|

市場調査レポート

商品コード

1694042

エネルギー・電力産業における試験、検査、認証(TIC)-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Testing, Inspection, And Certification (TIC) In The Energy And Power Industry - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| エネルギー・電力産業における試験、検査、認証(TIC)-市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 137 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

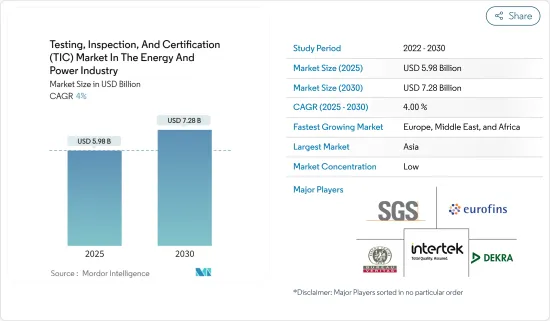

エネルギー電力産業における試験、検査、認証市場は、2025年の59億8,000万米ドルから2030年には72億8,000万米ドルに成長し、予測期間(2025~2030年)のCAGRは4%になると予測されます。

主要ハイライト

- TIC(試験、検査、認証)企業の主要役割は、顧客製品の健康、安全、品質要件を維持することです。さらに、試験、検査、認証ベンダーは、試験、検査、認証サービスに従事し、生産性の向上を支援するとともに、現地メーカーが世界標準に準拠できるよう支援しています。

- 試験、検査、認証(TIC)は、サービス、インフラ、製品が品質と安全基準を満たしていることを保証します。これは、定期的な検査が必要な電力やエネルギーなどの産業では特に重要です。TICサービス市場は、産業の季節性に関係なく安定した成長が見込まれています。

- エネルギー電力産業は世界経済を支えています。エネルギー成長を維持し、環境支援を提供するために、エネルギー電力プロジェクトを効率的かつ効果的に運営する必要性が高まっています。都市化の進展と農村部から都市部への人口移動が、エネルギー電力産業におけるTIC市場開拓の原動力となっています。

- 再生可能エネルギーに対する需要の高まり、政府の厳しい規制、環境汚染を抑制するための環境問題への取り組み、電力部門における先進技術やデジタル技術の採用増加などは、市場の成長を促す主要因のひとつです。欧州の電力エネルギー部門は急速に改革を進めており、デジタル化と相互接続が新たな規範となっています。2050年までに世界初の気候ニュートラル大陸になるという目標は、低炭素の未来を採用するよう産業を後押ししています。TICサービスは、競合、資産の安全性、厳しい環境基準への準拠を可能にします。

- 規制機関や政府による厳しい規制、特にハイエンドの産業機器認証は、エネルギー電力セクタ企業に試験、検査、認証(TIC)サービスのアウトソーシング導入を迫る。また、発電ベンダーは、TICサービスがプライバシーやセキュリティに関するいくつかのリスクをもたらすため、アウトソーシングに消極的可能性があります。したがって、TICサービスの採用は、こうした抑制要因のために多くの労力を要する可能性があります。

- ドイツでは、技術検査機関(TUV)グループを含む多くの民間適合性評価機関が存在します。認定は、顧客が適合性評価を信頼できるようにするものです。認定機関は、適合性評価機関の技術的能力とその客観性を証明します。EUの適合性評価機関は、各国の認定機関が発行する1つの認定を受けるだけでよく、この認定は単一市場全体で認められています。ドイツの認定機関(Deutsche Akkreditierungsstelle GmbH-DAkkS)は、ドイツで最も重要な認定機関です。

- エネルギー電力産業におけるTIC市場に影響を与えるマクロ経済要因は、世界的と地域的な全体的な経済成長です。経済活動の活発化は通常、エネルギープロジェクトへの投資の増加につながり、その結果、コンプライアンス、安全性、信頼性を確保するためのTICサービスへの需要が高まっている

試験、検査、認証(TIC)市場の動向

著しい成長を確認する発電

- 発電部門は、さまざまな産業や日常生活に必要なエネルギーを供給し、世界の経済開発において基本的な役割を果たしています。持続可能で信頼性の高い電力への需要が高まる中、実用的な試験、検査、認証(TIC)サービスが最重要となっています。

- 規制遵守は、発電セグメントにおけるTICサービスの主要な市場の促進要因の一つです。世界各国の政府は、発電施設の安全性、信頼性、環境の持続可能性を確保するために厳しい規制を実施しています。

- これらの規制は、発電所運営者に対して、指定された基準を満たすために包括的な検査、検査、認証を受けることを求めています。厳しい規則に従わない場合、発電事業者は厳しい法的結果、罰則、風評被害を受ける可能性があります。このため、発電所がこうした規制を遵守し、操業を円滑に維持しようとする中で、TICサービスに対する需要が大幅に高まっています。

- 発電部門には複雑な機械、高電圧、危険物が含まれるため、安全性が最優先されます。試験、検査、認証(TIC)サービスは、潜在的な安全リスクを特定し、発電設備が許容される安全基準内で稼働することを保証する上で極めて重要です。これらのサービスには、電気システム、機械部品、火災安全性、放射線被曝などが含まれます。発電セクタにおけるTICサービスの市場需要は、リスクを軽減し、事故を防止し、労働者と周辺地域社会の福利を守る必要性によって牽引されています。

- さらに、発電施設は資本集約的な投資であり、その効率的な運用はエネルギー需要を満たすために極めて重要です。検査、検査、認証サービスは、発電に使用される機器やシステムが要求される品質基準を満たしていることを保証するのに役立ちます。厳格な検査と検査を実施することで、TICサービスは発電インフラにおける欠陥、故障、非効率を特定するのに役立ちます。これにより、発電所のオペレーターは問題を迅速に修正し、パフォーマンスを最適化し、全体的な信頼性を向上させることができます。このように、品質保証と卓越した運用の必要性が、発電セグメントにおけるTICサービスの市場需要を牽引しています。

アジアが最大の市場シェアを占める

- 中国はアジア太平洋で急速に経済成長を遂げている国のひとつであり、TIC(検査・認証)市場の繁栄にとって魅力的な場所となっています。また、製品の安全性や品質に関する消費者の知識が高まることで、エネルギー電力セグメントの機器検査のようなセグメントの成長にも拍車がかかると予想されます。

- CECによると、中国では2023年時点で約2,920ギガワットの発電容量が設置されており、2022年の約3,000ギガワットから増加しています。火力発電の大半は石炭火力であり、中国で最も大きな発電能力を持つエネルギー源です。さらにCECによると、2023年の中国の総電力消費量は約9,220テラワット時でした。これは、消費量が約8,640テラワット時であった2022年と比較して顕著な増加でした。このような電力消費の増加は、同国の研究市場を牽引すると考えられます。

- インドは、アジア太平洋で最も急速に台頭している経済圏のひとつであり、検査市場としては最もダイナミックな市場のひとつです。CEAによると、インドで最もエネルギー容量が大きいのは火力発電で、2023年2月時点で23万6,000メガワット以上の設備容量があります。同国の発電量の約70%は火力発電所によるものです。石炭が電力供給の大半を占め、火力発電所による貢献は86%を超えました。石炭とともに、褐炭、ディーゼル、ガスからも火力発電が行われています。

- COVID-19の第2波が流行する中、ULはインドの太陽光発電(PV)インバータ製造業者向けに検査サービスを開始すると発表しました。ULは、新・再生可能エネルギー省(Ministry of New and Renewable Energy:MNRE)が義務付ける規格の要求事項への対応を支援するため、ベンガルールに施設を拡大しました。この検査所は、国家認定委員会(National Accreditation Board)が検査所・校正機関(NABL)として認定しています。BISは強制登録制度(CRS)のもとで、代表的なモデルの検査に基づいて太陽光発電インバータの検査を実施することを認めています。

- 日本国内での生産量が少ないため、日本政府は常に、安定した発電供給を確保するため、世界的に探査・開発プロジェクトを増やすようエネルギー企業に働きかけてきました。こうした取り組みにより、日本はエネルギーセグメントの資本設備の主要輸出国の1つとなっており、TICサービスの主要導入国の1つとなっています。

- 2023年11月、日本の沖縄電力(9511.T)は、二酸化炭素(CO2)排出量削減を目指し、商用ガス火力発電所で水素の混焼を検査的に開始する新タブ計画を発表しました。沖縄本島南部の吉野浦火力発電所の35メガワット(MW)ユニットで、水素混焼率30%を目指します。水素混焼技術の確立は、再生可能エネルギーの拡大とCO2排出量の削減という2つの目標を達成するための重要な取り組みです。

試験、検査、認証(TIC)産業概要

エネルギー電力産業におけるTIC市場は細分化されており、SGS SA、Eurofins Scientific SE、Bureau Veritas SA、Intertek Group PLC、DEKRA SE、DNV Group ASなどの主要企業が参入しています。調査対象市場の参入企業は、製品提供を強化し、サステイナブル競争優位性を獲得するために、提携や買収などの戦略を採用しています。

- 2023年9月-Intertekはフランスの独立系検査・エンジニアリングスペシャリストであるEmitech Groupと提携。EN 17025とEN 17065の認定を受け、ノーティファイドボディ、CBスキームに参加するEmitech Groupは、トレーニング、検査、エンジニアリングの専門知識を、多様なエンドユーザー産業で活動する組織に提供しています。この戦略的提携により、Emitech GroupとIntertekの欧州の顧客に先進的な設備と対象範囲の拡大がもたらされます。

- 2023年6月-Applus+は、フランスを拠点とする著名な材料検査・研究開発技術パートナーであるRescollの全株式を取得。レスコールの従業員数は約170名、年間売上高は2,100万ユーロを超えます。その設備の整ったラボ、専門家、多様な能力は、エネルギー、医療、航空宇宙、産業セグメントの開発をサポートすると主張しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- COVID-19後遺症とその他のマクロ経済要因が市場に与える影響

- 産業の魅力-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 今後需要が見込まれる主要規格/認証とサービスタイプ

第5章 市場力学

- 市場の促進要因

- 製品の安全性と環境保護を確保するための政府規制と義務化

- エネルギー効率化プロセスへの投資の増加とエネルギー電力セグメントにおけるスマートグリッドの利用の増加

- 市場抑制要因

- 多様な規格が存在するため、非インシュアント企業がコンプライアンスを確保するのが困難

第6章 市場セグメンテーション

- サービスタイプ別

- 検査

- 認証

- 地域別

- 中国

- 米国

- インド

- 日本

- ブラジル

- カナダ

- 韓国

- ドイツ

- フランス

- サウジアラビア

- 用途別

- 発電

- 貯蔵

- 流通・販売

第7章 競合情勢

- 企業プロファイル

- DNV Group AS

- SGS SA

- Bureau Veritas SA

- Applus Services SA

- Intertek Group PLC

- DEKRA SE

- Eurofins Scientific SE

- Advanced Technology Group,spol.s r.o.

- TUV SUD AG

- Element Materials Technology Group Limited

第8章 ベンダーの市場シェア分析

第9章 市場の将来展望

The Testing, Inspection, And Certification Market In The Energy And Power Industry is expected to grow from USD 5.98 billion in 2025 to USD 7.28 billion by 2030, at a CAGR of 4% during the forecast period (2025-2030).

Key Highlights

- The primary role of TIC (testing, inspection, and certification) companies is to sustain the health, safety, and quality requirements of their client's products. Moreover, testing, inspection, and certification vendors are engaged in verification, inspection, testing, and certification services to help improve productivity and also help local manufacturers comply with global standards.

- Testing, inspection, and certification (TIC) ensure that services, infrastructure, and products meet quality and safety standards. This is especially crucial in industries like power and energy, where regular inspections are required. The TIC services market is expected to grow consistently regardless of industrial seasonality.

- The energy and power industry feeds the world's economy. There is a rising need to efficiently and effectively operate energy and power projects to sustain energy growth and provide environmental support. Increasing urbanization and people migrating from rural areas to urban areas are driving the development of the TIC market in the energy and power industry.

- The growing demand for renewable energy, the government's stringent regulation, environmental concerns initiative for controlling environmental pollution and increasing adoption of advanced and digital technologies in the power sector are some of the major factors driving the market's growth. The European power and energy sector is rapidly reinventing itself, where digitalization and interconnection are the new norms. The goal of becoming the world's first climate-neutral continent by 2050 is pushing the industry to adopt a low-carbon future. TIC services enable the competitiveness and asset's safety and compliance with stringent environmental standards.

- Stringent regulations from regulatory bodies and government, especially in high-end industrial equipment certification, compel energy and power sector companies to adopt outsourced testing, inspection, and certification (TIC) services. The power generation vendors may also be reluctant to outsource TIC services as they pose several risks related to privacy and security, as it involves sharing confidential supply chain information with third parties. Hence, adopting TIC services might take a lot of work due to these restraining factors.

- In Germany, there are many private conformity assessment bodies, including the group of Technical Inspection Agencies (TUV). Accreditation ensures that customers can trust in conformity assessment. Accreditation bodies attest to the technical competence of conformity assessment bodies and their objectivity. Conformity bodies in the EU require just one accreditation issued by their national accreditation body, which is recognized across the single market. The German Accreditation Body (Deutsche Akkreditierungsstelle GmbH - DAkkS) is the foremost accreditation body in Germany.

- The macroeconomic factors impacting the TIC market in the energy and power industry is the overall economic growth, both globally and regionally, as it plays a significant role in driving the demand for energy and power infrastructure, products, and services. Higher economic activity typically leads to increased investment in energy projects, which, in turn, drives the demand for TIC services to ensure compliance, safety, and reliability.

Testing, Inspection, and Certification (TIC) Market Trends

Power Generation to Witness Significant Growth

- The power generation sector plays a fundamental role in global economic development, providing the energy required for various industries and everyday life. With the rising demand for sustainable and reliable power, practical testing, inspection, and certification (TIC) services have become paramount.

- Regulatory compliance is one of the primary market drivers for TIC services in the power generation sector. Governments globally have implemented stringent regulations to ensure power generation facilities' safety, reliability, and environmental sustainability.

- These regulations require power plant operators to undergo comprehensive testing, inspection, and certification to meet the specified standards. Failure to comply with the stringent rules can result in severe legal consequences, penalties, and reputational damage for power generation companies. The demand for TIC services has thus increased significantly as power plants seek to comply with these regulations and maintain their operations smoothly.

- The power generation sector involves complex machinery, high voltages, and hazardous materials, making safety a top priority. Testing, inspection, and certification (TIC) services are crucial in identifying potential safety risks and ensuring that power generation facilities operate within acceptable safety standards. These services include electrical systems, mechanical components, fire safety, radiation exposure, and more. The market demand for TIC services in the power generation sector is driven by the need to mitigate risks, prevent accidents, and safeguard the well-being of workers and surrounding communities.

- Moreover, power generation facilities are capital-intensive investments, and their efficient operation is crucial for meeting energy demands. Testing, inspection, and certification services help ensure that the equipment and systems used in power generation meet the required quality standards. By conducting rigorous testing and inspections, TIC services help identify defects, malfunctions, or inefficiencies in the power generation infrastructure. This enables power plant operators to rectify issues promptly, optimize performance, and improve overall reliability. The need for quality assurance and operational excellence thus drives the market demand for TIC services in the power generation sector.

Asia Holds the Largest Market Share

- China is among the rapidly growing economies in the Asia-Pacific area, making it an appealing location for the TIC (testing, inspection, and certification) market to thrive. Increasing consumer knowledge about product safety and quality is also anticipated to spur growth in sectors like equipment testing in the energy and power field.

- According to CEC, approximately 2,920 gigawatts of electricity generation capacity had been installed in China as of 2023, up from some 3,000 gigawatts in 2022. Most thermal power is coal-based and is the energy source with the country's most significant power generation capacity. Moreover, according to CEC, China had a total electricity consumption of around 9,220 terawatt hours in 2023. This was a notable increase compared to 2022, when consumption amounted to approximately 8,640 terawatt hours. This increase in electricity consumption will drive the studied market in the country.

- India is one of the most dynamic markets for testing and inspection in the Asia-Pacific region, as it is one of the fastest emerging economies in the region. According to CEA, India's highest energy capacity came from thermal energy, amounting to an installed capacity of over 236 thousand megawatts as of February 2023. Approximately 70% of the country's electricity generation was from thermal power plants. Coal dominated power supply with a contribution of over 86% through thermal power plants. Along with coal, thermal power is generated from lignite, diesel, and gas.

- During the second wave of the COVID-19 pandemic, UL announced the launch of testing services for India's solar photovoltaic (PV) inverter manufacturers. UL has expanded its facility in Bengaluru to help manufacturers comply with the requirements of the standards mandated by the Ministry of New and Renewable Energy (MNRE). The National Accreditation Board accredits the laboratory for Testing and Calibration Laboratories (NABL). The BIS recognizes it under the Compulsory Registration Scheme (CRS) to conduct testing of solar PV inverters based on testing of representative models.

- Owing to low domestic production in the country, the Japanese government always encouraged its energy companies to increase exploration and development projects globally to secure a stable power generation supply. These initiatives make Japan one of the major exporters of energy-sector capital equipment, making it one of the primary adopters of TIC services.

- In November 2023, Japan's Okinawa Electric Power (9511.T) opened new tab plans to start co-firing hydrogen on a trial basis at a commercial gas-fired power plant in a bid to reduce carbon dioxide (CO2) emissions. The utility aims to achieve a hydrogen co-firing rate of 30% at the 35 megawatts (MW) unit of its Yoshinoura thermal power station in the southern island of Okinawa. Establishing hydrogen co-firing technology is a critical initiative to help achieve two goals: expanding renewable energy and slashing CO2 emissions.

Testing, Inspection, and Certification (TIC) Industry Overview

The TIC market in the energy and power industry is fragmented, with major players like SGS SA, Eurofins Scientific SE, Bureau Veritas SA, Intertek Group PLC, DEKRA SE, and DNV Group AS. Players in the market studied are adopting strategies such as partnerships and acquisitions to enhance product offerings and gain sustainable competitive advantage.

- September 2023 - Intertek partnered with Emitech Group, the French independent testing and engineering specialist. Accredited to EN 17025 and EN 17065, a notified body, and a participant in the CB scheme, the Emitech Group offers its expertise in training, testing, and engineering to organizations operating across a diverse range of end-user industries. This strategic alliance will bring advanced facilities and expanded coverage to Emitech Group and Intertek's European customers.

- June 2023 - Applus+ acquired the entire share capital of Rescoll, a prominent materials testing and research and development technological partner based in France. Rescoll has approximately 170 employees and an annual revenue of over EUR 21 million. Its well-equipped laboratories, experts, and diverse capabilities are claimed to support the development of the energy, medical, aerospace, and industry sectors.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Key Standards/Certifications and Type of Services that Might be in Demand in the Future

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Government Regulations and Mandates to Ensure Product Safety and Environmental Protection

- 5.1.2 Rising Investments in Energy Efficiency Process and Increasing Usage of Smart Grids in the Energy and Power Sector

- 5.2 Market Restraints

- 5.2.1 The Presence of Diverse Standards Makes It Complicated for Non-incumbents to Ensure Compliance

6 MARKET SEGMENTATION

- 6.1 By Service Type

- 6.1.1 Testing and Inspection

- 6.1.2 Certification

- 6.2 By Geography

- 6.2.1 China

- 6.2.2 United States

- 6.2.3 India

- 6.2.4 Japan

- 6.2.5 Brazil

- 6.2.6 Canada

- 6.2.7 South Korea

- 6.2.8 Germany

- 6.2.9 France

- 6.2.10 Saudi Arabia

- 6.3 By Application

- 6.3.1 Power Generation

- 6.3.2 Storage

- 6.3.3 Distribution and Sales

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 DNV Group AS

- 7.1.2 SGS SA

- 7.1.3 Bureau Veritas SA

- 7.1.4 Applus Services SA

- 7.1.5 Intertek Group PLC

- 7.1.6 DEKRA SE

- 7.1.7 Eurofins Scientific SE

- 7.1.8 Advanced Technology Group,spol.s r.o.

- 7.1.9 TUV SUD AG

- 7.1.10 Element Materials Technology Group Limited