のような特殊製品を開発しています。こうした用途に特化した要件が、農業用界面活性剤市場の着実な成長を促し、プレミアム価格を支えています。

バイオベース原料の高い生産コスト

発酵または植物油を原料とするバイオベースの生産ルートは、炭素クレジットを考慮した後でも、石油化学の代替品より15~30%割高です。ダウが最近、キラント中間体の価格をポンド当たり0.10米ドル引き上げたことは、誘導体のサプライチェーンに影響を及ぼすインフレ圧力を示しています。農地の70%を零細農家が所有する新興市場では、政府の補助金なしには、価格に敏感な農家の導入が遅れる可能性があります。酵素触媒の効率改善、反応器容量の拡大、製品別の利用によってコスト・パリティを達成できる可能性はあるが、現在の2年間のコスト面での不利が、農業用界面活性剤における再生可能グレードの市場シェア拡大を制約しています。

セグメント分析

非イオン性分子は、中性電荷、幅広いpH耐性、グリホサートやフェノキシ系除草剤との適合性が実証されていることから、2024年の売上高の38%を占めました。これらの界面活性剤は、親水性ー親油性バランス(HLB)値が12~15であり、様々な溶剤の組み合わせを乳化するのに有効です。非イオン界面活性剤が市場の優位性を維持する一方で、両性界面活性剤は8.2%の成長を遂げており、陰イオン条件下で劣化する微生物製剤での採用が増加しています。欧州のリンゴ園での実地試験では、両性界面活性剤が散布温度範囲を広げながら銅の散布量を20%削減することが実証されました。

両性界面活性剤のメーカーはベタインやイミダゾリン構造を利用し、低発泡性と生分解性を提供し、スーパーマーケットのコンプライアンス監査における残留物ゼロの要件を満たしています。両性界面活性剤の農業用界面活性剤市場は、2030年までに倍増すると予想され、ドローンで操作するブドウ園用途での初期採用が見込まれます。非イオン性のサブカテゴリーである有機シリコーンは、表面張力を20 mN/m以下に低下させることで性能を向上させ、5秒以内に気孔への浸透を可能にします。プレミアム価格であるにもかかわらず、これらの特殊なシロキサンは、高い散布量では植物毒性の可能性があるため、選択的に使用されています。

除草剤は2024年の農業用界面活性剤市場収益の40.2%を占めました。世界的な抵抗性管理戦略は、葉のクチクラに浸透する効果的な湿潤剤を必要とする接触型および浸透型の雑草防除ソリューションに引き続き依存しているためです。米国中西部での圃場試験では、サフルフェナシルとメチル化種子油を組み合わせたタンク混合剤でベルベットリーフを95%防除できたことが実証され、技術の進歩が示されました。市場の成長を支えているのは、新しい有効成分のラベルで、最適な性能を確保するためにアジュバントの要件が頻繁に指定されていることです。

殺菌剤分野は、市場規模は小さいもの、暖かい季節による病原菌のライフサイクルの延長により、CAGR 7.4%で成長しています。ブラジルの調査では、有機シリコーン湿潤剤は従来の非イオン性界面活性剤と比較して、大豆のさび病の重症度を30%低減することが示されました。両性キャリアを利用した新しいナノ銅製剤はEUの規制審査を受けており、金属残留物の減少という利点が期待できます。殺虫剤セグメントは、消泡性と浸透性を兼ね備えた特殊な界面活性剤を必要とするナノカプセル化ピレスロイドで構成されています。

地域分析

アジア太平洋地域は2024年の市場収益の32%を占め、これは中国の広範な稲作とトウモロコシ栽培、インドの拡大する大豆と綿花の輪作慣行が牽引しています。中国の調査では、静電ドローン散布が92.1%の害虫駆除効果を達成し、水の使用量を90%削減したことが実証され、電荷適合アジュバントの需要が高まっています。インドでは農薬市場が10.3%成長し、グジャラート州やマディヤ・プラデーシュ州で普及している硬水条件下でグリホサートの安定性を維持する湿潤剤のニーズが高まっています。日本では、政府が支援するスマート農業構想により、ロボット農機のセンサー干渉を防ぐ超低発泡シリコーンの使用が増加しています。

アフリカの市場規模は小さいが、ナイジェリア、ケニア、南アフリカが土壌検査と可変施用マッピングを通じて精密農業能力を拡大するにつれて、CAGRは7.9%になると予測されます。南アフリカの柑橘類輸出では、EUの残留農薬基準に準拠するため、耐風性とパックハウス加工時の容易な除去を両立するアジュバントが必要とされています。ナイジェリアの温室開発では、生物学的殺虫剤と連動するpH緩衝散布剤が必要とされ、地域的な製造事業の機会を創出しています。

北米では、遺伝子組み換え作物や厳格なドリフト防止対策を通じて、プレミアム市場の地位を維持しており、米国の農家は風洞試験済みのドリフト低減製品を利用しています。カナダのキャノーラ農家は、春のバーンダウン散布にメチル化種子油を使用しており、液体界面活性剤市場の成長を支えています。欧州市場は、Farm-to-Fork政策に合わせて、バイオベースのエトキシレートや非APE製剤への移行を進めています。南米では、ブラジルの大豆産業が可変レートドローン技術を採用しており、多様な水条件に適した、すばやく溶けるアジュバントポッドを必要としています。中東市場では、灌漑システムの限られた水資源を最適化するための土壌湿潤剤が注目されています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 作物の収穫量を増やすための農薬の需要増加

- 精密農業の導入により界面活性剤の使用量が増加

- 持続可能なバイオベースの界面活性剤への注目の高まり

- 超低用量活性物質を可能にするナノ界面活性剤の革新

- 生物学的作物保護適合性要件

- 自律型ドローンと静電噴霧器の利用拡大

- 市場抑制要因

- バイオベース原材料の高生産コスト

- 化学物質残留物に関する厳格な規制

- 特殊エトキシレートの原料供給の不安定性

- ナノ製剤の植物毒性に関する懸念

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 製品タイプ別

- アニオン性

- 非イオン性

- カチオン

- 両性

- 油性界面活性剤

- 用途別

- 除草剤

- 殺虫剤

- 殺菌剤

- その他の用途

- 基質別

- 合成

- バイオベース

- 作物別用途

- 作物ベース

- 穀物

- 油糧種子

- 果物と野菜

- 非作物ベース

- 芝生と観賞用芝

- その他の作物への応用

- 作物ベース

- 形態別

- 液体

- 粉末/粒状

- 機能別

- 湿潤剤

- 分散剤

- 浸透剤/アジュバント

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東

- サウジアラビア

- アラブ首長国連邦

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- その他アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Corteva Agriscience

- BASF SE

- Evonik Industries AG

- Croda International Plc

- Solvay SA

- Nouryon

- Clariant

- Wilbur-Ellis Company LLC

- Nufarm

- Kao Corporation

- Lamberti S.p.A.

- Brandt, Inc.

- GarrCo Products, Inc.

- Bionema

- Innospec Inc.

- Stepan Company

- Loveland Products, Inc.(Nutrien)

- Norac Concepts Inc.

- Helena Agri-Enterprises, LLC