|

|

市場調査レポート

商品コード

1640559

アスファルト改質剤:市場シェア分析、産業動向と統計、成長予測(2025~2030年)Asphalt Modifiers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アスファルト改質剤:市場シェア分析、産業動向と統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

アスファルト改質剤の市場規模は2025年に46億米ドルと予測され、予測期間(2025~2030年)のCAGRは5.34%で、2030年には59億7,000万米ドルに達すると予測されています。

COVID-19は製造業に大きな影響を及ぼし、市場の成長を阻害しました。しかし、その後各産業はパンデミックから回復しました。それ以来、建設産業の着実な成長が市場を牽引しています。

主要ハイライト

- 予測期間中、市場の需要を牽引するのは、道路における交通量の増加や荷重の増加、スーパーセーブ設計仕様への対応、舗装の長寿命化、MROコストの低下などであると考えられます。

- その一方で、改質アスファルトセメントを使用するコストが高いことや、アスファルトを扱うことによる健康上のリスクが、市場の成長を鈍らせる可能性が高いです。

- HMA(ホットミックスアスファルト)の需要の増加、RAP(再生アスファルト舗装)の人気の高まり、生物再生可能な改質剤の開発、ウォームミックスアスファルト技術の改善、アスファルト(ナノクレイ)を変更するためにナノ技術を使用する研究から、市場の将来の機会が期待されています。

- アスファルトの需要が高いため、アジア太平洋が最も重要であり、今後数年間成長し続けると考えられます。

アスファルト改質剤の市場動向

舗装用途からの需要増加

- アスファルトとコンクリートの混合物は、道路、空港滑走路、誘導路、自転車専用道路などの建設に多く使われてきました。バインダー改質剤(ポリマー、エラストマー、繊維、ゴムなど)や骨材改質剤(石灰、粒状ゴム、剥離防止剤など)は、熱ひび割れ、わだち掘れ、剥離などの問題に対する耐性を高め、アスファルト舗装の性能を向上させるために使用されます。これにより、舗装が長持ちします。

- 近年、アスファルト改質剤の世界需要は、平均を上回る成長を遂げています。アスファルト改質剤の需要は、世界中で進行中の道路建設活動のレベルと直接的な相関関係を持っています。

- 米国国勢調査局によると、2022年に実施される連邦高速道路と道路建設の金額は約17億米ドルになり、前年の合計金額約14億米ドルに比べて18%増加します。道路や高速道路に投入される資金が増えれば、アスファルト改質剤の需要も増えると考えられます。

- また、ポーランド中央統計局は12月の月報で、2022年のポーランドにおけるアスファルトの総生産量は約164万トンで、前年の生産額約154万トンを約6%上回ったと発表しました。

- 欧州アスファルト舗装協会(EAPA)によると、欧州では2021年に約2億9,060万トンのホットミックスとウォームミックスアスファルトを製造しました。これは、前年の生産量より1,370万トン多いだけです。最も生産量が多かったのはドイツで、総生産量の13%以上を占め、イタリアとフランスがこれに続きました。

世界各地で建設される高速道路や道路の増加に伴い、アスファルト舗装の需要が増加し、アスファルト改質剤の需要も増加すると考えられます。

アジア太平洋が市場を独占する

- アジア太平洋は、中国、インド、日本のような国家における建設ニーズの拡大の結果として、アスファルト改質剤市場を独占しました。この地域の市場成長は、新しい空港滑走路の建設や輸送の拡大によって促進されています。

- ここ数年の不動産セクターの不安定な成長にもかかわらず、拡大する産業サービスセクターに耐えられるよう中国政府が鉄道・道路インフラを大幅に開発した結果、最近の中国建設産業は大きく成長しています。

- 中国は道路開発とメンテナンスへの投資を倍増させました。さらに、中国には現在と将来の道路・高速道路建設プロジェクトがいくつかあります。増城-仏山高速道路は中国広東省の23億7,600万米ドルのプロジェクトで、増城から天河区間までの38.4kmの高速道路を建設します。2021年第3四半期に着工し、2025年第4四半期に完成する予定です。

- 一方、インドには580万kmを超える道路があり、世界第2位の道路システムとなっています。道路交通・高速道路省は2022~23年連邦予算で1兆9,910億714万インドルピー(260億4,000万米ドル)を与えられています。

- さらに、India Brand Equity Foundationの報告によると、インド国道庁(NHAI)は2022~23年に2万5,000kmの国道を1日あたり50kmのペースで建設する意向です。また、NHAIは高速道路資産(InvIT)を収益化するため、インフラ投資信託を通じて4,000億インドルピー(57億2,000万米ドル)を調達する意向です。

- 国土交通省によると、2021年度の日本の建設用アスファルトの国内需要は約106万トン。前年度の約120万トンから減少しました。

プロジェクトの実行ペースは、今後数年間でさらに増加すると考えられます。同地域の道路・高速道路インフラ開発への投資は、予測期間中に増加すると予想されます。全体として、このような投資と開発がアジア太平洋のアスファルト改質剤市場を牽引すると予想されます。

アスファルト改質剤産業概要

アスファルト改質剤市場は部分的に統合されており、主要企業が大きなシェアを占めています。アスファルト改質剤市場の主要企業には、DuPont、BASF SE、Arkema、Nouryon、Dowなどが含まれます(順不同)。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 交通量の多さと荷重の重さ

- スーパーセーブ設計仕様への適合重視

- 舗装の長寿命化とMROコスト削減のメリット

- 抑制要因

- 改質アスファルトセメントを使用するための高い初期費用

- アスファルトに関する労働衛生上の危険性

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

- 規制施策

第5章 市場セグメンテーション(金額ベース市場規模)

- 用途

- 舗装

- 屋根

- その他

- エンドユーザー産業

- 物理的改質剤

- プラスチック

- ゴム

- その他の物理的改質剤

- 化学改質剤

- 繊維

- 接着性向上剤

- 増量剤

- 充填剤

- 酸化防止剤

- ストリップ防止剤

- その他

- 物理的改質剤

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- カタール

- その他の中東・アフリカ

- アジア太平洋

第6章 競争情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)分析**/市場ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Arkema

- ArrMaz Products, Inc.

- BASF SE

- Cargill

- Dow

- DuPont

- Engineered Additives LLC

- Evonik Industries AG

- Exxon Mobil Corporation

- Genan Holding A/S

- Honeywell International Inc.

- Kao Corporation

- Kraton Corporation

- McAsphalt Industries Limited

- Nouryon

- PQ Corporation

- Sasol

第7章 市場機会と今後の動向

- HMA(ホットミックスアスファルト)への嗜好の高まり

- 再生アスファルト舗装(RAP)の人気の高まり

- バイオ再生可能な改質剤の開発

- ウォームミックスアスファルト技術の進歩

- アスファルト改質(ナノ粘土)にナノ技術を組み込む調査

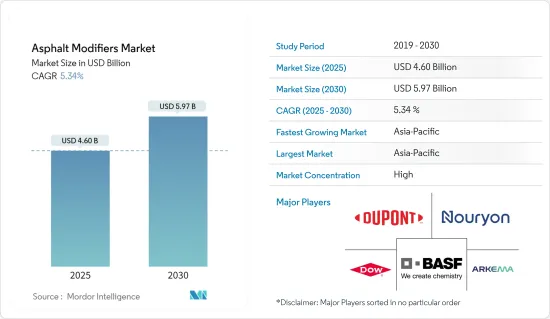

The Asphalt Modifiers Market size is estimated at USD 4.60 billion in 2025, and is expected to reach USD 5.97 billion by 2030, at a CAGR of 5.34% during the forecast period (2025-2030).

COVID-19 had a major impact on the manufacturing industry, thus hampering market growth. However, the industries have since recovered from the pandemic. Since then, the construction industry's steady growth has been the market's main driver.

Key Highlights

- During the forecast period, the demand for the market is likely to be driven by things like more traffic and heavier loads on roads, a focus on meeting super-save design specifications, longer pavement life, and lower MRO costs.

- On the other hand, the high cost of using modified asphalt cement and the health risks of working with asphalt are likely to slow the growth of the market.

- Future opportunities for the market are expected to come from the growing demand for HMA (Hot Mix Asphalt), the growing popularity of RAP (Reclaimed Asphalt Pavement), the development of bio-renewable modifiers, the improvement of warm mix asphalt technologies, and research into using nanotechnology to change asphalt (Nano-Clay).

- Due to the high demand for asphalt, the Asia-Pacific region has been the most important and will continue to grow over the next few years.

Asphalt Modifiers Market Trends

Increasing Demand from Paving Application

- Mixtures of asphalt and concrete have been used a lot to build roads, airport runways, taxiways, and bike lanes, among other things. Binder modifiers (like polymers, elastomers, fibers, and rubber) and aggregate modifiers (like lime, granulated rubber, and anti-strip agents) are used to improve the performance of asphalt pavements by making them more resistant to problems like thermal cracking, rutting, stripping, and so on. This makes the pavement last longer.

- In recent years, the global demand for asphalt modifiers has been witnessing above-average growth. The demand for asphalt modifiers has a direct correlation with the level of ongoing road construction activities around the world.

- According to the US Census Bureau, the value of federal highway and street construction put in place in the United States in 2022 will be around USD 1.7 billion, representing an increase of 18% over the previous year's total value of approximately USD 1.4 billion. With more money going into roads and highways, there would be more demand for asphalt modifiers, which are an important part of the business.

- The Central Statistical Office of Poland in its December monthly report also stated that the total production of asphalt in Poland in 2022 was about 1.64 million metric tons, about 6% more than the previous year's production value of about 1.54 million metric tons.

- According to the European Asphalt Pavement Association (EAPA), Europe made about 290.6 million metric tons of hot and warm mix asphalt in 2021. This is just 13.7 million metric tons more than what was made the year before. Germany produced the most, making up over 13% of the total output, followed by Italy and France.

With more highways and roads being built in different parts of the world, this is likely to increase the demand for asphalt pavements, which will in turn increase the demand for asphalt modifiers.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region dominated the asphalt modifier market as a result of the expanding need for construction in nations like China, India, and Japan. Market growth in the area is being fueled by the construction of new airport runways and transportation expansions.

- The significant development of rail and road infrastructure by the Chinese government to withstand the expanding industrial and service sectors has resulted in significant growth of the Chinese construction industry in recent years, despite the volatile growth in the real estate sector in the last couple of years.

- China has doubled its investment in road development and maintenance. Furthermore, the country has several present and prospective road and highway construction projects. The Zengcheng-Foshan Expressway is a USD 2,376 million project in Guangdong, China, that involves the construction of a 38.4-km highway from Zengcheng to Tianhe Section. Construction began in the third quarter of 2021 and is scheduled to finish in the fourth quarter of 2025.

- India, on the other hand, has over 5.8 million kilometers of roads, which makes it the second-largest road system in the world.The Ministry of Road Transport and Highways has been given INR 199,107.71 crore (USD 26.04 billion) in the Union Budget 2022-23.

- Furthermore, the India Brand Equity Foundation reports that the National Highway Authority of India (NHAI) intends to build 25,000 kilometers of national highways in 2022-23 at a rate of 50 kilometers per day. In addition, NHAI intends to raise INR 40,000 crore (USD 5.72 billion) through an infrastructure investment trust to monetize its motorway assets (InvIT).

- According to the Ministry of Land, Infrastructure, Transport, and Tourism (MLIT), Japan's domestic demand for asphalt for construction in fiscal year 2021 was about 1.06 million metric tons. This was down from about 1.2 million tons in the prior fiscal year.

The pace of project execution is likely to increase further in the coming years. Investments in the development of roads and highway infrastructure in the region are anticipated to rise during the forecast period. Overall, such investments and development are expected to drive the asphalt modifiers market in the Asia-Pacific region.

Asphalt Modifiers Industry Overview

The asphalt modifiers market is partially consolidated, with the top players having a significant share of the market. Key players in the asphalt modifiers market include (not in any particular order) DuPont, BASF SE, Arkema, Nouryon, and Dow, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 High Traffic Volume and Heavier Loads

- 4.1.2 Emphasis on Meeting Super-save Design Specifications

- 4.1.3 Increased Pavement Work-life and Reduced MRO Cost Advantages

- 4.2 Restraints

- 4.2.1 High Initial Cost for Using Modified Asphalt Cement

- 4.2.2 Occupational Health Hazards Regarding Asphalt

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Regulatory Policy

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Application

- 5.1.1 Paving

- 5.1.2 Roofing

- 5.1.3 Other Applications

- 5.2 End-user Industry

- 5.2.1 Physical Modifiers

- 5.2.1.1 Plastics

- 5.2.1.2 Rubbers

- 5.2.1.3 Other Physical Modifiers

- 5.2.2 Chemical Modifiers

- 5.2.3 Fibers

- 5.2.4 Adhesion Improvers

- 5.2.5 Extenders

- 5.2.6 Fillers

- 5.2.7 Antioxidants

- 5.2.8 Anti-strip Modifiers

- 5.2.9 Other End-user Industries

- 5.2.1 Physical Modifiers

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Australia

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East & Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Qatar

- 5.3.5.4 Rest of Middle East & Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) Analysis**/Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Arkema

- 6.4.2 ArrMaz Products, Inc.

- 6.4.3 BASF SE

- 6.4.4 Cargill

- 6.4.5 Dow

- 6.4.6 DuPont

- 6.4.7 Engineered Additives LLC

- 6.4.8 Evonik Industries AG

- 6.4.9 Exxon Mobil Corporation

- 6.4.10 Genan Holding A/S

- 6.4.11 Honeywell International Inc.

- 6.4.12 Kao Corporation

- 6.4.13 Kraton Corporation

- 6.4.14 McAsphalt Industries Limited

- 6.4.15 Nouryon

- 6.4.16 PQ Corporation

- 6.4.17 Sasol

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Preference for HMA (Hot Mix Asphalt)

- 7.2 Growing Popularity of Reclaimed Asphalt Pavement (RAP)

- 7.3 Development of Bio-renewable Modifiers

- 7.4 Advancement in Warm Mix Asphalt Technologies

- 7.5 Research for Incorporating Nanotechnology in Asphalt Modification (Nano-clay)