南米の乗用車:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

South America Passenger Cars - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 272 Pages

- 納期

- 2~3営業日

- 商品コード

- 1693628

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

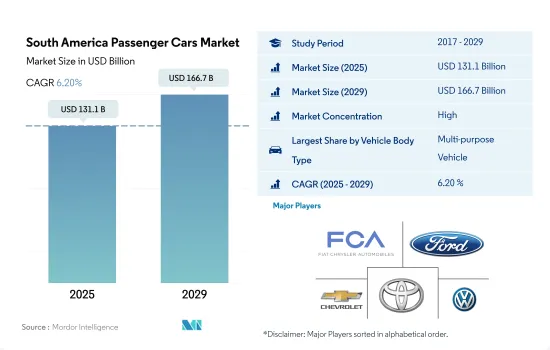

南米の乗用車市場規模は2025年に1,311億米ドルと推定され、2029年には1,667億米ドルに達すると予測され、予測期間(2025-2029年)のCAGRは6.20%で成長すると予測されます。

南米の乗用車市場は、経済的要因、消費者の嗜好、より持続可能な輸送ソリューションへのシフトによって大きな変化を遂げつつあります。

- 南米の自動車産業は、アジア太平洋諸国と比較して低い自動車保有率や可処分所得の上昇の速さなどの要因によって、大きな成長を遂げようとしています。特筆すべきは、南米における電気自動車(EV)の需要が、排出ガス削減や将来のエネルギー需要への懸念に後押しされて増加傾向にあることです。特にブラジルのEV需要の急増は注目に値し、複数の外資系自動車メーカーが同地域に生産施設を設立しています。

- COVID-19の大流行は消費者の購買力に影響を与え、原油価格の顕著な下落につながり、その後ガソリン・コストが低下しました。このガソリン価格の下落により、従来型の内燃機関車(ICE)がより手頃な価格になる可能性があるが、ほとんどの車両クラスで、総合的な所有コストの面ではEVが依然として優位性を保っています。しかし、この優位性の程度はさまざまで、販売に影響を与える可能性があります。

- 南米では持続可能な燃料へのシフトが顕著で、サトウキビ由来のエタノールが有力な選択肢として浮上しています。このバイオ燃料は、ガソリンやディーゼル燃料に比べ最大90%低い排出量を誇る。ブラジルが持続可能な燃料を採用するようになっていることは、この地域市場の形成に極めて重要な役割を果たしています。もう一つの重要な推進力は、自動車産業における再生可能エネルギーの消費拡大です。業界が持続可能性を重視する中、南米では自動車の電動化に関する研究が進んでおり、有望視されています。同地域の堅調な市場成長の可能性から投資拠点としての魅力があることから、経済的利益と市場強化の両方に大きな機会があります。

南米の乗用車市場動向

需要の急増と政府のインセンティブが南米の電気自動車市場を後押し

- 南米のブラジルやアルゼンチンといった国々は、自動車市場において大きな可能性を示しています。南米の自動車産業は近年著しい成長を遂げています。特にこの地域では、乗用車セグメントを中心に電気自動車(EV)の需要が高まっています。この急増は、意識の高まり、環境問題への関心の高まり、EV導入を促進する政府の取り組みといった要因によるものです。実際、同地域のEV販売台数は顕著な伸びを示し、2022年には2021年比で17.95%増加しました。

- 多様な市場を持つ南米では、電気自動車の急増が見込まれています。特にブラジルは、再生可能エネルギーによる発電を重視し、EVバッテリー開発に不可欠なニオブとリチウムの埋蔵量が豊富なことから、電気バスへのシフトを視野に入れています。2022年12月、サンパウロはディーゼルバスの購入を禁止し、2024年末までに2,600台の電気バスを導入する計画を発表しました。他の南米諸国でも同様の動向が見られ、2024年から2030年にかけて自動車の電動化が進むと予想されます。

- 南米各国の政府政策とインセンティブ・プログラムは、同地域における車両電化の重要な推進力となります。例えば、税制上の優遇措置は極めて重要な役割を果たしています。例えばコロンビア政府は、2030年までに60万台のEVを走らせるという野心的な目標を掲げ、インセンティブと補助金を活用して二酸化炭素排出量の削減に取り組んでいます。他の南米諸国でも同様の取り組みが見込まれており、EVの販売は2024年から2030年にかけて急増すると予想されます。

南米の乗用車産業の概要

南米の乗用車市場はかなり統合されており、上位5社で65.90%を占めています。この市場の主要企業は以下の通り。 Fiat Chrysler Automobiles N.V, Ford Motor Company, GM Motor(Chevrolet), Toyota Motor Corporation and Volkswagen AG(アルファベット順)

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 人口

- 一人当たりGDP

- 自動車購入のための消費者支出(cvp)

- インフレ率

- 自動車ローン金利

- シェアライド

- 電化の影響

- EV充電ステーション

- バッテリーパック価格

- Xev新モデル発表

- 中古車販売

- 燃料価格

- OEM生産統計

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 車両構成

- 乗用車

- ハッチバック

- 多目的車

- セダン

- SUV

- 乗用車

- 推進タイプ

- ハイブリッド車と電気自動車

- 燃料カテゴリー別

- BEV

- FCEV

- HEV

- PHEV

- ICE

- 燃料カテゴリー別

- ディーゼル

- ガソリン

- LPG

- ハイブリッド車と電気自動車

- 国名

- アルゼンチン

- ブラジル

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Fiat Chrysler Automobiles N.V

- Ford Motor Company

- GM Motor(Chevrolet)

- Hyundai Motor Company

- Kia Corporation

- Nissan Motor Co. Ltd.

- Renault do Brasil S/A

- Stellantis N.V.

- Toyota Motor Corporation

- Volkswagen AG

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

The South America Passenger Cars Market size is estimated at 131.1 billion USD in 2025, and is expected to reach 166.7 billion USD by 2029, growing at a CAGR of 6.20% during the forecast period (2025-2029).

The South American passenger cars market is undergoing significant changes driven by economic factors, consumer preferences, and a shift toward more sustainable transportation solutions

- The automotive industry in South America is poised for significant growth, driven by factors such as low car ownership rates and a faster rise in disposable incomes compared to Asia-Pacific countries. Notably, the demand for electric vehicles (EVs) in South America has been on the rise, fueled by concerns about emissions reduction and future energy needs. Brazil's surging demand for EVs is particularly noteworthy, attracting several foreign automakers to set up production facilities in the region.

- The COVID-19 pandemic impacted consumer purchasing power, leading to a notable drop in oil prices and subsequently reducing gasoline costs. While this decline in gas prices may make conventional internal combustion engine (ICE) vehicles more affordable, EVs still hold an advantage in terms of overall ownership costs across most vehicle classes. However, the extent of this advantage may vary, potentially influencing sales.

- South America has seen a notable shift toward sustainable fuel options, with ethanol derived from sugarcane emerging as a prominent choice. This biofuel boasts emissions up to 90% lower than gasoline or diesel equivalents. Brazil's increasing adoption of sustainable fuels has played a pivotal role in shaping the regional market. Another significant driver is the growing consumption of renewable energy in the automotive industry. As the industry emphasizes sustainability, the ongoing research into automotive electrification in South America holds promise. Given the region's attractiveness as an investment hub due to its robust market growth potential, there are significant opportunities for both financial gains and market enhancements.

South America Passenger Cars Market Trends

Surging demand and government incentives propel South America's electric vehicle market

- Countries like Brazil and Argentina in South America show significant potential in the automobile market. The South American vehicle industry has witnessed notable growth in recent years. Notably, the region has seen a rising demand for electric vehicles (EVs), especially in the passenger car segment. This surge can be attributed to factors like heightened awareness, growing environmental concerns, and governmental initiatives promoting EV adoption. In fact, EV sales in the region saw a notable increase, growing by 17.95% in 2022 compared to 2021.

- South America, with its diverse markets, is poised for a surge in electric vehicles. Brazil, in particular, is eyeing a shift toward electric buses, driven by its focus on renewable power generation and its abundant reserves of niobium and lithium, crucial for EV battery development. A significant move in this direction came in December 2022 when Sao Paulo banned diesel bus purchases and announced plans to deploy 2600 electric buses by 2024-end. Similar trends in other South American nations are expected to drive vehicle electrification from 2024 to 2030.

- Government policies and incentive programs across South American nations are set to be key drivers for vehicle electrification in the region. Tax benefits, for instance, are playing a pivotal role. Colombia's government, for instance, is leveraging incentives and subsidies with an ambitious target of putting 600,000 EVs on its roads by 2030, aiming to tackle carbon emissions. With similar initiatives anticipated in other South American countries, the sales of EVs are expected to witness a surge from 2024 to 2030.

South America Passenger Cars Industry Overview

The South America Passenger Cars Market is fairly consolidated, with the top five companies occupying 65.90%. The major players in this market are Fiat Chrysler Automobiles N.V, Ford Motor Company, GM Motor (Chevrolet), Toyota Motor Corporation and Volkswagen AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Population

- 4.2 GDP Per Capita

- 4.3 Consumer Spending For Vehicle Purchase (cvp)

- 4.4 Inflation

- 4.5 Interest Rate For Auto Loans

- 4.6 Shared Rides

- 4.7 Impact Of Electrification

- 4.8 EV Charging Station

- 4.9 Battery Pack Price

- 4.10 New Xev Models Announced

- 4.11 Used Car Sales

- 4.12 Fuel Price

- 4.13 Oem-wise Production Statistics

- 4.14 Regulatory Framework

- 4.15 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Vehicle Configuration

- 5.1.1 Passenger Cars

- 5.1.1.1 Hatchback

- 5.1.1.2 Multi-purpose Vehicle

- 5.1.1.3 Sedan

- 5.1.1.4 Sports Utility Vehicle

- 5.1.1 Passenger Cars

- 5.2 Propulsion Type

- 5.2.1 Hybrid and Electric Vehicles

- 5.2.1.1 By Fuel Category

- 5.2.1.1.1 BEV

- 5.2.1.1.2 FCEV

- 5.2.1.1.3 HEV

- 5.2.1.1.4 PHEV

- 5.2.2 ICE

- 5.2.2.1 By Fuel Category

- 5.2.2.1.1 Diesel

- 5.2.2.1.2 Gasoline

- 5.2.2.1.3 LPG

- 5.2.1 Hybrid and Electric Vehicles

- 5.3 Country

- 5.3.1 Argentina

- 5.3.2 Brazil

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Fiat Chrysler Automobiles N.V

- 6.4.2 Ford Motor Company

- 6.4.3 GM Motor (Chevrolet)

- 6.4.4 Hyundai Motor Company

- 6.4.5 Kia Corporation

- 6.4.6 Nissan Motor Co. Ltd.

- 6.4.7 Renault do Brasil S/A

- 6.4.8 Stellantis N.V.

- 6.4.9 Toyota Motor Corporation

- 6.4.10 Volkswagen AG

7 KEY STRATEGIC QUESTIONS FOR VEHICLES CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 272 Pages

- 納期

- 2~3営業日