|

市場調査レポート

商品コード

1716717

単相ポータブル発電機市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Single Phase Portable Generators Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 単相ポータブル発電機市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月27日

発行: Global Market Insights Inc.

ページ情報: 英文 125 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

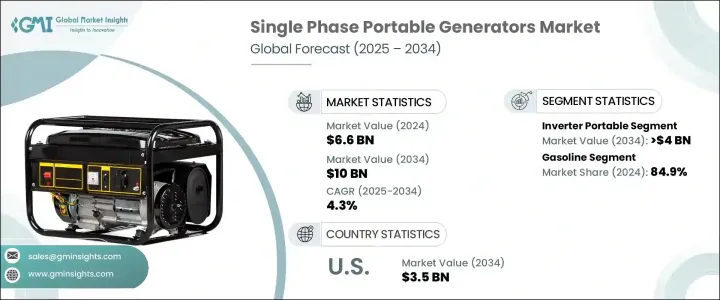

単相ポータブル発電機の世界市場は、2024年に66億米ドルを生み出し、2025年から2034年にかけてCAGR 4.3%で成長すると予測されています。

この成長の原動力は、インフラ開発への投資の増加、急速な都市化、先進国および新興経済諸国全体で進行中の建設ブームです。住宅や商業施設の建設プロジェクトの急増と、緊急事態への備えに対する消費者の意識の高まりが、ポータブル電源ソリューションの需要を押し上げています。さらに、通信業界の拡大や、ハリケーン、洪水、山火事などの気象関連災害の頻度と激しさの上昇が、信頼性の高い電源への需要を引き続き煽っています。

世界の電力網が老朽化し、課題が増えるにつれて、携帯型バックアップ電源ソリューションの必要性が顕著になっています。また、スマートホームの普及と屋外レクリエーション活動の人気の高まりも、単相ポータブル発電機の使用増加に寄与しています。さらに、分散型エネルギー・ソリューションへのシフトと、グリッド故障時の信頼できる電力へのニーズが、こうした多用途デバイスの採用を後押ししています。環境問題への関心が高まる中、メーカーはポータブル発電機の燃料効率の改善と排出量の削減に注力し、その魅力をさらに高めています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 66億米ドル |

| 予測金額 | 100億米ドル |

| CAGR | 4.3% |

単相ポータブル発電機は、単一の電圧波形で交流電流を生成するように設計されているため、幅広いシナリオに適応して使いやすいです。携帯性とコンパクトな設計により、常時電力供給が不可能な場所での一時的な電力供給に最適です。災害への備えとリスク軽減に対する意識の高まりにより、特に自然災害の多い地域では、これらの発電機に対する需要が大幅に増加しています。停電時にバックアップ電力を供給するための住宅環境でも、工具や機器に電力を供給するための建設現場でも、これらの発電機は継続性と安全性を維持するために不可欠な要素であり続けています。

市場は製品タイプによって区分され、従来型ポータブル発電機とインバーターポータブル発電機が主要なカテゴリーです。インバーターポータブル発電機分野は、2034年までに40億米ドルを創出すると予測されています。これらの発電機は、コンパクトなサイズ、静かな動作、軽量設計、高い燃料効率などの優れた利点を提供し、住宅および商業用途でますます人気が高まっています。インバーター発電機は、ノイズを最小限に抑えながら安定した電力を供給できることから、消費者に支持されており、繊細な電子機器への電力供給や非常時のシームレスな電力供給を確保するのに適しています。

燃料タイプでは、市場はさらにディーゼル、ガソリン、その他の燃料オプションに区分されます。ガソリン駆動の単相ポータブル発電機は、2024年のシェア84.9%で市場を独占しています。手ごろな価格で、必要な電力が少ない用途に適しているため、住宅や中小企業での用途に好まれています。ガソリン発電機は、停電時や野外活動時のバックアップ電源として広く使用されており、市場での存在感を高めています。さらに、燃料効率と排出制御技術の進歩により、ガソリン発電機の需要は長期的に維持されると予想されます。

米国の単相ポータブル発電機市場は、2024年に25億米ドルを生み出し、今後数年間で力強い成長が予測されます。信頼性が高く継続的なエネルギー・ソリューションに対する需要の増加、自然災害による頻繁な電力途絶、送電網インフラの老朽化が、市場成長を促す重要な要因となっています。住宅用および商業用アプリケーションにおける信頼性の高いバックアップ電源ソリューションへのニーズは、これらの発電機への需要を継続的に煽り、電力依存が高まる社会における関連性を確実なものにしています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 規制状況

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長ポテンシャル分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略的展望

- イノベーションと持続可能性の展望

第5章 市場規模・予測:製品別、2021年~2034年

- 主要動向

- 従来型ポータブル

- インバーターポータブル

第6章 市場規模・予測:燃料・定格出力別、2021年~2034年

- 主要動向

- ディーゼル

- 20 kW未満

- 20-50 kW

- 50-100 kW

- ガソリン

- 2 kW未満

- 2 kW-5 kW

- 6 kW-8 kW

- 8 kW~15 kW

- その他

第7章 市場規模・予測:最終用途別、2021年~2034年

- 主要動向

- 住宅

- 商業

第8章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ロシア

- 英国

- ドイツ

- フランス

- スペイン

- オーストリア

- イタリア

- アジア太平洋

- オーストラリア

- 日本

- 中国

- インド

- インドネシア

- シンガポール

- ベトナム

- 中東

- サウジアラビア

- アラブ首長国連邦

- カタール

- トルコ

- イラン

- オマーン

- アフリカ

- エジプト

- ナイジェリア

- アルジェリア

- 南アフリカ

- ラテンアメリカ

- メキシコ

- アルゼンチン

- ブラジル

第9章 企業プロファイル

- Allmand Bros

- Atlas Copco

- Briggs &Stratton

- Caterpillar

- Champion Power Equipment

- Cummins

- Deere &Company

- DuroMax Power Equipment

- FIRMAN Power Equipment

- Generac Power Systems

- HIMOINSA

- Honda India Power Products

- Kirloskar

- Rehlko

- Wacker Neuson

- Westinghouse Electric Corporation

- Yamaha Motor

- YANMAR

The Global Single Phase Portable Generators Market generated USD 6.6 billion in 2024 and is projected to grow at a CAGR of 4.3% from 2025 to 2034. This growth is driven by increasing investments in infrastructure development, rapid urbanization, and the ongoing construction boom across developed and developing economies. The surge in residential and commercial construction projects, coupled with rising consumer awareness about emergency preparedness, is propelling the demand for portable power solutions. Additionally, the telecommunications industry's expansion and the rising frequency and intensity of weather-related disasters, such as hurricanes, floods, and wildfires, continue to fuel the demand for reliable power sources.

As global electricity grids age and face increasing challenges, the need for portable backup power solutions becomes more prominent. The growing adoption of smart homes, coupled with the rising popularity of outdoor recreational activities, also contributes to the increasing use of single-phase portable generators. Moreover, the shift toward decentralized energy solutions and the need for reliable power during grid failures are encouraging the adoption of these versatile devices. With increasing environmental concerns, manufacturers are focusing on improving fuel efficiency and reducing emissions in portable generators, further enhancing their appeal.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.6 Billion |

| Forecast Value | $10 Billion |

| CAGR | 4.3% |

Single-phase portable generators are designed to produce alternating current with a single voltage waveform, making them adaptable and easy to use in a wide range of scenarios. Their portability and compact design make them ideal for providing temporary power in locations where a permanent electricity supply is unavailable. Heightened awareness of disaster preparedness and risk mitigation has led to a significant rise in demand for these generators, particularly in regions prone to natural disasters. Whether used in residential settings to provide backup power during outages or in construction sites for powering tools and equipment, these generators remain an essential component in maintaining continuity and safety.

The market is segmented based on product type, with conventional portable and inverter portable generators being the dominant categories. The inverter portable generator segment is anticipated to generate USD 4 billion by 2034. These generators offer superior benefits such as compact size, quiet operation, lightweight design, and high fuel efficiency, making them increasingly popular in residential and commercial applications. Consumers favor inverter generators for their ability to provide stable power with minimal noise, making them suitable for powering sensitive electronic devices and ensuring a seamless power supply during emergencies.

In terms of fuel type, the market is further segmented into diesel, gasoline, and other fuel options. Gasoline-powered single-phase portable generators dominated the market with an 84.9% share in 2024. Their affordability and suitability for applications with low power requirements make them the preferred choice for residential and small business applications. Gasoline-powered generators are widely used for backup power during outages and outdoor activities, contributing to their strong market presence. Additionally, advancements in fuel efficiency and emission control technologies are expected to sustain the demand for gasoline-powered generators in the long term.

The U.S. Single Phase Portable Generators Market generated USD 2.5 billion in 2024, with strong growth projected in the coming years. Increasing demand for reliable, continuous energy solutions, frequent power disruptions caused by natural disasters, and the aging grid infrastructure are significant factors driving market growth. The need for dependable backup power solutions in residential and commercial applications continues to fuel demand for these generators, ensuring their relevance in an increasingly power-dependent society.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Product, 2021 - 2034 ('000 Units & USD Million)

- 5.1 Key trends

- 5.2 Conventional portable

- 5.3 Inverter portable

Chapter 6 Market Size and Forecast, By Fuel & Power Rating, 2021 - 2034 ('000 Units & USD Million)

- 6.1 Key trends

- 6.2 Diesel

- 6.2.1 < 20 kW

- 6.2.2 20 - 50 kW

- 6.2.3 > 50 - 100 kW

- 6.3 Gasoline

- 6.3.1 < 2 kW

- 6.3.2 2 kW - 5 kW

- 6.3.3 6 kW - 8 kW

- 6.3.4 > 8 kW - 15 kW

- 6.4 Others

Chapter 7 Market Size and Forecast, By End Use, 2021 - 2034 ('000 Units & USD Million)

- 7.1 Key trends

- 7.2 Residential

- 7.3 Commercial

Chapter 8 Market Size and Forecast, By Region, 2021 - 2034 ('000 Units & USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Russia

- 8.3.2 UK

- 8.3.3 Germany

- 8.3.4 France

- 8.3.5 Spain

- 8.3.6 Austria

- 8.3.7 Italy

- 8.4 Asia Pacific

- 8.4.1 Australia

- 8.4.2 Japan

- 8.4.3 China

- 8.4.4 India

- 8.4.5 Indonesia

- 8.4.6 Singapore

- 8.4.7 Vietnam

- 8.5 Middle East

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 Qatar

- 8.5.4 Turkey

- 8.5.5 Iran

- 8.5.6 Oman

- 8.6 Africa

- 8.6.1 Egypt

- 8.6.2 Nigeria

- 8.6.3 Algeria

- 8.6.4 South Africa

- 8.7 Latin America

- 8.7.1 Mexico

- 8.7.2 Argentina

- 8.7.3 Brazil

Chapter 9 Company Profiles

- 9.1 Allmand Bros

- 9.2 Atlas Copco

- 9.3 Briggs & Stratton

- 9.4 Caterpillar

- 9.5 Champion Power Equipment

- 9.6 Cummins

- 9.7 Deere & Company

- 9.8 DuroMax Power Equipment

- 9.9 FIRMAN Power Equipment

- 9.10 Generac Power Systems

- 9.11 HIMOINSA

- 9.12 Honda India Power Products

- 9.13 Kirloskar

- 9.14 Rehlko

- 9.15 Wacker Neuson

- 9.16 Westinghouse Electric Corporation

- 9.17 Yamaha Motor

- 9.18 YANMAR