|

|

市場調査レポート

商品コード

1640547

水素コンプレッサ-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Hydrogen Compressor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 水素コンプレッサ-市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 202 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

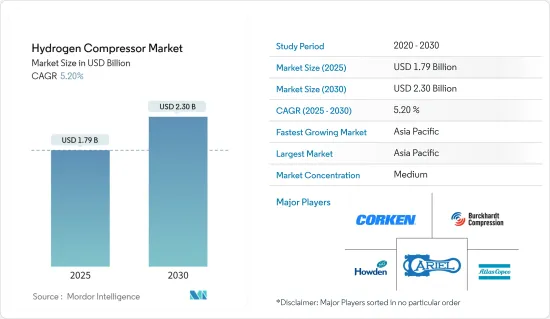

水素コンプレッサ市場規模は2025年に17億9,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは5.2%で、2030年には23億米ドルに達すると予測されます。

主要ハイライト

- 肥料や石油精製などのエンドユーザー産業からの水素需要の増加、輸送用水素パイプラインインフラの世界的展開の増加などの要因が、予測期間中の水素コンプレッサ市場を牽引すると予想されます。

- 一方、関税の上昇や貿易施策の不確実性の長期化に伴う、製造活動の急激な低下や世界の貿易の低迷による産業・経済活動の鈍化は、水素を使用する産業からの資本財の需要を減少させ、それによって調査された市場の成長を抑制すると予想されます。

- 技術の進歩や、太陽光や風力などのクリーンな供給源と組み合わせた電気分解による水素製造のための新たな供給源は、市場の成長に十分な機会を提供すると考えられます。

- 予測期間中、アジア太平洋が水素コンプレッサ市場を独占すると予想され、需要の大半は中国、インド、日本によるものです。

水素コンプレッサ市場の動向

市場を独占する油性セグメント

- オイルベースの潤滑式コンプレッサは、オイルフリーコンプレッサよりもコストが低く、耐用年数が長いです。オイル汚染の影響が非常に大きく、オイルフリーコンプレッサが必須とされる産業で使用される場合を除き、商用と産業用途に最適と考えられています。

- オイルベースのコンプレッサは、オイルフリーのコンプレッサよりも効率が高いと考えられています。オイルは冷却媒体として機能し、圧縮プロセス中にコンプレッサの熱の約80%を奪うからです。また、高圧縮比が要求される産業用途にも適しています。

- 資本支出という点では、潤滑油ベースのコンプレッサはオイルフリーコンプレッサよりも安価であると考えられ、価格差は30~40%の範囲になることが多いです。容量や産業固有の要件などの要因によっては、50%に達することさえあり、その結果、油性水素コンプレッサの需要が高まっている

- 油性コンプレッサは、オイルフリーコンプレッサよりも手頃な価格であるが、継続的なメンテナンスが必要であり、オイル漏れのリスクを排除するために使用されるフィルターやその他の部品の交換に、より大きな注意を払う必要があります。継続的な油汚染は、製品の汚染や安全性の低下、生産停止、法的問題など、深刻な結果を招く可能性があります。

- 石油ベースの水素コンプレッサは、ガラス精製、鉄鋼業、半導体製造、溶接、焼きなまし、発電所(発電機の冷却水)における金属の熱処理、航空宇宙用途、医薬品などの製造業で主に好まれています。

- 米国地質調査所によると、2023年の米国の生鉄鋼生産量は8,000万トンと推定されています。米国の鉄鋼産業の2023年の粗鋼生産額は約1,100億米ドルと推定され、2022年の1,280億米ドルから15%減少しました。工業化の進展に伴い、鉄鋼生産は今後も増加する可能性があり、その結果、石油ベースの水素コンプレッサの需要が生まれる可能性があります。

- さらに、世界鉄鋼協会によると、鉄鋼需要は2024年に1.7%増加し、2025年には1.2%増加して18億1,500万トンに達すると予想されています。したがって、鉄鋼需要の増加が今後の市場成長を牽引することになります。

- 潤滑不足は、水素コンプレッサの部品の早期摩耗を持続的に脅かすため、石油ベースの水素コンプレッサのメンテナンスコストを増加させ、その需要を制限する可能性があります。

- このような要因から、予測期間中、油性タイプが水素コンプレッサ市場を独占すると予想されます。

アジア太平洋が市場を独占する見込み

- アジア太平洋は、中国、日本、インドなどの国々で政府の施策が好意的であるため、今後数年間は燃料電池の有望な市場になると予想されます。

- 中国は、世界最大かつ最も急成長している水素コンプレッサ市場のひとつです。同国では近年、化学・石油・ガス・製造業が著しい成長を遂げています。

- 水素遠心式コンプレッサは、エチレンプラントなどの精製・石油化学産業で分解ガス圧縮や冷凍サービスに使用されています。エチレンとベンゼンの生産不足のため、中国はエチレンとベンゼンの生産能力増強に投資しています。

- さらに、コンプレッサ市場を拡大するため、複数のコンプレッサ企業がアジア諸国に投資しています。例えば、2024年4月、PDC MachinesとKirloskar Pneumatic Company Limitedは、インド全域で水素圧縮ソリューションを提供することで合意しました。この合意により、PDCはインド国内の水素市場をサポートし、KPCLの既存顧客ベースを活用することでアジアでのリーチを拡大します。これにより、同地域における水素コンプレッサ市場の重要性が高まることになります。

- 水素燃料電池車の開発と、水素燃料電池車に充電するための水素燃料ステーションの建設を目指す日本の動きは、水素コンプレッサ市場を牽引すると予想されます。

- 例えば、AIRIA(日本)によると、2023年3月現在、日本で使用されている燃料電池電気自動車は7,470台で、2015年の200台以下から増加しています。これらの車両の大半は、主に水素を燃料とする乗用車です。このことは、予測期間中、水素燃料ステーション用水素コンプレッサの需要を促進すると予想されます。

- したがって、こうした要因から、予測期間中、アジア太平洋が水素コンプレッサ市場を独占すると予想されます。

水素コンプレッサ産業概要

水素コンプレッサ市場は適度にセグメント化されています。主要企業には、Corken Inc.、Ariel Corporation、Burckhardt Compression AG、Howden Group Ltd、Atlas Copco Groupなどがあります(順不同)。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:10億米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- エンドユーザー産業からの水素需要の増加

- 輸送用水素パイプラインインフラ導入の増加

- 抑制要因

- 製造活動と世界貿易の急激な減少による産業・経済活動の鈍化

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 技術

- 単段式

- 多段式

- タイプ

- 油性

- オイルフリー

- エンドユーザー産業

- 化学

- 石油・ガス

- その他

- 市場分析:地域別2028年までの市場規模と需要予測(地域別)

- 北米

- 米国

- カナダ

- その他の北米

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- ロシア

- ノルディック

- スペイン

- その他の欧州

- アジア太平洋

- インド

- 中国

- 日本

- オーストラリア

- マレーシア

- インドネシア

- タイ

- その他のアジア太平洋

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- カタール

- アラブ首長国連邦

- ナイジェリア

- エジプト

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他の南米

- 北米

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Corken Inc.

- Ariel Corporation

- Burckhardt Compression AG

- Hydro-Pac Inc.

- Haug Kompressoren AG

- Sundyne Corp.

- Howden Group Ltd

- Indian Compressors Ltd

- Atlas Copco Group

- Ingersoll Rand Inc.

- 市場ランキング/シェア(%)分析

第7章 市場機会と今後の動向

- 水素製造の技術的進歩と新たな供給源

目次

Product Code: 54577

The Hydrogen Compressor Market size is estimated at USD 1.79 billion in 2025, and is expected to reach USD 2.30 billion by 2030, at a CAGR of 5.2% during the forecast period (2025-2030).

Key Highlights

- Factors such as the increase in demand for hydrogen from end-user industries, such as fertilizers and oil refineries, and increasing deployment of hydrogen pipeline infrastructure globally for transportation are expected to drive the hydrogen compressor market during the forecast period.

- On the other hand, the slowdown in industrial and economic activities due to a sharp decline in manufacturing activity and global trade, with higher tariffs and prolonged trade policy uncertainty, is expected to decrease the demand for capital goods from industries using hydrogen, thereby restraining the growth of the market studied.

- Nevertheless, the technological advancements and emerging sources for hydrogen production using electrolysis in combination with cleaner sources, such as solar and wind, are likely to provide ample opportunities for the market's growth.

- Asia-Pacific is expected to dominate the hydrogen compressor market during the forecast period, with the majority of the demand coming from China, India, and Japan.

Hydrogen Compressor Market Trends

Oil-based Segment Expected to Dominate the Market

- Oil-based lubricated compressors cost less and provide a longer service life than oil-free compressors. They are considered ideal for commercial and industrial applications until and unless they are used in industries where the consequences of oil contamination are considered very high and having an oil-free compressor is a must.

- Oil-based compressors are considered more efficient than oil-free compressors, as oil acts as a cooling medium, taking out approximately 80% of the compressor's heat during the compression process. They are also considered more suitable for industrial usage with requirements of a high compression ratio.

- In terms of capital outlay, lubricated oil-based compressors are often considered less expensive than oil-free compressors, with price differences often varying in the range of 30-40%. It may even reach 50%, depending upon factors such as capacity and industry-specific requirements, resulting in increased demand for oil-based hydrogen compressors.

- Although oil-based compressors are more affordable than oil-free compressors, they require continuous maintenance and greater attention to replacing filters and other components used to eliminate the risk of oil leakage. Ongoing oil contamination may result in severe consequences, such as spoiled or unsafe products, production downtime, and legal issues.

- Oil-based hydrogen compressors are mostly preferred in the manufacturing industry for glass purification, iron and steel industry, semiconductor manufacturing, welding, annealing, and heat-treating metals in power plants (coolant for generators), aerospace applications, pharmaceuticals, etc.

- According to the United States Geological Survey, in 2023, raw steel production in the United States was estimated to be 80 million metric tons. The US iron and steel industry produced raw steel in 2023 with an estimated value of about USD 110 billion, a 15% decrease from USD 128 billion in 2022. With the increasing industrialization, steel production may continue to increase, which, in turn, may create demand for oil-based hydrogen compressors.

- Furthermore, according to the World Steel Association, steel demand is expected to increase by 1.7% in 2024 and grow by 1.2% in 2025 to reach 1,815 million tonnes. Thus, the increase in demand for steel will drive the market's growth in the future.

- Insufficient lubrication persistently threatens premature wear of hydrogen compressor components, which may increase the maintenance cost of oil-based hydrogen compressors and limit their demand.

- Therefore, based on such factors, the oil-based type segment is expected to dominate the hydrogen compressor market during the forecast period.

Asia-Pacific Expected to Dominate the Market

- Asia-Pacific is expected to be a promising market for fuel cells in the coming years because of the favorable government policies in countries such as China, Japan, and India.

- China is one of the world's largest and fastest-growing hydrogen compressor markets. The country has witnessed significant growth in its chemical, oil, gas, and manufacturing sectors in recent years.

- Hydrogen centrifugal compressors are used in refining and petrochemical industries, such as ethylene plants, for cracked-gas compression and refrigeration services. Due to ethylene and benzene production shortages, China has been investing in increasing its ethylene and benzene production capacities.

- Furthermore, several compressor companies are investing in Asian countries to expand the compressor market. For instance, in April 2024, PDC Machines and Kirloskar Pneumatic Company Limited agreed to provide hydrogen compression solutions throughout India. As per the agreement, PDC will support the local Indian hydrogen market, amplifying its reach in Asia by leveraging KPCL's existing customer base. This will boost the significance of the hydrogen compressor market in the region.

- The development of hydrogen fuel cell vehicles and Japan's aim to build hydrogen fuel stations for recharging the vehicles are expected to drive the hydrogen compressor market.

- For instance, according to AIRIA (Japan), as of March 2023, 7.47 thousand fuel-cell electric vehicles were in use in Japan, increasing from less than 200 in 2015. The majority of these vehicles were primarily hydrogen-fueled passenger cars. This, in turn, is expected to drive the demand for hydrogen compressors for hydrogen fuel stations during the forecast period.

- Therefore, based on such factors, Asia-Pacific is expected to dominate the hydrogen compressor market during the forecast period.

Hydrogen Compressor Indsutry Overview

The hydrogen compressor market is moderately fragmented. Some of the major companies include (in no particular order) Corken Inc., Ariel Corporation, Burckhardt Compression AG, Howden Group Ltd, and Atlas Copco Group.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increase in Demand for Hydrogen from End-user Industries

- 4.5.1.2 Increasing Deployment of Hydrogen Pipeline Infrastructure for Transportation

- 4.5.2 Restraints

- 4.5.2.1 The Slowdown in Industrial and Economic Activities Due to a Sharp Decline in Manufacturing Activity and Global Trade

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Technology

- 5.1.1 Single-stage

- 5.1.2 Multistage

- 5.2 Type

- 5.2.1 Oil-based

- 5.2.2 Oil-free

- 5.3 End-user Industry

- 5.3.1 Chemical

- 5.3.2 Oil and Gas

- 5.3.3 Other End-user Industries

- 5.4 Geography (Regional Market Analysis {Market Size and Demand Forecast till 2028 (For Regions Only)})

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Russia

- 5.4.2.6 NORDIC

- 5.4.2.7 Spain

- 5.4.2.8 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 India

- 5.4.3.2 China

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 Malaysia

- 5.4.3.6 Indonesia

- 5.4.3.7 Thailand

- 5.4.3.8 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 Saudi Arabia

- 5.4.4.2 South Africa

- 5.4.4.3 Qatar

- 5.4.4.4 United Arab Emirates

- 5.4.4.5 Nigeria

- 5.4.4.6 Egypt

- 5.4.4.7 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Colombia

- 5.4.5.4 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Corken Inc.

- 6.3.2 Ariel Corporation

- 6.3.3 Burckhardt Compression AG

- 6.3.4 Hydro-Pac Inc.

- 6.3.5 Haug Kompressoren AG

- 6.3.6 Sundyne Corp.

- 6.3.7 Howden Group Ltd

- 6.3.8 Indian Compressors Ltd

- 6.3.9 Atlas Copco Group

- 6.3.10 Ingersoll Rand Inc.

- 6.4 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technological Advancements and Emerging Sources for Hydrogen Production