|

市場調査レポート

商品コード

1444055

航空用C4ISR:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Air-based C4ISR - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 航空用C4ISR:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

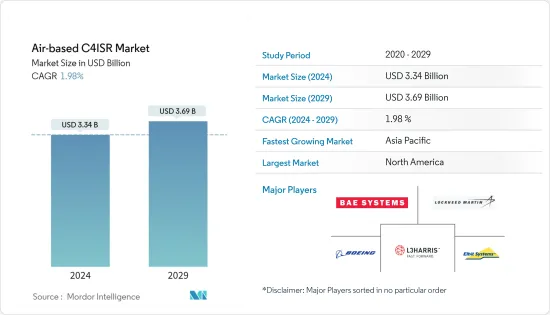

航空用C4ISR市場規模は、2024年に33億4,000万米ドルと推定され、2029年までに36億9,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に1.98%のCAGRで成長します。

COVID-19のパンデミックが世界経済に深刻な打撃を与えているにもかかわらず、その影響は2020年と2021年に増加し続けた世界の軍事支出には影響していないです。世界の軍事支出は2021年に総額2兆1,130億米ドルに達し、増加しています。このような多額の支出は、COVID-19のパンデミックが防衛システムの開発と調達に与えた影響がごくわずかであることを示しています。軍事支出の増加により、来年は航空用C4ISR市場が牽引されると予想されます。

世界中で政治的、地理的緊張が高まっているため、航空用C4ISRシステムの需要が高まっています。信号認識と生存性を強化するための無人航空機(UAV)、電子支援/対抗措置(ESM/ECM)、空挺用C2、高度な戦術航空偵察システム、および空挺警戒管制システム(AWACS)に対する需要の急速な増加により、航空用C4ISR市場の成長が促進されています。

近代化計画や各国の脅威認識の高まりなどの要因により、航空用C4ISRシステムの需要の大部分は、予測期間中にアジア太平洋地域で発生すると予想されます。

航空用C4ISR市場動向

世界の国防費の伸び

国際戦略情勢の重大な変化により、国際安全保障システムの構成は、増大する覇権主義、一国主義、強権政治によって損なわれ、現在進行中のいくつかの世界紛争を引き起こしています。

領土権の不確実性、政治的緊張、軍事大国間の普遍的な優位性の探求は、地政学的なシナリオを乱す主な原因の一つです。この点に関して、政府の最も一般的な反応は、それぞれの国の安全を改善するために軍事支出を増やすことです。

COVID-19のパンデミックによる経済的影響にもかかわらず、世界の国防支出は2020年と2021年も増加し続けました。2021年の最大の軍事支出国は米国、中国、インド、英国、ロシアであり、これらを合わせると世界の軍事支出の62%を占めました。

各国に対する脅威が高まるにつれ、軍隊のC4ISR能力を強化することがどの国にとっても重要になっています。これに関連して、さまざまな国のC4ISR能力を効果的に向上させるためのいくつかの軍事計画が現在進行中です。これらのプログラムを促進するために、各国は先住民族の開発または世界のベンダーからの調達を通じて、そのような能力の強化に巨額の投資を行っています。これらの投資は、防衛支出の増加によってさらに促進されます。

近年、これらの地域の国々はC4ISRシステムを組み込んだ新世代のプラットフォームや機器を発注しており、そのような開発プログラムもいくつか進行中です。これらのプログラムは予測期間中に実行される予定です。

このようなプラットフォームや装備の開発と調達には、システムのコストが膨大であるため、各国からの莫大な防衛費が必要となります。したがって、防衛支出の増加が今後数年間の市場の成長を促進すると予想されます。

アジア太平洋地域は予測期間中に最高の成長を記録

アジア太平洋地域は、中国、インド、日本などの軍事支出が高い国の存在により、他の地域と比較して最も高い成長率が見込まれます。複数の国の陸と海の国境に地政学的な緊張が存在するため、C4ISRの調達は地域全体で増加する可能性があります。アジア太平洋地域全体での強制的な近代化努力により、C4ISRシステムの調達も増加すると予想されます。中国とインドは国軍の能力強化に向けて大きく前進しており、世界の国防費上位5カ国に入っています。

テクノロジーと電子戦の進歩により、電子戦に効果的に対処するためのテクノロジーの需要が高まっています。これに合わせて、世界の技術に追いつくために、軍隊でも新たな開発が行われています。たとえば、2022年 3月、インド国防省は、インド空軍戦闘機に高度電子戦スイートを供給するためにBELとパートナーシップを締結しました。

軍事目的の通信技術を向上させる取り組みにおいて、韓国は既存の技術のアップグレードに投資してきました。その結果、軍用レベルの通信の需要に応えるための新たな契約やパートナーシップが観察されています。例えば、

2021年9月、ハンファシステムズとLIG Nex1は、韓国初の専用軍事通信衛星であるANASIS-IIに関連する韓国国防調達計画局(DAPA)から契約を獲得したと発表しました。ハンファシステムズは、2020年7月に宇宙に打ち上げられたANASIS-II衛星システムに関連した2024年までのネットワーク制御システムの確立と携帯地上端末の製造の両方で3,600億ウォン(3億700万米ドル)の契約を獲得したと発表しました。

このような発展により、予測期間中に市場は大幅な成長率に向かうと予想されます。

航空用C4ISR業界の概要

C4ISRシステムの技術進歩と多機能システムへの需要により、メーカーは費用対効果の高いソリューションの研究開発への投資を推進しています。たとえば、回転翼UAVのプロトタイプがHindustan Aeronautics Limited(HAL)によって発表されました。2021年 5月、Aeronauticsは長距離海上哨戒任務用に小型戦術ドローンOrbiter 4を発表しました。 UASは24時間以上の耐久性があり、複数のペイロードを同時に運搬および運用できます。滑走路に依存せず(あらゆるタイプの船舶で離着陸可能)、高度な画像処理機能、自動離陸および回収システム、GPS/データリンクの有無にかかわらず航行できる機能を備えています。地域企業の技術と製品ポートフォリオにおけるこのような進歩は、近い将来の戦略的拡大計画に役立つと予想されます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競合の程度

第5章 市場セグメンテーション

- タイプ

- C4システム

- ISR

- 電子戦

- 地域

- 北米

- 米国

- カナダ

- 欧州

- 英国

- フランス

- ドイツ

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋

- ラテンアメリカ

- ブラジル

- その他ラテンアメリカ

- 中東とアフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- その他中東とアフリカ

- 北米

第6章 競合情勢

- ベンダーの市場シェア

- 企業プロファイル

- The Boeing Company

- General Dynamics Corporation

- Elbit Systems Ltd

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- BAE Systems PLC

- CACI International Inc.

- Kratos Defense &Security Solutions Inc.

- Rheinmetall Defense

- L3Harris Technologies Inc.

- Denel SOC Ltd

- ThalesRaytheonSystems

第7章 市場機会と将来の動向

The Air-based C4ISR Market size is estimated at USD 3.34 billion in 2024, and is expected to reach USD 3.69 billion by 2029, growing at a CAGR of 1.98% during the forecast period (2024-2029).

Despite the COVID-19 pandemic hitting the global economy severely, the impact of the same is not felt on the global military expenditure, which continued to increase in 2020 and 2021. The global military expenditure reached a total of USD 2.113 trillion in 2021, increasing by about 0.7% compared to 2020. Such high expenditure indicates the negligible impact the COVID-19 pandemic had on defense systems development and procurements. The growth in military spending is expected to drive the air-based C4ISR market in the coming year.

The increasing political and geographical tensions around the world are propelling the demand for airborne C4ISR systems. The rapid growth in demand for unmanned aerial vehicles (UAVs), electronic support/countermeasures (ESM/ECM), airborne C2, advanced tactical air reconnaissance system, and airborne warning and control systems (AWACS) to enhance signal awareness and survivability is driving the growth of the air-based C4ISR market.

A majority of the demand for air-based C4ISR systems is anticipated to be generated in the Asia-Pacific region during the forecast period, due to factors, like modernization plans and an increase in the threat perception of countries.

Air-based C4ISR Market Trends

Growth in the Global Defense Expenditure

Owing to profound changes in the international strategic landscape, the configuration of international security systems has been undermined by the growing hegemonism, unilateralism, and power politics, which fueled several ongoing global conflicts.

Uncertainties in territorial rights, political tensions, and the quest for universal dominance among the military powerhouses are among the major causes disturbing the geopolitical scenario. In this regard, the most common reaction of the governments is to increase their military spending, to improve security in their respective countries.

Despite the economic impact of the COVID-19 pandemic, global defense expenditure continued to increase in 2020 and 2021. According to SIPRI, the global military expenditure in 2021 rose to USD 2113 billion, an increase of 0.7% in from 2020. billion. Global spending in 2021 was 12% higher than in 2012. The five largest military spenders in 2021 were the United States, China, India, the United Kingdom, and Russia, which together accounted for 62% of world military spending.

As the threats for the countries become higher, enhancing the militaries' C4ISR capabilities becomes important for every country. In this regard, several military programs are currently underway to effectively upgrade the C4ISR capabilities of various countries. To facilitate these programs, countries are investing huge amounts into the enhancement of such capabilities, either through indigenous development or through procurement from global vendors. These investments are further driven by the growth in defense expenditures.

In recent years, countries in these regions have placed orders for newer generation platforms and equipment that incorporate C4ISR systems whereas several such development programs are also underway. These programs are expected to run during the forecast period.

The development and procurement of such platforms and equipment demands huge defense spending from the countries, as the cost of the systems is immense. Thus, the growth in defense spending is expected to drive the growth of the market in the coming years.

The Asia-Pacific region to Register Highest Growth During the Forecast Period

The Asia-Pacific region is expected to witness the highest growth rate as compared to the other regions, due to the presence of high military spending countries, such as China, India, and Japan. With the presence of geopolitical tensions in the land and sea borders in multiple countries, the procurement of C4ISR is likely to increase across the region. Forced modernization efforts across the Asia-Pacific region are also expected to increase the procurement of C4ISR systems. China and India are taking huge strides toward strengthening the capabilities of their armed forces and are among the top five defense-spending countries in the world.

The increasing technology and electronic warfare have been driving the demand for technologies to effectively tackle electronic warfare. In line with this, new developments have been occurring in the army, to keep up with global technology. For instance, In March 2022, the Defence Ministry of India signed a partnership with BEL to supply an Advanced Electronic Warfare suite for the Indian Air Force fighter jets. The contract was signed between the Ministry of Defense and Bharat Electronics Limited (BEL), with an estimated value of INR 1993 Crore.

In efforts to increase communications technology for military purposes, south Korea has been investing in upgrading its existing technologies. As a result, new contracts and partnerships have been observed, to cater to the demand for military-grade communications. For instance,

In September 2021, Hanwha Systems and LIG Nex1 have announced that they have secured contracts from South Korea's Defense Acquisition Program Administration (DAPA) linked to ANASIS-II, the country's first dedicated military communications satellite. Hanwha Systems stated that they was awarded a KRW360 billion (USD307 million) contract to both establish a network control system and manufacture portable ground terminals by 2024 linked to the ANASIS-II satellite system, which launched into space in July 2020.

Such developments are expected to drive the market towards significant growth rates during the forecast period.

Air-based C4ISR Industry Overview

The prominent players in the air-based C4ISR market are Lockheed Martin Corporation, the Boeing Company, BAE Systems PLC, L3Harris Technologies Inc., Lockheed Martin Corporation, and Elbit Systems Ltd. However, there are many manufacturers that provide C4ISR solutions for air, land, and sea platforms. The regional manufacturers are gradually growing their presence in the market due to the support of their governments and partnerships with global players. Technological advancement in C4ISR systems and the demand for multi-functional systems are propelling the investments of manufacturers in the research and development of cost-effective solutions. For instance, a prototype of a rotary-wing UAV was unveiled by Hindustan Aeronautics Limited (HAL), In May 2021, Aeronautics introduced its Orbiter 4 small tactical drone for long-range maritime patrol missions. The UAS has an endurance of more than 24 hours and can carry and operate multiple payloads simultaneously. It is airstrip independent (can take off and land on any type of vessel) and features advanced image processing capabilities, an automatic takeoff and recovery system, and the ability to navigate with or without GPS/data link. Such advancements in technology and product portfolio of the regional companies are anticipated to help the strategic expansion plans in the near future.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 C4 Systems

- 5.1.2 ISR

- 5.1.3 Electronic Warfare

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.2 Europe

- 5.2.2.1 United Kingdom

- 5.2.2.2 France

- 5.2.2.3 Germany

- 5.2.2.4 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Japan

- 5.2.3.4 South Korea

- 5.2.3.5 Rest of Asia-Pacific

- 5.2.4 Latin America

- 5.2.4.1 Brazil

- 5.2.4.2 Rest of Latin America

- 5.2.5 Middle-East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 United Arab Emirates

- 5.2.5.3 South Africa

- 5.2.5.4 Rest of Middle-East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share**

- 6.2 Company Profiles*

- 6.2.1 The Boeing Company

- 6.2.2 General Dynamics Corporation

- 6.2.3 Elbit Systems Ltd

- 6.2.4 Lockheed Martin Corporation

- 6.2.5 Northrop Grumman Corporation

- 6.2.6 BAE Systems PLC

- 6.2.7 CACI International Inc.

- 6.2.8 Kratos Defense & Security Solutions Inc.

- 6.2.9 Rheinmetall Defense

- 6.2.10 L3Harris Technologies Inc.

- 6.2.11 Denel SOC Ltd

- 6.2.12 ThalesRaytheonSystems