|

市場調査レポート

商品コード

1687164

PVC安定剤:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)PVC Stabilizers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| PVC安定剤:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 190 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

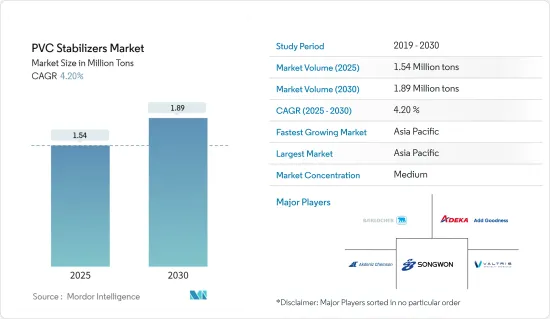

PVC安定剤の市場規模は2025年に154万トンと推定され、予測期間(2025-2030年)のCAGRは4.2%で、2030年には189万トンに達すると予測されています。

COVID-19の流行はPVC安定剤市場に悪影響を与えました。世界の操業停止と厳しい政府規制により、ほとんどの生産拠点が操業停止となり、壊滅的な後退を余儀なくされました。それでも、市場は2021年に回復し、今後数年間で大幅に上昇すると予想されます。

主なハイライト

- 短期的には、PVCパイプ、チューブ、継手用の安定剤需要の増加と自動車産業での使用の増加がPVC安定剤の需要を促進する主な要因です。

- しかし、鉛ベースの安定剤の使用に関する健康被害と厳しい政府規制が市場成長の妨げになると予想されます。

- とはいえ、環境に優しい選択肢として有機錫系安定剤の使用が増加していることから、市場調査には新たな機会が生まれると予想されます。

- アジア太平洋が世界のPVC安定剤市場を独占しています。この地域の国々における建築・建設を含むさまざまなエンドユーザー産業でのPVC安定剤需要の増加が、アジア太平洋市場を牽引しています。中国とインドがこの地域市場に大きく貢献しています。

PVC安定剤市場の動向

市場を独占する建築・建設セグメント

- ポリ塩化ビニル(PVC)は、建築・建設業界における主要なプラスチックとして際立っています。頑丈でありながら軽量であるため、耐候性、化学腐食、摩耗に対する耐久性が保証されています。PVCから作られる一般的な製品には、パイプ、ケーブル、窓枠、床材、屋根材などがあります。

- PVCパイプは、上下水道システムにおいて極めて重要な役割を果たしています。彼らは、スムーズで摩擦のない流れを確保し、ビルドアップ、スケーリング、および腐食に抵抗します。特に、PVCパイプは飲料水の輸送に安全であると考えられており、地下に設置した場合、100年を超える耐用年数を誇ります。さらに、コスト効率が高く、8~10回リサイクルすることができます。

- オックスフォード・エコノミクスは、世界の建設生産高が力強い成長軌道を描くと予測しており、現在の4兆2,000億米ドル超から2037年には13兆9,000億米ドル超に増加すると予測しています。

- 中国は、世界のPVCパイプの50~60%を生産し、世界を席巻しています。特に、塩化ビニル・ポリマーから作られる硬質チューブ、パイプ、ホースの最大の輸出国となっています。

- 2023年、中国の建設産業は実額で6.5%の成長を遂げました。国家統計局(NBS)の発表によると、同産業の経済貢献は最初の9ヵ月間で前年同期比7.2%増と急増しました。

- インベスト・インディアによると、都市化の動向によると、2030年までに人口の40%以上が都市部に居住するようになり、2,500万戸の中級住宅と手頃な価格の住宅がさらに必要となります。さらに、住宅都市省によると、AMRUT計画の下、約134,000戸の水道と102,000戸の下水道が整備されています。

- 米国では、パリ協定に合わせ、2030年までに排出量を2005年比で50~52%削減するという米国政府の目標があるため、今後数年間、PVC生産に影響が出る可能性が高いです。その結果、米国塩ビ業界は、温室効果ガス(GHG)排出を抑制するための実質的な対策を準備しており、2050年までにカーボンニュートラルを目指しています。

- さらに2023年12月には、米国環境保護庁(EPA)がPVC規制の計画を発表し、廃棄義務化の形を変える構えです。

- European Council of Vinyl Manufacturersによると、窓、パイプ、床材、屋根膜などの建築用製品には、欧州の塩ビの70%が使用されています。欧州の建築・建設業界では、塩ビは主要なプラスチックです。

- ドイツの堅調な経済は、商業スペースの需要を急増させています。特に、高品質でESGに準拠したオフィスビルへの関心が高まっており、プライム賃料が上昇していることからも明らかです。2023年第3四半期には24万6,000平方メートルのオフィススペースが稼動し、2024年には合計180万平方メートルになると予測されています。

- こうした動きを踏まえると、世界の建設業界の隆盛は、今後数年間のPVC安定剤の強気な見通しを示唆しています。

アジア太平洋地域が市場を独占

- アジア太平洋地域は、中国やインドなどの国々における建設や自動車などの産業からの需要の急増によって、PVC安定剤市場をリードしています。

- PVCパイプや床材は、耐久性、審美的な柔軟性、容易な設置、簡単な清掃、リサイクル性などの利点を提供します。建築・建設業界では、塩ビ屋根材はメンテナンスの手間が少なく、30年以上もつ長寿命が支持されています。

- 中国・香港の住宅当局は、低価格住宅の建設を推進するため、いくつかの施策を打ち出しています。当局は2030年までの10年間で30万1,000戸の公共住宅を供給することを目指しています。

- さらに、日本の建設業界も、ここ数年、塩ビ安定剤の主要な消費者となっています。日本では、三菱地所が2027年の完成を目標に、毎月4万3,000米ドルの家賃が見込まれる高級アパート50戸を擁する日本一の高層ビルを東京駅近くに建設するなど、注目すべき建設プロジェクトが行われています。

- PVCは、自動車業界において、従来型自動車や電気自動車のボンネット内や内装などに一般的に使用されています。

- 中国は世界最大の自動車メーカーのひとつです。OICAによると、2023年の中国の乗用車生産台数は2,600万台で、2022年比で10%以上増加しました。

- さらにOICAによると、2023年のインドの自動車生産台数は585万台で、2022年比で7%以上の増加を記録しました。同国の乗用車生産台数は478万台で、2022年比で7.9%増加し、市場の成長を支えています。

- 新華社通信のデータによると、中国の電子機器製造業は、生産台数の増加と国内および世界需要の回復に支えられ、2024年の年初4ヵ月に好調な業績を示しました。工業情報化部の報告によると、中国のエレクトロニクス産業の主要企業は、2024年1月から4月までの合計利益が前年同期比75.8%急増し、1,442億人民元(~203億米ドル)に達しました。

- インド包装産業協会(PIAI)は、インドの包装産業が予測期間中に22%の堅調な成長を遂げると予測しています。さらに、インドの包装市場は2025年までに2,048億1,000万米ドルに達する勢いであり、それまでのCAGRは26.7%という驚異的な伸びを誇っています。この急増は、今後数年間、インド全土でPVC安定剤の需要が高まることを裏付けています。

- このようなダイナミクスと政府の後押しを考えると、アジア太平洋地域は予測期間中にPVC安定剤市場で需要の高まりを記録する準備が整っています。

PVC安定剤産業の概要

PVC安定剤市場は、その性質上、部分的に断片化されています。主要企業(順不同)には、Baerlocher GmbH、ADEKA Corporation、Akdeniz Chemson、SONGWON、Valtris Specialty Chemicalsなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- PVCパイプ、チューブ、継手用安定剤の需要拡大

- 自動車産業での使用の増加

- その他の促進要因

- 抑制要因

- 鉛系安定剤の使用に関する健康被害と厳しい政府規制

- その他の阻害要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- タイプ別

- カルシウムベース

- 鉛ベース

- スズベース

- バリウム系

- その他のタイプ

- エンドユーザー産業別

- 建築・建設

- 自動車

- 電気・電子

- 包装

- フットウェア

- その他エンドユーザー産業

- 地域別

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- 北欧諸国

- トルコ

- ロシア

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他南米

- 中東・アフリカ

- サウジアラビア

- カタール

- アラブ首長国連邦

- ナイジェリア

- エジプト

- 南アフリカ

- その他中東とアフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Adeka Corporation

- Akdeniz Chemson

- Baerlocher GmbH

- Clariant

- Galata Chemicals

- Goldstab Organics Pvt. Ltd

- KD Chem Co. Ltd

- Kunshan Maijisen Composite Materials Co. Ltd

- Pau Tai Industrial Corp.

- PMC Group Inc.

- Ra Chemicals Pvt. Ltd

- Reagens SpA

- Shandong Jinchangshu New Material Technology Co. Ltd

- SONGWON

- Timah

- Valtris Specialty Chemicals

- Vikas Ecotech Ltd

第7章 市場機会と今後の動向

- 環境に優しい選択肢としての有機錫安定剤の使用増加

- その他の機会

The PVC Stabilizers Market size is estimated at 1.54 million tons in 2025, and is expected to reach 1.89 million tons by 2030, at a CAGR of 4.2% during the forecast period (2025-2030).

The COVID-19 pandemic adversely affected the PVC stabilizers market. Global lockdowns and severe government rules resulted in a catastrophic setback, as most production hubs were shut down. Nonetheless, the market recovered in 2021 and is expected to rise significantly in the coming years.

Key Highlights

- Over the short term, growing demand for stabilizers for PVC pipes, tubings, and fittings and increasing use in the automotive industry are the major factors driving demand for PVC stabilizers.

- However, health hazards and stringent government regulations regarding the use of lead-based stabilizers are expected to hinder the market's growth.

- Nevertheless, the rising usage of organo-tin stabilizers as an environmentally friendly option is expected to create new opportunities for the market studied.

- Asia-Pacific dominates the global PVC stabilizers market. Rising demand for PVC stabilizers in different end-user industries, including building and construction in the countries of this region, is driving the Asia-Pacific market. China and India are the major contributors to this regional market.

PVC Stabilizers Market Trends

The Building and Construction Segment to Dominate the Market

- Polyvinyl chloride (PVC) stands out as the predominant plastic in the building and construction industry. Its robust yet lightweight nature ensures durability against weathering, chemical corrosion, and abrasion. Common products crafted from PVC include pipes, cables, window profiles, flooring, and roofing.

- PVC pipes play a pivotal role in water, waste, and sewage systems. They resist build-up, scaling, and corrosion, ensuring a smooth, friction-free flow. Notably, PVC pipes are deemed safe for transporting drinking water, boasting a service life exceeding 100 years for underground installations. Additionally, they are cost-effective and can be recycled 8-10 times.

- Oxford Economics forecasts a robust growth trajectory for global construction output, projecting an increase from over USD 4.2 trillion currently to a staggering USD 13.9 trillion by 2037, predominantly fueled by the construction powerhouses of China, the United States, and India.

- China dominates the global landscape, producing 50-60% of the world's PVC pipes. Notably, it stands as the foremost exporter of rigid tubes, pipes, and hoses crafted from vinyl chloride polymers.

- In 2023, China's construction industry witnessed a 6.5% growth in actual value. The industry's economic contribution surged by 7.2% Y-o-Y during the initial nine months, as highlighted by the National Bureau of Statistics (NBS).

- As per Invest India, urbanization trends suggest that by 2030, over 40% of the population will reside in urban locales, driving the need for an additional 25 million mid-end and affordable housing units. Furthermore, according to the Ministry of Housing & Urban Affairs, around 134 lakh water tap connections and 102 lakh sewer/septage connections have been provided under the AMRUT scheme.

- PVC production in the United States is likely to be affected in the coming years due to the US government's target of reducing emissions by 50-52% from 2005 benchmarks by 2030, aligning with the Paris Agreement. Consequently, the US PVC industry is gearing up for substantial measures to curtail greenhouse gas (GHG) emissions, eyeing carbon neutrality by 2050.

- Furthermore, in December 2023, the US Environmental Protection Agency (EPA) unveiled plans to regulate PVC, a move poised to reshape disposal mandates.

- According to the European Council of Vinyl Manufacturers, windows, pipes, flooring, roofing membranes, and other building products use 70% of all European PVC. It is the leading plastic in the European building and construction industry.

- Germany's robust economy is driving a surge in demand for commercial spaces. Notably, there has been a growing interest in high-quality, ESG-compliant office buildings, evident from rising prime rents. In Q3 2023, 246,000 sq. m of office space came online, with forecasts suggesting a total of 1.8 million sq. m in 2024.

- Given these dynamics, the global construction industry's prominence suggests a bullish outlook for PVC stabilizers over the coming years.

Asia-Pacific to Dominate the Market

- Asia-Pacific leads the PVC stabilizers market, driven by surging demand from industries like construction and automotive in countries like China and India.

- PVC pipes and flooring offer benefits like durability, aesthetic flexibility, easy installation, simple cleaning, and recyclability. In the building and construction industry, PVC roofing is favored for its low maintenance and longevity, lasting over 30 years.

- The housing authorities of Hong Kong, China, have launched several measures to push the construction of low-cost housing. The officials aim to provide 301,000 public housing units in 10 years till 2030.

- In addition, Japan's construction industry has been another major consumer of PVC stabilizers in recent times. Japan is witnessing notable construction projects, including Mitsubishi State's endeavor of erecting the nation's tallest building near Tokyo station, featuring 50 luxury apartments projected to earn USD 43,000 monthly in rent, with a completion target of 2027.

- PVC is commonly used in under-the-hood applications, interiors, and other areas in conventional vehicles and electric vehicles in the automotive industry.

- China is one of the largest automotive manufacturers worldwide. According to OICA, in 2023, the production of passenger vehicles in China stood at 26 million units, an increase of more than 10% compared to 2022.

- Moreover, according to the OICA, in 2023, the total production of vehicles in India stood at 5.85 million units, registering an increase of more than 7% compared to 2022. The production of passenger vehicles in the country stood at 4.78 million units, registering an increase of 7.9% compared to the year 2022, thereby supporting the growth of the market.

- As per data from Xinhua News Agency, China's electronics manufacturing industry showcased robust performance in the initial four months of 2024, buoyed by rising production and a rebound in both domestic and global demand. Major companies in China's electronics industry, as reported by the Ministry of Industry and Information Technology, saw their combined profits surge by 75.8% Y-o-Y, reaching CNY 144.2 billion (~USD 20.3 billion) from January to April 2024.

- The Packaging Industry Association of India (PIAI) projects the Indian packaging industry to grow at a robust 22% during the forecast period. Furthermore, the Indian packaging market is on track to hit USD 204.81 billion by 2025, boasting an impressive CAGR of 26.7% until then. This surge underscores a rising demand for PVC stabilizers across India over the coming years.

- Given these dynamics and government backing, Asia-Pacific is poised to register heightened demand in the PVC stabilizers market during the forecast period.

PVC Stabilizers Industry Overview

The PVC stabilizers market is partially fragmented by nature. The major players (not in any particular order) include Baerlocher GmbH, Adeka Corporation, Akdeniz Chemson, SONGWON, and Valtris Specialty Chemicals.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand for Stabilizers for PVC Pipes, Tubings and Fittings

- 4.1.2 Increasing Use In the Automotive Industry

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Health Hazards and Stringent Government Regulations Regarding the Use of Lead-based Stabilizers

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 By Type

- 5.1.1 Calcium-based

- 5.1.2 Lead-based

- 5.1.3 Tin-based

- 5.1.4 Barium-based

- 5.1.5 Other Types

- 5.2 By End-user Industry

- 5.2.1 Building and Construction

- 5.2.2 Automotive

- 5.2.3 Electrical and Electronics

- 5.2.4 Packaging

- 5.2.5 Footwear

- 5.2.6 Other End-user Industries

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 NORDIC Countries

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Qatar

- 5.3.5.3 United Arab Emirates

- 5.3.5.4 Nigeria

- 5.3.5.5 Egypt

- 5.3.5.6 South Africa

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Adeka Corporation

- 6.4.2 Akdeniz Chemson

- 6.4.3 Baerlocher GmbH

- 6.4.4 Clariant

- 6.4.5 Galata Chemicals

- 6.4.6 Goldstab Organics Pvt. Ltd

- 6.4.7 KD Chem Co. Ltd

- 6.4.8 Kunshan Maijisen Composite Materials Co. Ltd

- 6.4.9 Pau Tai Industrial Corp.

- 6.4.10 PMC Group Inc.

- 6.4.11 Ra Chemicals Pvt. Ltd

- 6.4.12 Reagens SpA

- 6.4.13 Shandong Jinchangshu New Material Technology Co. Ltd

- 6.4.14 SONGWON

- 6.4.15 Timah

- 6.4.16 Valtris Specialty Chemicals

- 6.4.17 Vikas Ecotech Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rising Usage of Organo-tin Stabilizers as an Environment-friendly Option

- 7.2 Other Opportunities