|

市場調査レポート

商品コード

1687221

C4ISR:市場シェア分析、産業動向・統計、成長予測(2025~2030年)C4ISR - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| C4ISR:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 173 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

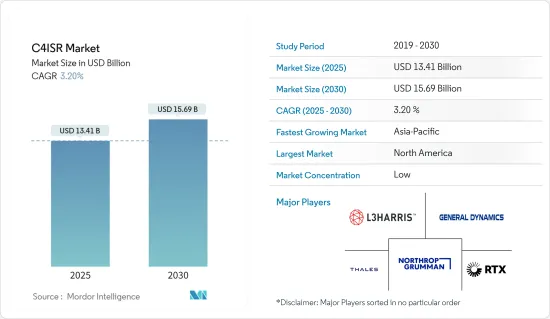

C4ISRの市場規模は2025年に134億1,000万米ドルと推定・予測され、予測期間中(2025-2030年)のCAGRは3.2%で、2030年には156億9,000万米ドルに達すると予測されます。

非対称戦に対する需要の高まりに加え、ネットワーク中心の戦闘管理や無人車両のような先進技術に対する需要の高まりが、予測期間中の市場成長を加速すると予想されます。軍人の状況認識を向上させるために監視範囲と能力を強化したISRシステムに情報収集センサーを統合することは、この地域のISR市場の成長を促進すると予想されます。

ISRシステムとペイロードの小型化と精度向上への注目の高まりが、あらゆるプラットフォームでの利用を促進しています。高い信頼性と低コストでの入手が可能なことから、軍はこれらのシステムを大量に調達しています。新たな脅威が出現するにつれ、これらのシステムはその有用性から軍事的な備えとして不可欠なものとなっています。

急速な技術開発が防衛産業における破壊的技術を生み出しています。現在の焦点は、AIと機械学習技術をISRプラットフォームに組み込むことです。また、軍はオープンアーキテクチャーISRシステムへのシフトにも注力しています。無人システムや自律機能を備えたシステムに対する需要の高まりは、今後数年間の市場調査を推進すると予想されます。

さまざまなC4ISRシステムの採用が進む一方で、エンドユーザーには多くの課題が突きつけられています。C4ISR業界の技術進歩はかつてない速度で成長しているが、生成されるデータ量の増加は軍や業界関係者に多くの課題を突きつけています。

C4ISR市場の動向

予測期間中、宇宙分野が最も高い成長を遂げる

宇宙におけるC4ISR技術には、高度な衛星システム、リモートセンシング、データ分析が含まれます。これらは、正確でタイムリーな情報収集、戦略的監視、偵察を可能にし、国家安全保障における情報に基づく意思決定に不可欠です。ハイブリッド・シナリオに移行しつつある戦争の様相の変化は、共同作戦に支えられ、効果的な作戦を可能にする相互運用性を必要とします。

軍事衛星と偵察ドローンはもう何十年も使われているが、擬似高高度衛星(HAPS)の登場は、カバー範囲とコストの面でドローンと衛星のギャップを埋めました。HAPSは、地上と衛星ベースの通信システムの長所を取り入れています。従来の静止衛星よりもはるかに経済的な価格対性能マージンで音声、ビデオ、ブロードバンド・サービスを効率的に提供することで、衛星の容量と性能の制限をなくします。

例えば、2023年11月、ノースロップ・グラマン社は、北極衛星ブロードバンド・ミッション(ASBM)の熱真空試験を完了しました。同様に、2023年2月、米国国家地理空間情報局は、米国の同盟国に商業衛星画像を提供するため、マキサー・テクノロジーズに1億9,200万米ドルの5年契約を発注しました。マキサーは同盟国に3次元データ・サービスも提供します。このような開発は、予測期間中に宇宙ベースC4ISRセグメントの見通しを増強すると予想されます。

北米は予測期間中に最も高い成長が見込まれる

北米地域は現在市場を独占しており、予測期間中もその支配が続くと見られています。これは主に米国とカナダ政府による様々な陸・空・海・宇宙ISRシステムの調達によるものです。2023年度、米国国防総省は、指揮、制御、通信、コンピュータ、情報システムに127億米ドルを割り当てた。米国軍は、特殊任務機群、電子戦機(EC-37B)、戦場空中通信ノード機(E-11A)、海上哨戒機(P-8A)の近代化を発注中です。2022年から2029年の間に、合計12機のP-8Aと5機のE-11Aが納入される予定です。高度な通信システムや状況認識システムの開発へのこうした投資は、調査対象市場の成長を加速させると予想されます。

さらに2022年3月、カナダ国防省は、空域調整センター近代化(ASCCM)プロジェクトの一環として、TORCH-Xベースのソリューションを提供するためにエルビット・システムズUKを選定しました。このプロジェクトでは、エルビット・システムズUKはTORCH-Xベースのバトル・マネジメント・アプリケーション(BMA)の共同空域バージョンを提供する予定であり、ローカルまたは認識された空域画像を常時表示することで状況認識を提供し、複雑な陸上および共同戦域における航空資産の効果的な調整を可能にします。このシステムはエルビット・システムズのE-CIXTMオープンアーキテクチャーフレームワークを利用して運用され、カナダ軍のレガシーアプリケーションや戦術データリンクへの接続を可能にする一方、カナダ軍のデジタル変革計画を支援する新しいアプリケーションの将来的な統合を可能にします。このように、防衛能力強化への関心の高まりと先進的なC4ISRシステムの採用拡大が、この地域全体の市場成長の原動力となっています。

C4ISR産業の概要

C4ISR市場は細分化されており、世界中の軍隊を支援する多くの国際的・地域的プレーヤーが存在します。C4ISR市場の著名なプレイヤーとしては、Northrop Grumman Corporation、RTX Corporation、L3Harris Technologies, Inc.、THALES、General Dynamics Corporationなどが挙げられます。各社は、さまざまな地域でのプレゼンスを拡大し、軍からの新規契約を獲得するために新たな戦略を策定しています。市場プレーヤーは、他の地域でのプレゼンスを拡大するため、地元メーカーとJVやパートナーシップを積極的に結んでいます。このような計画に加え、AIや量子ネットワーキングのような技術と統合されたC4ISRシステムを開発するための研究開発への投資も、企業が新規顧客を獲得し、今後数年間で市場でのシェアを拡大するのに役立つと予想されます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手・消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- プラットフォーム

- 航空

- 陸上

- 海洋

- 宇宙

- 目的

- 指揮・統制・通信・コンピュータ(C4)

- 情報・監視・偵察(ISR)

- 電子戦(EW)

- 地域

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- ロシア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- その他ラテンアメリカ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- トルコ

- その他中東とアフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- Elbit Systems Ltd

- BAE Systems PLC

- Saab AB

- THALES

- RTX Corporation

- L3Harris Technologies, Inc.

- CACI INTERNATIONAL INC.

- General Dynamics Corporation

- Honeywell International Inc.

- The Boeing Company

- Leidos

- Israel Aerospace Industries Ltd.

第7章 市場機会と今後の動向

The C4ISR Market size is estimated at USD 13.41 billion in 2025, and is expected to reach USD 15.69 billion by 2030, at a CAGR of 3.2% during the forecast period (2025-2030).

The growing demand for asymmetric warfare, along with increasing demand for advanced technologies like network-centric battle management and unmanned vehicles, is expected to accelerate the market growth during the forecast period. The integration of intelligence-gathering sensors into the ISR systems with enhanced surveillance range and capabilities for better situational awareness of military personnel is expected to propel the growth of the ISR market in the region.

The increasing focus on miniaturization and improving the accuracy of the ISR systems and payloads are propelling their utilization across all platforms. Their high reliability and availability at low costs have propelled militaries to procure these systems in abundance. As a new line of threats emerges, these systems have become integral to military preparedness due to their utility.

Rapid technological developments are breeding disruptive technologies in the defense industry. The current focus is on incorporating AI and machine learning technologies into ISR platforms. Militaries are also focusing on shifting toward open-architecture ISR systems. The growing demand for unmanned systems and systems with autonomous capabilities is expected to propel the market studied in the coming years.

While the adoption of a variety of C4ISR systems is increasing, it is presenting a host of challenges for end users, thereby putting pressure on manufacturers to help them overcome the challenges. Although technological advancements in the C4ISR industry are growing at unprecedented rates, the increasing amount of generated data is presenting a host of challenges for militaries and industry players.

C4ISR Market Trends

Space Segment Will Witness Highest Growth During the Forecast Period

C4ISR technologies in space encompass advanced satellite systems, remote sensing, and data analytics. These enable precise and timely intelligence gathering, strategic surveillance, and reconnaissance, which is crucial for informed decision-making in national security. The changing face of warfare, moving toward hybrid scenarios, will be underpinned by joint operations and will require interoperability to allow effective operation.

Though military satellites and surveillance drones have been used for decades now, the advent of pseudo-high-altitude satellites (HAPS) has bridged the gap between drones and satellites in terms of coverage and cost. HAPS incorporates the best aspects of terrestrial and satellite-based communication systems. They eliminate the capacity and performance limitations of satellites by efficiently delivering voice, video, and broadband services at much more economical pricing vs. performance margins than conventional geostationary satellites.

For instance, in November 2023, Northrop Grumman Corporation completed Thermal Vacuum tests on the Arctic Satellite Broadband Mission (ASBM), a two-satellite constellation designed to deliver broadband communications to the Northern polar region for the US Space Force and Space Norway. Similarly, in February 2023, The National Geospatial-Intelligence Agency awarded Maxar Technologies a five-year contract worth USD 192 million to provide commercial satellite imagery to US allies. Maxar will also provide three-dimensional data services to the allies. Such developments are expected to augment the prospects of the Space-based C4ISR segment during the forecast period.

North America is expected to witness highest growth during the forecast period

The North American region currently dominates the market and is expected to continue its domination during the forecast period. This is mainly due to the procurement of various land, air, sea, and space ISR systems by the US and Canadian governments. For FY 2023, the US Pentagon allocated USD 12.7 billion for command, control, communications, computers, and intelligence systems. The US armed forces are modernizing their special mission aircraft fleet, Electronic Warfare aircraft (EC-37B), Battlefield Airborne Communications Node aircraft (E-11A), and Maritime Patrol Aircraft (P-8A) on order. Between 2022 and 2029, a total of 12 P-8A and 5 E-11A are expected to be delivered. Such investments in the development of advanced communication and situational awareness systems are expected to accelerate the growth of the market studied.

Furthermore, in March 2022, the Canadian Department of National Defense selected Elbit Systems UK to provide a TORCH-X-based solution as part of the Airspace Coordination Centre Modernization (ASCCM) Project. Under the project, Elbit Systems UK will likely supply a joint-air version of its TORCH-X-based Battle Management Application (BMA) that will provide situational awareness by constantly displaying a local or recognized air picture, thus enabling effective coordination of air assets into complex land and joint battlespace. The system will be operated utilizing Elbit Systems' E-CIXTM open architecture framework that will enable connectivity to the Canadian Armed Forces' legacy applications and tactical datalinks while allowing future integration of new applications in support of the Canadian Armed Forces digital transformation plan. Thus, the growing focus on enhancing defense capabilities and the rising adoption of advanced C4ISR systems drive the growth of the market across the region.

C4ISR Industry Overview

The C4ISR market is fragmented, with many international and regional players supporting the armed forces worldwide. Some of the prominent players in the C4ISR market are Northrop Grumman Corporation, RTX Corporation, L3Harris Technologies, Inc., THALES, and General Dynamics Corporation. The companies are formulating new strategies to expand their presence in various regions and capture new contracts from the armed forces. The market players are actively forming JVs and partnerships with local manufacturers to expand their presence in other regions. In addition to such plans, investments into R&D for developing C4ISR systems that are integrated with technologies like AI and quantum networking are also anticipated to help the companies attract new customers and increase their share in the market in the coming years.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Platform

- 5.1.1 Air

- 5.1.2 Land

- 5.1.3 Sea

- 5.1.4 Space

- 5.2 Purpose

- 5.2.1 Command, Control, Communications, and Computer (C4)

- 5.2.2 Intelligence, Surveillance, and Reconnaissance (ISR)

- 5.2.3 Electronic Warfare (EW)

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 France

- 5.3.2.4 Russia

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Mexico

- 5.3.4.3 Rest of Latin America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Turkey

- 5.3.5.4 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Lockheed Martin Corporation

- 6.2.2 Northrop Grumman Corporation

- 6.2.3 Elbit Systems Ltd

- 6.2.4 BAE Systems PLC

- 6.2.5 Saab AB

- 6.2.6 THALES

- 6.2.7 RTX Corporation

- 6.2.8 L3Harris Technologies, Inc.

- 6.2.9 CACI INTERNATIONAL INC.

- 6.2.10 General Dynamics Corporation

- 6.2.11 Honeywell International Inc.

- 6.2.12 The Boeing Company

- 6.2.13 Leidos

- 6.2.14 Israel Aerospace Industries Ltd.