欧州の保証管理システム:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Europe Warranty Management System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 108 Pages

- 納期

- 2~3営業日

- 商品コード

- 1693554

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

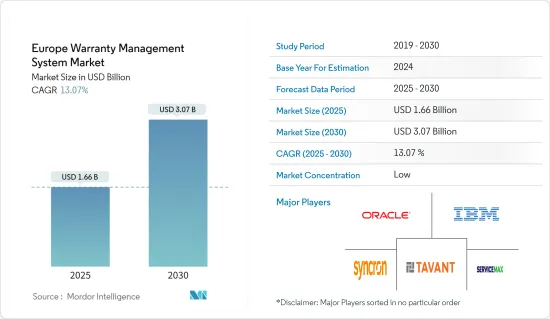

欧州の保証管理システム市場規模は2025年に16億6,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは13.07%で、2030年には30億7,000万米ドルに達すると予測されます。

主なハイライト

- あらゆるサービス事業において重要なのは保証管理です。顧客資産の保証範囲とデータを表示し、アクセスし、自動的に追跡する能力は重要です。保証管理によって、企業は売上損失や顧客の不興を買うことがないです。

- 保証管理システムは、保証クレーム処理とインストールベースの資産追跡を自動化することにより、サービス事業者が保証、クレーム、資産を設計、管理、追跡、処理することを可能にします。革新的な保証管理システム(WMS)は、AIや機械学習機能と連携して顧客満足度を保証し、欧州市場を牽引しています。

- 自動車業界の保証管理は、サプライヤーからディーラー、最終消費者までの全プロセスにまたがる豊富なデータが、さまざまなレベルでエラーの確率を高めているため、複雑なものとなっています。各ディーラーやメーカーは、保証請求やデータの取り扱いについて独自の手順を持っているが、従来のシステムでは信頼性や一貫性のある結果が得られないことが多く、欧州の保証管理システムの導入に拍車をかけています。

- 保証管理システムは、広範なビジネスルールを使用してすべての特典機能を検証し、診断およびモバイル機器からの情報ストリームを保証請求フォームに即座に組み込むことによって、保証情報の正確性と品質を向上させます。このアプリケーションは、返品の承認、返品の追跡、RGA/RMAの作成、マテリアルハンドリングの返品承認を処理します。部品やコンポーネントのサプライヤー保証を管理することで、保証トラッカーはサプライヤーとメーカーが協力して保証コストを削減することを可能にし、市場の普及に拍車をかけています。

- しかしながら、欧州の保証管理システムでは競争が激化し、価格感応度が高まっているため、エンドユーザが保証管理システムを選択する際に、価格よりもサービス機能を妥協する可能性があるため、プロバイダは市場の成長を制限しています。さらに、不正確な診断、過剰なメンテナンス、不正行為、保証と修理手順の理解不足に起因する過大請求が、予測期間中の市場成長率を阻害しています。

- COVID-19の流行に伴い、自動化技術へのシフトが地域全体で顕著になっています。生産性の向上、データの信頼性、クレームデータの有効性の強化、品質など、かなりの利点が、AIやMLを用いた自動保証管理システムの導入に顧客を誘い込み、市場の成長率に寄与しています。

欧州の保証管理システム市場動向

クラウド展開セグメントが主要市場シェアを占める

- 新たなデータストレージを構築・維持する代わりに、データをクラウドに移行することでコストとリソースを節約することの重要性に対する企業の認識が高まっていることが、クラウドベースのソリューションに対する需要、ひいてはこの地域におけるオンデマンド保証管理システムの採用を後押ししています。さらに、クラウドプラットフォームとエコシステムは、複数の利点があるため、今後数年間で、デジタル革新のペースと規模を爆発的に拡大させる発射台としての役割を果たすと予想されます。

- さらに、パブリッククラウドサービスを導入することで、信頼性の境界が組織の枠を超えて広がり、クラウドインフラにとってセキュリティが不可欠な要素となります。しかし、クラウドベースのソリューションの利用が増えたことで、企業の保証管理慣行の導入が大幅に簡素化されました。グーグルドライブ、ドロップボックス、マイクロソフトアジュールなどのクラウド・サービスの採用が増加し、これらのツールがビジネスプロセスの不可欠な部分として台頭する中、企業は、オンデマンドの保証管理ソリューションを取り入れることで、機密データのコントロールを失うなどのセキュリティ問題に対処しなければならないです。

- この国で最も急成長している市場のひとつがクラウドであり、この分野への投資の増加は、調査対象業界の領域を広げています。大手サービスプロバイダーは、国内の広範なパブリッククラウド環境やハイブリッドクラウド環境、ハイパースケール・サービスの管理をますます強化しています。例えば、オラクルは2022年7月、EU全域の顧客により良いサービスを提供するため、2023年にEUに新たなソブリンクラウドゾーンを導入すると発表しました。ドイツとスペインがEU初の2つのソブリンクラウド地域をホストする予定で、同地域の現在のパブリックOCI地域とは論理的にも物理的にも区別されます。新しいソブリンクラウドリージョンでは、民間企業や政府機関が、機密性の高い、規制の対象となる、あるいは戦略的に重要な地域のデータやアプリケーションをホストできるようになります。

- また、クラウドベースのソリューションは、設備投資要件が低いというメリットもあり、ビジネスの説得力が増します。クラウドベースのサービスを導入すれば、企業はハードウェアコンポーネントに投資する必要がないため、設備投資要件を大幅に削減できます。また、クラウドソリューションは、アプリケーションのコストをより正確に予測することができるため、企業はテクノロジーを導入するための初期費用をそれほど負担する必要がないです。また、ハードウェアとITサポートの節約により、クラウドベースのソリューションはより手頃な価格になっています。

- さらに、クラウドベースのシステムの採用が拡大していることも、市場の成長に寄与しています。例えば、欧州連合(EU)では昨年、EU企業の41%がクラウドコンピューティングを採用したと発表しています。EUでは、特に小売業でクラウドコンピューティングの利用が伸びています。クラウドコンピューティングには、クラウドインフラストラクチャとソフトウェアアプリケーションの2つのコンポーネントが含まれます。保証管理システムにおけるソフトウェアアプリケーションの需要の高まりが、予測期間中の市場成長に寄与すると予想されます。

ドイツが最速の成長を記録する見込み

- ドイツは、さまざまな産業における政府の規制と、顧客の多様なニーズを満たすためのソフトウェア開発の増加により、この地域で最も急成長している国の一つです。重機械、自動車、その他多くの産業で生産量が増加しており、顧客に販売した製品の保証期間やクレームを追跡できるよう、この地域で保証管理システムの生産が促進されています。

- 最近、ドイツの法律家は、顧客に有利な保証規制を強化する新しい販売法を可決しました。2年間の保証期間は、商品およびサービスの購入日または引き渡し日から適用されます。保証期間の終了間際に欠陥が発見された場合、条件に若干の修正が加えられます。この制限が適用されるのは、購入から4ヶ月が経過した後です。このシナリオは、保証期間満了直前に問題が顕在化した場合、購入者に保証請求のための余分な時間を与えます。

- 自動車メーカーと保証会社間のパートナーシップの高まりは、市場の研究を促進すると予想されます。このような開発は、ワークフローを合理化し、クレームを追跡するために、彼らの製品ポートフォリオに新しいソリューションを展開することを後押しします。例えば、Europe Assistance Germanyは、長年のパートナーであり保証保険会社であるReal Garant VersicherungAGに車両保証のポートフォリオを委託し、自動車産業における主要事業である欧州全域のモビリティサービスの処理に専念しています。

- ドイツ貿易投資庁によると、バリューチェーンに沿った約6,600の企業があり、その90%近くが中小企業であることから、機械・設備はドイツで最も活発なセクターです。ドイツの機械・設備(M&E)部門は、100万人以上の労働者を擁するドイツ最大の産業雇用者であり続けています。M&E部門は国内で最も革新的な部門のひとつであり、昨年は合計で約170億ユーロを研究開発に費やしました。工作機械、駆動技術、マテリアルハンドリング機器部門は、機械工学部門の中でも年間売上高が最も大きい部門です。機器製造業界では、このように多くの企業が、購入した組み立て部品ごとに保証書を管理しなければならないです。保証管理システムは、保証、クレーム、収益性を容易に監視・管理する高度なツールを提供するため、保証管理システムを導入することで、このような多忙な作業を軽減することができます。

- ドイツでは、人口の増加と高齢化、慢性疾患の増加、インフラの整備、技術の進歩が、この分野の拡大に寄与しています。保証管理システムは、ペースメーカーや除細動器などの埋め込み機器の保証プロセスを効率的に管理します。保証期間中の機器の返却を合理化し、リコールの際には必要な書類を作成します。ドイツでは、ヘルスケアは公的医療と民間医療によって提供されています。政府はヘルスケア産業に多額の投資を行っており、その結果、両心室ペースメーカー、植え込み型除細動器、植え込み型心臓ループ記録装置、ペースメーカーなどの革新的な手術器具が利用できるようになりました。

欧州の保証管理システム産業概要

- 欧州の保証管理システム市場は、Oracle Corporation、IBM Corporation、Syncron AB、Servicemax Inc.これらの企業は、顧客にカスタマイズされたソリューションを提供するために幅広く投資しています。さらに、市場の新興企業は投資家から資金を集めています。市場の主要企業は、市場での地位を維持するために、提携、合併、買収、投資を行っています。

- 2022年11月、サービスライフサイクル管理の世界的リーダーの1社であるデジタル製品・ソリューション企業のTavant Technologies Inc.は、商用メーカーの世界的リーダーの1社であるDaimler Truck AG(DTAG)と提携し、DTAGの欧州ブランド向けに保証・クレーム管理ソリューションを提供することを発表したが、これは欧州の自動車製造業における保証管理システムの市場導入を示すものです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の市場への影響評価

第5章 市場力学

- 市場促進要因

- 製造業と自動車産業における保証管理システムの採用増加

- 顧客満足を確保するための次世代保証管理システムにおけるAIとML機能の採用増加

- 市場抑制要因

- 価格に敏感な市場における独立系サービスプロバイダー間の激しい競合

第6章 市場セグメンテーション

- 展開別

- オンプレミス

- クラウド

- エンドユーザー産業別

- 産業機器

- 自動車・輸送機器

- 耐久消費財

- その他のエンドユーザー産業(医療機器、航空宇宙、防衛など)

- 国別

- 英国

- ドイツ

- フランス

- その他欧州

第7章 競合情勢

- 企業プロファイル

- Syncron AB

- IFS AB

- Tavant Technologies Inc.

- ServiceMax Inc.

- SKYLYZE

- Pegasystems Inc.

- PTC Inc.

- Oracle Corporation

- IBM Corporation

- Wipro Limited

第8章 投資分析

第9章 市場機会と今後の動向

目次

Product Code: 92648

The Europe Warranty Management System Market size is estimated at USD 1.66 billion in 2025, and is expected to reach USD 3.07 billion by 2030, at a CAGR of 13.07% during the forecast period (2025-2030).

Key Highlights

- A crucial part of every service business is warranty management. The capacity to view, access, and automatically track client asset warranty coverage and data is critical. With warranty management, companies may be protected by loss of sales and customer displeasure.

- The warranty management system enables service businesses to design, administer, track, and process warranties, claims, and assets by automating warranty claim handling and installed base asset tracking. Innovative warranty management systems (WMS) are linked with AI and machine learning capabilities to guarantee customer satisfaction, driving the European market.

- The automobile sector's management of warranties is complex because the abundance of data, which spans the entire process from suppliers to dealers to final consumers, increases the probability of errors at different levels. Although each dealer and manufacturer has unique procedures for handling warranty claims and data, the traditional systems frequently do not produce reliable or consistent results, fuelling the adoption of warranty management systems in Europe, supported by the region's industrial development in automating.

- The warranty management system improves the accuracy and quality of warranty information by validating all privilege features using broad business rules and immediately incorporating information streams from diagnostic and mobile devices into warranty claim forms. The application handles the authorization of returns, tracking of returns, and creation of RGA/RMA or approvals for returns of material. By managing supplier warranties for parts and components, the warranty tracker enables suppliers and manufacturers to work together to cut warranty costs, fueling market adoption.

- However, due to the increasing competition and the increase in the Price sensitivity in the European warranty management system, providers are limiting the market growth because end users could compromise service features over price while choosing the warranty management system for their business due to the high price sensitivity in the market. Additionally, inaccurate diagnosis, excessive maintenance, fraud, and overcharging resulting from a lack of understanding of the warranty and repair procedure hamper the market growth rate during the forecast period.

- With the COVID-19 pandemic, the shift toward automated technologies has been significant across the region. Considerable advantages like enhanced productivity, data reliability, enhanced claim data validity, quality, etc., are luring customers into adopting automated warranty management systems with AI and ML, contributing to the market's growth rate.

Europe Warranty Management System Market Trends

Cloud Deployment Segment Holds Major Market Share

- The increasing realization among enterprises about the importance of saving money and resources by moving their data to the cloud instead of building and maintaining new data storage drives the demand for cloud-based solutions and, hence, the adoption of on-demand warranty management systems in the region. Moreover, owing to multiple benefits and over the next few years, cloud platforms and ecosystems are anticipated to serve as a launchpad for an explosion in the pace and scale of digital innovation.

- Furthermore, deploying public cloud services extends the boundary of trust beyond the organization, making security a vital part of the cloud infrastructure. However, the increasing usage of cloud-based solutions has significantly simplified enterprises' adoption of warranty management practices. With the increased adoption of cloud services, such as Google Drive, Dropbox, and Microsoft Azure, among others, and with these tools emerging as an integral part of business processes, enterprises must deal with security issues, such as losing control over sensitive data, raises the incorporation of on-demand warranty management solutions.

- One of the country's fastest-growing markets is the cloud, and rising investment in the sector is broadening the area of the industry under study. Large service providers increasingly manage the country's extensive public and hybrid cloud environments and hyper-scale services. For instance, in July 2022, Oracle announced it would introduce new sovereign cloud zones for the European Union in 2023 to serve its clients across the European Union better. Germany and Spain will host the first two EU sovereign cloud regions, which will be logically and physically distinct from the region's current public OCI regions. The new sovereign cloud regions will allow private businesses and government agencies to host sensitive, regulated, or strategically significant regional data and applications.

- Cloud-based solutions also benefit from lower capital expenditure requirements, making the business more compelling. Deploying cloud-based services can significantly reduce the Capex requirement as companies do not need to invest in hardware components. Cloud solutions also enable better prediction of the cost of an application, and companies don't need to incur as much upfront cost to incorporate the technology. Also, hardware and IT support savings make cloud-based solutions much more affordable.

- Furthermore, the growing adoption of cloud-based systems contributes to market growth. For instance, the European Union states that 41% of EU businesses adopted cloud computing last year. In the European Union, cloud computing usage grew, especially in retail. Cloud computing involves two components, which are cloud infrastructure and software applications. The growing demand for software applications in warranty management systems is expected to contribute to the market's growth during the forecast period.

Germany is Expected to Register the Fastest Growth

- Germany is one the fastest-growing countries in the region due to government regulations in different industries and the increasing development of software to satisfy customers' diverse needs. The demand for heavy equipment, automotive, and many more industries is increasing their production, driving the output of warranty management systems in the region so that the sectors may track the warranty periods and claims made on the products sold to customers.

- Recently, German lawmakers passed a new sales law that tightens warranty regulations in favor of customers. The two-year warranty period will be applicable for goods and services from the date of purchase or delivery. If a flaw is discovered near the conclusion of the warranty period, some modifications will be made to the conditions. The limitations are applicable only after the completion of four months after the purchase. This scenario gives the buyer extra time to make warranty claims if the issue materializes just before the expiration of the warranty period.

- The rise in partnerships between the automotive and warranty issuer firms is expected to drive the market studied. Such developments will push them to deploy new solutions in their product portfolio to streamline the workflow and track the claims. For instance, Europe Assistance Germany outsourced its portfolio of vehicle warranties to its long-time partner and warranty insurance Real Garant VersicherungAG to concentrate on its main business in the automotive industry, the processing of mobility services across Europe.

- According to German Trade and Invest, with almost 6,600 enterprises along the value chain, nearly 90% of which are SMEs, machinery and equipment are Germany's most active sector. The German Machinery and Equipment (M&E) sector continues to be the largest industrial employer in Germany, with a workforce of more than one million workers. The M&E sector is one of the most innovative in the nation, which spent about EUR 17 billion on research and development in total in the last year. The machine tools, drive technology, and material handling equipment sectors are some of the most significant in yearly turnover within the mechanical engineering sector. Such a high number of firms in the industry of equipment production have to maintain warranty documents for each assembled part they buy. Such hectic work can be reduced by deploying warranty management systems because they provide advanced tools to easily monitor and manage warranties, claims, and profitability.

- In Germany, population growth and aging, an increase in chronic disease prevalence, infrastructure improvements, and technological advancements have contributed to the sector's expansion. The warranty management systems efficiently manage the warranty processes for implanted devices like pacemakers and defibrillators. They streamline the return of the equipment under warranty and fill out the necessary paperwork in the event of a recall. In Germany, healthcare is made available through public and private healthcare. The government is making significant investments in the healthcare industry, which has led to the availability of innovative surgical tools such as biventricular pacemakers, implantable cardioverter defibrillators, implantable cardiac loop recorders, and pacemakers.

Europe Warranty Management System Industry Overview

- The European warranty management system market is highly fragmented due to various market players like Oracle Corporation, IBM Corporation, Syncron AB, Servicemax Inc., Tavant Technologies Inc., etc. These companies are extensively investing in offering customized solutions to customers. Moreover, the startups in the market are attracting funding from investors. The key players in the market are making partnerships, mergers, acquisitions, and investments to retain their market position.

- In November 2022, Tavant Technologies Inc., a digital products and solutions company, one of the global leaders in service lifecycle management, announced a partnership with Daimler Truck AG (DTAG), one of the global leaders in commercial manufacturers, to offer warranty and claim management solutions for the DTAG European brands, which shows the market adoption of warranty management systems in the European automotive manufacturing industries.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Adoption of Warranty Management Systems in the Manufacturing and Automotive Industries

- 5.1.2 Increasing Adoption of AI and ML Capabilities in Next-generation Warranty Management Systems to Ensure Customer Satisfaction

- 5.2 Market Restraints

- 5.2.1 Intense Competition Between Independent Service Providers in Price-sensitive Markets

6 MARKET SEGMENTATION

- 6.1 By Deployment

- 6.1.1 On-Premise

- 6.1.2 Cloud

- 6.2 By End-user Industry

- 6.2.1 Industrial Equipment

- 6.2.2 Automotive and Transportation

- 6.2.3 Consumer Durable

- 6.2.4 Other End-user Industries (Medical Devices, Aerospace, Defense, Etc.)

- 6.3 By Country

- 6.3.1 United Kingdom

- 6.3.2 Germany

- 6.3.3 France

- 6.3.4 Rest of Europe

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Syncron AB

- 7.1.2 IFS AB

- 7.1.3 Tavant Technologies Inc.

- 7.1.4 ServiceMax Inc.

- 7.1.5 SKYLYZE

- 7.1.6 Pegasystems Inc.

- 7.1.7 PTC Inc.

- 7.1.8 Oracle Corporation

- 7.1.9 IBM Corporation

- 7.1.10 Wipro Limited

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

欧州の保証管理システム:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 108 Pages

- 納期

- 2~3営業日