|

市場調査レポート

商品コード

1693691

インドのコンクリート混和剤:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)India Concrete Admixtures - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| インドのコンクリート混和剤:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 207 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

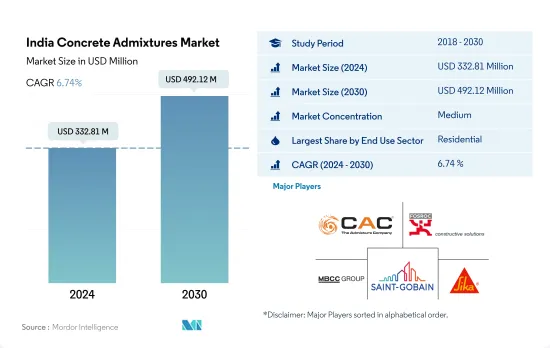

インドのコンクリート混和剤市場規模は2024年に3億3,281万米ドルと推定され、2030年には4億9,212万米ドルに達すると予測され、予測期間(2024~2030年)のCAGRは6.74%で成長すると予測されます。

外国投資の誘致と経済成長の推進に注力するインドが市場の成長に影響を与える

- コンクリート混和剤市場は2022年に大幅に急増し、2021年の値を8.15%上回りました。この成長は主に全国的な建設活動の活発化によって推進されました。2023年にはコンクリート混和剤の需要が5%増加すると予測され、インフラと商業セクタがこの急増の先陣を切りました。

- コンクリートがインドの大半の住宅建築物の基礎材料であることを考えれば、2022年にコンクリート混和剤の需要と金額が住宅部門を支配したことは驚くべきことではないです。この需要にさらに拍車をかけているのが、インドの都市人口の一貫した増加です。特に、2022年と2021年の都市人口は、前年比でそれぞれ2.1%と2.2%増加しました。

- 2022年には、インフラ部門がコンクリート混和剤市場の第2位の貢献者に浮上したが、これはインドがインフラ開拓に力を入れていることの証です。この重点化はコンクリート混和剤需要の顕著な急増につながっています。例えば、2022年のインフラ支出は前年比3.09%増となり、2019~2023年にかけて約1兆4,000億米ドルをインフラプロジェクトに投資するという国の計画と一致しています。

- 新しい商業ビルの建設は、2023~2030年の予測期間中にCAGR 5.26%を記録する展望です。この勢いは、インド経済の急成長と外資系企業からの投資流入が予想されることに起因しています。商業セグメントでは、予測期間中のCAGRは8.04%と予測され、成長はさらに顕著になると予想されます。

インドのコンクリート混和剤市場動向

インドのグレードAオフィス市場は、2030年までに12億平方フィートに達すると予想され、商業建築部門の需要を牽引する可能性が高いです。

- 2022年、インドの新規商業床面積は2021年比で6.2%の数量増となりました。小売セクタ、特に上位7都市(デリーNCR、バンガロール、ハイデラバード、ムンバイ、プネー、チェンナイ、コルカタ)では、旺盛な需要が見られ、モールスペースは260万平方フィートを超え、2021年から27%増加しました。2023年を展望すると、外国直接投資(FDI)の急増が新たなオフィス、小売店、その他の施設の必要性を煽り、このセクタの新規床面積は3,800万平方フィート急増すると予想されます。特に、2023年の建設開発へのFDI資本流入額は9,600万米ドルに達すると予測されています。

- 2020年、インドの商業施設の新設床面積は2019年比で68.3%減少しました。この減少は主に政府による全国的な封鎖によるもので、進行中のプロジェクトが中断し、サプライチェーンが緊張し、労働力の確保に影響を与えました。しかし、2021年に規制が緩和されると、新規床面積が約5億2,600万平方フィート急増し、大幅な回復が見られました。さらに、2021年にはグリーンビルディングへの取り組みが顕著に増加し、商業プロジェクトの約55%が持続可能性を取り入れ、このセグメントの需要をさらに押し上げました。

- 2030年を展望すると、インドの商業施設の新設床面積は3億5,800万平方フィートに達すると予測され、2023年から大幅に急増します。この急増により、ショッピングモール、オフィススペース、その他の商業施設に対する需要が高まっています。例えば、上位7都市におけるインドのグレードAオフィス市場は、2026年までに10億平方フィートに拡大し、2030年までにさらに12億平方フィートに拡大します。その結果、同国の商業施設の新設床面積は、予測期間中にCAGR 5.26%という堅調な伸びを記録する展望です。

住宅需要の増加と不動産セクタの拡大が住宅セクタの需要を押し上げる

- 2022年、インドの住宅床面積は前年を上回る9.4%の伸びを示しました。国内の住宅需要は急増し、上位7都市(デリーNCR、バンガロール、ハイデラバード、ムンバイ、プネー、チェンナイ、コルカタ)の合計で約40万2,000戸が新たに建設され、2021年から44%増加しました。2023年第1四半期には、これらの都市の住宅販売戸数は11.4万戸に達し、前年から9.95万戸以上も急増しました。その結果、インドの住宅新築床面積は2023年には2022年比で約7,100万平方フィート拡大すると予測されました。

- 2020年、インドの住宅セクタは後退に直面し、新設床面積は前年比6.25%減少しました。この減少は、全国的な封鎖、サプライチェーンの混乱、労働力不足、建設生産性の低下、外国投資の落ち込みが原因です。しかし、2021年にはインドの住宅不動産市場は回復し、上位7都市で約16万3,000戸の新築住宅が増加しました。この急増により、2021年の住宅セクタの新設床面積は2020年比で約6億4,900万平方フィートと大幅に増加しました。

- 今後、インドの住宅セクタは、2023~2030年にかけて数量ベースで2.95%のCAGRを示す展望です。この成長は、持続的な住宅需要、投資の増加、有利な政府施策によるものです。特に、2030年までにインドの人口の40%以上が都市部に居住するようになり、手頃な価格の住宅が約2,500万戸追加される需要が高まると予測されています。さらに、2030年までに住宅不動産市場は主要都市で150万戸に達すると予想されており、このセグメントの需要をさらに促進しています。

インドのコンクリート混和剤産業概要

インドのコンクリート混和剤市場は適度に統合されており、上位5社で52.50%を占めています。この市場の主要企業は、CAC Admixtures、Fosroc、Inc.、MBCC Group、Saint-Gobain、Sika AGなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 最終用途セグメントの動向

- 商業

- 産業・施設

- インフラ

- 住宅用

- 主要インフラプロジェクト(現在と発表済み)

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 最終用途セグメント

- 商業

- 産業・施設

- インフラ

- 住宅用

- サブプロダクト

- 促進剤

- 空気混入混和剤

- 高範囲減水剤(超可塑剤)

- リターダー

- 収縮低減混和剤

- 粘度調整剤

- 減水剤(可塑剤)

- その他

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- CAC Admixtures

- Chembond Chemicals Limited

- Don Construction Products Ltd.

- ECMAS Group

- Fosroc, Inc.

- MAPEI S.p.A.

- MBCC Group

- MC-Bauchemie

- Saint-Gobain

- Sika AG

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク(産業魅力度分析)

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 93446

The India Concrete Admixtures Market size is estimated at 332.81 million USD in 2024, and is expected to reach 492.12 million USD by 2030, growing at a CAGR of 6.74% during the forecast period (2024-2030).

India's focus on attracting foreign investment and propelling economic growth to influence the market's growth

- The market for concrete admixtures witnessed a significant surge in 2022, surpassing its 2021 value by 8.15%. This growth was primarily propelled by a nationwide uptick in construction activities. A 5% increase in the demand for concrete admixtures was projected for 2023, with the infrastructure and commercial sectors spearheading this surge.

- Given that concrete is a cornerstone material in the majority of residential buildings in India, it comes as no surprise that the residential segment dominated the demand and value for concrete admixtures in 2022. This demand is further fueled by India's consistently rising urban population. Notably, the urban population in 2022 and 2021 saw a 2.1% and 2.2% increase, respectively, compared to the preceding years.

- In 2022, the infrastructure sector emerged as the second-largest contributor to the concrete admixtures market, a testament to India's heightened focus on infrastructure development. This emphasis has translated into a notable surge in the demand for concrete admixtures. For instance, in 2022, infrastructure spending saw a 3.09% increase from the previous year, aligning with the nation's plan to invest approximately USD 1.4 trillion in infrastructure projects spanning 2019-2023.

- The construction of new commercial buildings is poised to witness a CAGR of 5.26% during the forecast period of 2023-2030. This momentum can be attributed to India's burgeoning economy and the anticipated influx of investments from foreign companies. Within the commercial segment, the growth is expected to be even more pronounced, with a projected CAGR of 8.04% during the forecast period.

India Concrete Admixtures Market Trends

India's Grade A office market is expected to reach 1.2 billion sq. ft by 2030 and is likely to drive the demand for the commercial construction sector

- In 2022, India's new commercial floor area saw a 6.2% volume growth compared to 2021. The retail sector, particularly in the top seven cities (Delhi NCR, Bangalore, Hyderabad, Mumbai, Pune, Chennai, and Kolkata), witnessed robust demand, adding over 2.6 million sq. ft of mall space, a 27% increase from 2021. Looking ahead to 2023, the sector's new floor area is expected to surge by 38 million sq. ft, driven by a surge in foreign direct investment (FDI) fueling the need for new offices, retail outlets, and other facilities. Notably, the FDI equity inflow for construction development in 2023 was projected to hit USD 96 million.

- In 2020, India's commercial new floor area plummeted by 68.3% in volume compared to 2019. This decline was primarily due to a nationwide lockdown imposed by the government, which disrupted ongoing projects, strained supply chains, and impacted labor availability. However, as restrictions eased in 2021, the country witnessed a significant rebound, with the new floor area surging by approximately 526 million sq. ft. Additionally, 2021 saw a notable uptick in green building initiatives, with around 55% of commercial projects embracing sustainability, further bolstering the demand for the sector.

- Looking ahead to 2030, India's commercial new floor area is projected to hit 358 million sq. ft, a significant jump from 2023. This surge drives a growing appetite for shopping malls, office spaces, and other commercial facilities. For instance, India's Grade A office market in the top seven cities is set to expand to 1 billion sq. ft by 2026 and further to 1.2 billion sq. ft by 2030. Consequently, the country's commercial new floor area is poised to witness a robust CAGR of 5.26% during the forecast period.

Rise in demand for housing units and increasing real estate sector to boost residential sector demand

- In 2022, India witnessed a 9.4% growth in residential floor area, outpacing the previous year. The demand for housing in the country surged, with the top seven cities (Delhi NCR, Bangalore, Hyderabad, Mumbai, Pune, Chennai, and Kolkata) collectively adding approximately 402,000 new units, marking a 44% increase from 2021. In Q1 2023, housing sales in these cities reached 1.14 lakh units, a staggering jump of over 99,500 units from the previous year. Consequently, it was projected that the residential new floor area in India would expand by approximately 71 million sq. ft in 2023 compared to 2022.

- In 2020, the residential sector in India faced a setback, witnessing a 6.25% decline in new floor area compared to the previous year. This decline was attributed to the nationwide lockdown, disruptions in the supply chain, labor shortages, reduced construction productivity, and a dip in foreign investments. However, in 2021, the Indian residential real estate market rebounded, adding around 163,000 new residential units across the top seven cities. This surge translated into a significant increase of about 649 million sq. ft in the residential sector's new floor area in 2021 compared to 2020.

- Looking ahead, the residential sector in India is poised to exhibit a CAGR of 2.95% in terms of volume from 2023 to 2030. This growth can be attributed to sustained housing demand, increased investments, and favorable government policies. Notably, by 2030, it is projected that over 40% of India's population will reside in urban areas, driving a demand for approximately 25 million additional affordable housing units. Furthermore, by 2030, the residential real estate market is expected to hit 1.5 million units in key cities, further fueling the demand in the sector.

India Concrete Admixtures Industry Overview

The India Concrete Admixtures Market is moderately consolidated, with the top five companies occupying 52.50%. The major players in this market are CAC Admixtures, Fosroc, Inc., MBCC Group, Saint-Gobain and Sika AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End Use Sector Trends

- 4.1.1 Commercial

- 4.1.2 Industrial and Institutional

- 4.1.3 Infrastructure

- 4.1.4 Residential

- 4.2 Major Infrastructure Projects (current And Announced)

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size, forecasts up to 2030 and analysis of growth prospects.)

- 5.1 End Use Sector

- 5.1.1 Commercial

- 5.1.2 Industrial and Institutional

- 5.1.3 Infrastructure

- 5.1.4 Residential

- 5.2 Sub Product

- 5.2.1 Accelerator

- 5.2.2 Air Entraining Admixture

- 5.2.3 High Range Water Reducer (Super Plasticizer)

- 5.2.4 Retarder

- 5.2.5 Shrinkage Reducing Admixture

- 5.2.6 Viscosity Modifier

- 5.2.7 Water Reducer (Plasticizer)

- 5.2.8 Other Types

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 CAC Admixtures

- 6.4.2 Chembond Chemicals Limited

- 6.4.3 Don Construction Products Ltd.

- 6.4.4 ECMAS Group

- 6.4.5 Fosroc, Inc.

- 6.4.6 MAPEI S.p.A.

- 6.4.7 MBCC Group

- 6.4.8 MC-Bauchemie

- 6.4.9 Saint-Gobain

- 6.4.10 Sika AG

7 KEY STRATEGIC QUESTIONS FOR CONCRETE, MORTARS AND CONSTRUCTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms