宇宙ベースC4ISR:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Space-based C4ISR - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1687111

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

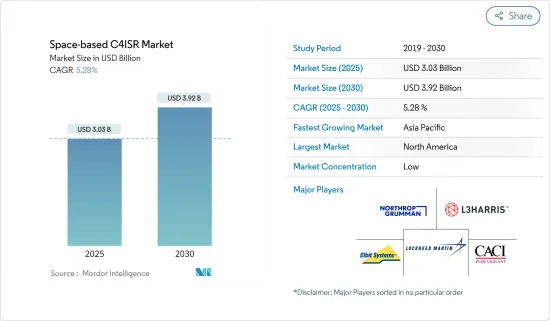

宇宙ベースC4ISRの市場規模は2025年に30億3,000万米ドルと推定され、2030年には39億2,000万米ドルに達すると予測され、予測期間中(2025-2030年)のCAGRは5.28%です。

諜報・監視・偵察(ISR)は、国家の戦略的防衛において極めて重要な役割を果たします。多くの国は、状況認識を強化し、通信速度を向上させ、脅威検出能力を強化するために、宇宙ベースのシステムに注目しています。世界各国は、現在および将来の安全保障上の要求を満たすため、データの収集から発信に至るまで、あらゆる面でISRシステムを活用しています。さらに、多くの国が宇宙ベースの強力な画像情報(IMINT)を武器庫に強化し、宇宙空間での円滑な軍事作戦のためにこれらの能力を積極的に強化しています。

地理空間システムの普及とマイクロエレクトロニクスの進歩は、洗練された宇宙ベースC4ISRシステムの構築に役立っています。これらのシステムは高度な機能を誇ると同時に、関連する研究開発コストを引き下げています。しかし、宇宙ベースC4ISRに対する需要の急増は、サイバーセキュリティや潜在的な宇宙ベース兵器攻撃に関する懸念の高まりをもたらしました。さらに、規制上の制約や技術的な限界は、宇宙ベースC4ISRシステムの設計と進歩に課題をもたらし、今後数年間の市場の成長を阻害する可能性があります。

宇宙ベースC4ISR市場の動向

予測期間中、ISR分野が市場を独占する見込み

宇宙ベースC4ISR市場における諜報・監視・偵察(ISR)能力は、現代の防衛戦略の目となり耳となります。宇宙におけるISR技術には、高度な衛星システム、リモートセンシング、データ分析が含まれ、正確でタイムリーな情報収集、戦略的監視、偵察が可能になります。ハイブリッド・シナリオに移行する戦争の様相の変化は、共同作戦に支えられ、効果的な作戦を可能にする相互運用性を必要とします。

これらの軌道はGEOよりもデータ転送が速いなど、いくつかの利点があるため、いくつかの国がさまざまなISR衛星をLEOやMEO衛星コンステレーションに打ち上げています。加えて、LEO衛星は推進力や電力が少なくて済むため小型化でき、データ遅延も少なくなります。そのため、さまざまな国がISR衛星を宇宙に打ち上げています。例えば、2024年1月、三菱重工業のH2Aロケットが日本のISR衛星を軌道に乗せ、北朝鮮の軍事拠点の動きなどのデータを収集しました。同様に2023年12月、インドはAIを搭載した50機の監視衛星を開発し、捕捉したデータを分析してリアルタイムで最新情報を提供し、インドの国境監視を強化する計画を発表しました。さらに2024年5月、スペースX社のファルコン9ロケットが、情報収集用途の政府版スターリンク衛星を打ち上げました。米国は今後数年間で数百基の衛星を軌道に打ち上げる計画です。

このように、先進的なISRシステムの研究開発、調達のために多くの投資が行われており、市場の成長を牽引する可能性があります。技術の進歩、宇宙支配権獲得競争、軍事衛星への予算配分の増加は、予測期間中にこのセグメントの成長をさらに促進すると予想されます。

アジア太平洋地域が予測期間中に最も高い成長を記録する見込み

アジア太平洋地域のインフラ投資は、宇宙ベースC4ISRシステムの成長を加速させています。中国は、その高度な能力、急増する打ち上げロケット群、強力なBeiDou衛星ナビゲーション・プログラムで際立っています。特筆すべきは、2015年に戦略支援軍を結成した後、中国は48衛星のBeiDouコンステレーションを完成させ、地球同期軌道(GEO)と低軌道(LEO)の通信衛星とISR衛星を強化したことです。これは、特にLEOにおける宇宙能力の拡大と相まって、中国のC4ISRネットワークを強化しています。

一方、インドは軍事通信インフラを大幅に強化しており、運用可能な3基の軍事通信専用衛星と多目的衛星群を誇っています。最近のインド国防省による電気光学衛星の承認で注目されたこれらの資産は、宇宙ベースの情報能力を強化するというインドのコミットメントを強調しています。さらに、ISROは今後5年間で50機の地理情報衛星を打ち上げるという野心的な計画を立てており、部隊の動きを監視し、広大な地形を捉えることができます。

宇宙ベースC4ISR産業の概要

宇宙ベースC4ISR市場は断片化されており、いくつかの国際的・地域的プレーヤーが世界の軍隊からの需要を支えています。同市場における著名なプレイヤーには、Northrop Grumman Corporation、Lockheed Martin Corporation、L3Harris Technologies Inc.、CACI International Inc.、Elbit Systems Ltd.などがいます。

市場のプレーヤーは、地域間のリーチを広げ、軍からの追加契約を確保するために新たな戦略を練っています。新たな地域での足場を固めるため、現地メーカーとの提携や合弁事業も増えています。さらに、特に宇宙ベースC4ISRシステムを進歩させるための研究開発への投資の高まりは、AIや量子ネットワーキングなどの最先端技術と相まって、予測期間中に新たな顧客を誘致し、市場シェアを強化する構えです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- 産業の魅力- ポーターのファイブフォース分析

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 目的

- C4

- ISR

- 地域

- 北米

- 米国

- カナダ

- 欧州

- 英国

- フランス

- ドイツ

- ロシア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 世界のその他の地域

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Elbit Systems Ltd

- General Dynamics Corporation

- Maxar Technologies Ltd

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- BAE Systems PLC

- CACI International Inc.

- Kratos Defense & Security Solutions Inc.

- The Boeing Company

- L3Harris Technologies Inc.

- Defence Research and Development Organisation

- Hanwha Systems Co. Ltd

第7章 市場機会と今後の動向

目次

The Space-based C4ISR Market size is estimated at USD 3.03 billion in 2025, and is expected to reach USD 3.92 billion by 2030, at a CAGR of 5.28% during the forecast period (2025-2030).

Intelligence, surveillance, and reconnaissance (ISR) play a pivotal role in a nation's strategic defense. Many countries are turning to space-based systems to bolster their situational awareness, enhance communication speeds, and fortify their threat detection capabilities. Globally, countries are leveraging ISR systems across the board, from data collection to dissemination, to meet current and future security demands. Furthermore, many nations have bolstered their arsenals with potent space-based image intelligence (IMINT) and are actively enhancing these capabilities for smoother military operations in space.

The rise in geospatial system adoption and advancements in microelectronics have been instrumental in crafting sophisticated space-based C4ISR systems. These systems boast advanced features while simultaneously driving down associated R&D costs. However, the surge in demand for space-based C4ISR has brought about heightened concerns regarding cybersecurity and potential space-based weapon attacks. Additionally, regulatory constraints and technological limitations pose challenges to the design and advancement of space-based C4ISR systems, potentially impeding the market's growth in the coming years.

Space-based C4ISR Market Trends

The ISR Segment is Expected to Dominate the Market During the Forecast Period

Intelligence, surveillance, and reconnaissance (ISR) capabilities in the space-based C4ISR market represent the eyes and ears of modern defense strategies. ISR technologies in space encompass advanced satellite systems, remote sensing, and data analytics, enabling precise and timely intelligence gathering, strategic surveillance, and reconnaissance, which are crucial for informed decision-making in national security. The changing face of warfare moving toward hybrid scenarios will be underpinned by joint operations and require interoperability to allow effective operation.

Several countries are launching various ISR satellites into LEO and MEO satellite constellations as these orbits have several advantages over GEO, such as faster data transfer. In addition, LEO satellites are smaller because they require less propulsion and less power, and the data latency is reduced. So, various countries are launching ISR satellites into space. For instance, in January 2024, Mitsubishi Heavy Industries Limited's H2A rocket carried a Japanese ISR satellite into orbit to gather data on movements at North Korean military sites and for other applications. Similarly, in December 2023, India announced that it plans to develop 50 AI-enabled surveillance satellites to analyze the captured data to provide real-time updates and bolster India's border surveillance. Furthermore, in May 2024, SpaceX's Falcon 9 rocket launched government versions of Starlink satellites for intelligence-gathering applications. The US plans to launch hundreds of these satellites into orbit in the upcoming years.

Thus, many investments are being made to research, develop, and procure advanced ISR systems that may drive the market's growth. Technological advancement, the race to gain space dominance, and increased budget allocations on military satellites are further expected to drive the growth of this segment during the forecast period.

Asia-Pacific is Expected to Register the Highest Growth During the Forecast Period

Infrastructure investments in Asia-Pacific are accelerating the growth of space-based C4ISR systems. China is a standout with its advanced capabilities, a burgeoning fleet of launch vehicles, and a robust BeiDou satellite navigation program. Notably, after forming the Strategic Support Force in 2015, China completed its 48-satellite BeiDou constellation, bolstering its communication and ISR satellites in geosynchronous-earth orbit (GEO) and low-earth orbit (LEO). This, coupled with its expanding space capabilities, especially in LEO, has fortified China's C4ISR network.

Meanwhile, India is significantly enhancing its military communication infrastructure, boasting three operational dedicated military communication satellites and a fleet of dual-purpose ones. These assets, highlighted by the recent approval of an electro-optical satellite by the Indian Ministry of Defense, underscore India's commitment to bolstering its space-based intelligence capabilities. Additionally, ISRO's ambitious plan to launch 50 geo-intelligence satellites over the next five years, capable of monitoring troop movements and capturing vast swathes of terrain, further solidifies the increasing demand for C4ISR systems in the region.

Space-based C4ISR Industry Overview

The space-based C4ISR market is fragmented, with several international and regional players supporting the demand from the global armed forces. Some prominent players in the market are Northrop Grumman Corporation, Lockheed Martin Corporation, L3Harris Technologies Inc., CACI International Inc., and Elbit Systems Ltd.

Market players are crafting fresh strategies to broaden their reach across regions and secure additional contracts from the armed forces. They are increasingly forging partnerships and joint ventures with local manufacturers to bolster their foothold in new territories. Moreover, heightened investments in R&D, particularly for advancing space-based C4ISR systems, coupled with cutting-edge technologies such as AI and quantum networking, are poised to entice new clientele and bolster their market share during the forecast period.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Purpose

- 5.1.1 C4

- 5.1.2 ISR

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.2 Europe

- 5.2.2.1 United Kingdom

- 5.2.2.2 France

- 5.2.2.3 Germany

- 5.2.2.4 Russia

- 5.2.2.5 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Japan

- 5.2.3.4 South Korea

- 5.2.3.5 Rest of Asia-Pacific

- 5.2.4 Rest of the World

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Elbit Systems Ltd

- 6.2.2 General Dynamics Corporation

- 6.2.3 Maxar Technologies Ltd

- 6.2.4 Lockheed Martin Corporation

- 6.2.5 Northrop Grumman Corporation

- 6.2.6 BAE Systems PLC

- 6.2.7 CACI International Inc.

- 6.2.8 Kratos Defense & Security Solutions Inc.

- 6.2.9 The Boeing Company

- 6.2.10 L3Harris Technologies Inc.

- 6.2.11 Defence Research and Development Organisation

- 6.2.12 Hanwha Systems Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日