|

市場調査レポート

商品コード

1940830

トマト種子:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Tomato Seed - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| トマト種子:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年02月09日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

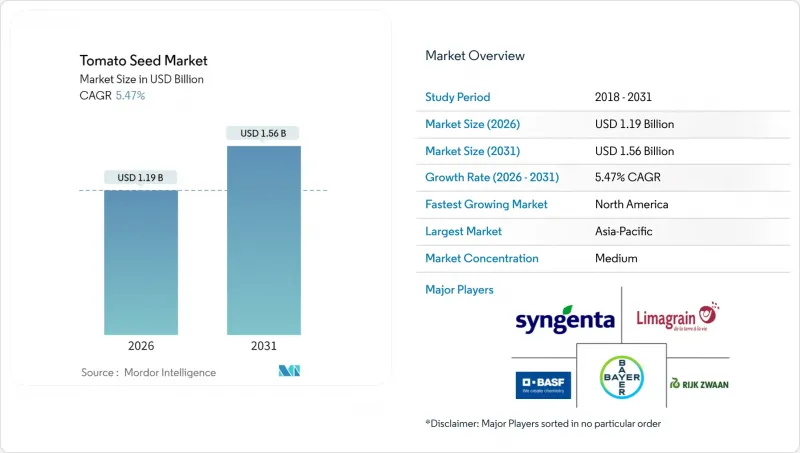

トマト種子市場は2025年に11億3,000万米ドルと評価され、2026年の11億9,000万米ドルから2031年までに15億6,000万米ドルに達すると予測されています。

予測期間(2026-2031年)におけるCAGRは5.47%と見込まれます。

高収量ハイブリッド品種の需要、保護栽培の急速な普及、遺伝子編集技術による形質スタックの着実な進展が成長の要因となっております。複数の病原体に耐性を持つハイブリッド種子の広範な採用により、生鮮・加工両サプライチェーンにおける高収量率が確保される一方、温室栽培の拡大により生産者は通年収穫が可能となり、プレミアム価格設定を目指しております。アジア太平洋地域は生産面で主導権を維持し、北米は最も速い成長率を示しています。市場の細分化により、ニッチな育種業者が気候変動に強い品種を商業化できる環境が整っています。一方で、小規模農家における非公式な種子の再利用や、バイオテクノロジー承認プロセスの長期化が、特定の開発途上地域における成長を抑制する要因となっています。

世界のトマト種子市場の動向と洞察

高収量ハイブリッド品種の需要増加

カリフォルニア州セントラルバレーやイタリアのポーバレーといった加工拠点では、機械収穫機が均一なサイズと同期した成熟期間を必要とするため、主にハイブリッド品種に依存しています。ハイブリッド品種は自然交配系統に比べて大幅な収量向上をもたらし、人件費やエネルギーコストの上昇による圧力に直面する加工業者の利益率を支えています。新興市場における契約栽培モデルは、初期の種子費用の管理を支援し、小規模農家が収量メリットを享受することを可能にしております。CRISPRガイド選択技術による追加的な雑種強勢効果の獲得により、種子開発者は育種サイクルを短縮し、ハイブリッド品種の市場投入を加速させることが可能となります。

保護栽培面積の拡大

年間を通じた温室栽培は、屋外栽培の単一サイクルと比較して複数回の収穫を可能にし、多額の資本投資を支えます。オランダの施設では、プレミアム小売プログラム向けに均一な品質を維持しながら、露地栽培よりも大幅に高い収量を達成しています。シンガポールを含む土地不足の経済圏では、限られた空間で生産量を最大化するため垂直農法が推進されています。気候変動の影響により、スペイン、メキシコ、日本の農家は極端な暑さや降雨量の変動を緩和するため管理環境へ移行しており、温室専用種子遺伝学への需要が拡大しています。

小規模農家における自家採種慣行の増加

東アフリカの多くのトマト農家は、後続の栽培サイクルで収量が減少するにもかかわらず、第二世代の種子を保存しています。この慣行は、作付け期の資金制約と融資へのアクセス制限によって促されています。低コストのハイブリッド品種や柔軟な支払いプランが代替手段を提供しているもの、無料で入手できる自家採種種子との競争には苦戦しています。その結果、ハイブリッド品種の採用と潜在的な収量向上の可能性は、いくつかの発展途上地域で十分に活用されていない状況です。

セグメント分析

ハイブリッド品種は2025年にトマト種子市場シェアの72.25%を占め、2031年までCAGR5.55%で拡大が見込まれております。これは生産者が病害抵抗性と均一性を重視していることを示しています。商業加工業者は、成熟の同期化により収穫作業回数と選別コストが削減されるため、ハイブリッドを好んで採用しております。予測期間中、保護栽培システムが専用温室用遺伝子を指定するため、ハイブリッド系統のトマト種子市場は引き続き大幅に拡大します。自然交配品種は、自給農業や伝統品種小売ニッチ市場で人気を維持しており、種子の保存と風味の真正性が購買決定を左右します。トマト種子市場はCRISPR選抜技術の恩恵を受けており、これにより育種サイクルが大幅に短縮され、複数世代のバッククロスを必要とする複合形質の導入が可能となります。

自然交配品種は生物多様性保全と有機農業において重要な役割を担っています。種子ライブラリーや農家協同組合がこれらの品種をサハラ以南アフリカや南米に流通させ、正式な小売網を迂回しながらも地域適応を支える非公式な取引経路を形成しています。一部のハイブリッド派生品種は、より低廉な種子コストで部分的な雑種強勢効果を提供することでギャップを埋め、中規模投入システムでの採用を支援します。総販売量は少ないもの、開放受粉種子の販売は消費者セグメント間で収益を分散させるため、トマト種子市場に回復力を加えています。見通し期間中、継続的な研究開発費を考慮するとハイブリッドの価格プレミアムは持続しますが、資金制約と伝統的嗜好が支配的な地域では開放受粉種子の需要は存続するでしょう。

トマト種子市場レポートは、育種技術(ハイブリッド品種、開放受粉品種、ハイブリッド派生品種)、栽培形態(露地栽培、保護栽培)、地域(アフリカ、アジア太平洋、欧州、中東、北米、南米)別に分析されています。市場予測は金額(米ドル)と数量(メトリックトン)で提示されます。

地域別分析

アジア太平洋地域は2025年に世界収益の36.20%を維持し、中国における生鮮・加工両チャネルを合わせた5,960万メトリックトンの生産量が基盤となっています。地方政府は耐熱性ハイブリッド種の種子購入を補助しており、インドの保護栽培プロジェクトでは毎年二桁のヘクタール規模で拡大しています。カルナータカ州やマハラシュトラ州などにおける温室導入は、2024年だけで15%増加し、気候適応型遺伝資源への需要を押し上げました。一方、インドネシアとベトナムでは、都市部小売供給向けの垂直栽培システムが拡大しており、これらは連続結実型ハイブリッド品種に依存しています。

北米はCAGR7.21%で拡大し、2031年まで最速成長地域を維持すると予測されています。カリフォルニア州セントラルバレーは加工量で引き続き首位を維持し、同地の生産者は工場の処理効率化を図るため、可溶性固形分を高めたハイブリッド品種へ迅速に移行しました。カナダとメキシコでは、米国全土の冬季市場へ供給するハイテク温室が拡大し、人工光に耐性のある不定型温室品種の需要を支えています。北米の研究機関やベンチャー資金による新興企業もCRISPR技術を用いた形質導入を加速させており、地域のイノベーションリーダーシップを強化しています。

欧州は厳格なバイオテクノロジー規制にもかかわらず着実な成長を遂げています。オランダとスペインでは、コージェネレーションシステムとディープウォーターカルチャーを組み合わせた省エネルギー型温室を導入し、通年供給を維持しています。イタリアのポー川流域は加工用生産の中心地であり、均一な成熟特性を備えたハイブリッド品種が好まれます。南欧では夏季の高温化と降雨量の不安定化に直面しているため、耐乾性品種の採用が進んでいます。並行して、欧州の「農場から食卓まで」戦略に基づく農薬削減への消費者志向が高まり、欧州規制当局が承認したマーカー支援バッククロス法で育種された耐病性種子の採用が促進されています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

- 調査手法

第2章 レポート提供

第3章 エグゼクティブサマリーおよび主要な調査結果

第4章 主要な業界動向

- 作付面積

- 主流の形質

- 育種技術

- 規制の枠組み

- バリューチェーン及び流通チャネル分析

- 市場促進要因

- 高収量ハイブリッド品種の需要増加

- 保護栽培面積の拡大

- 耐病性形質の採用拡大

- 加工用トマト産業の急速な成長

- CRISPR技術を活用した風味と保存性の特性スタック

- 種子バンク主導の気候耐性遺伝子型共同研究の急増

- 市場抑制要因

- 小規模農家における自家採種慣行の普及拡大

- バイオテクノロジー品種の承認プロセスにおける厳格なスケジュール

- 種子価格における統合主導のロイヤルティ高騰

- 在来種市場における特許保護形質への消費者反発の高まり

第5章 市場規模と成長予測(金額および数量)

- 育種技術

- ハイブリッド品種

- 開放受粉品種および交雑品種

- 栽培メカニズム

- 露地栽培

- 保護栽培

- 地域

- アフリカ

- 育種技術別

- 栽培メカニズム別

- 国別

- エジプト

- エチオピア

- ガーナ

- ケニア

- ナイジェリア

- 南アフリカ

- タンザニア

- その他アフリカ

- アジア太平洋地域

- 育種技術別

- 栽培メカニズム別

- 国別

- オーストラリア

- バングラデシュ

- 中国

- インド

- インドネシア

- 日本

- ミャンマー

- パキスタン

- フィリピン

- タイ

- ベトナム

- その他アジア太平洋地域

- 欧州

- 育種技術別

- 栽培メカニズム別

- 国別

- フランス

- ドイツ

- イタリア

- オランダ

- ポーランド

- ルーマニア

- ロシア

- スペイン

- トルコ

- ウクライナ

- 英国

- その他欧州地域

- 中東

- 育種技術別

- 栽培メカニズム別

- 国別

- イラン

- サウジアラビア

- その他中東

- 北米

- 育種技術別

- 栽培メカニズム別

- 国別

- カナダ

- メキシコ

- 米国

- その他北米地域

- 南米

- 育種技術別

- 栽培メカニズム別

- 国別

- アルゼンチン

- ブラジル

- その他南米

- アフリカ

第6章 競合情勢

- 主要な戦略的動きs

- 市場シェア分析

- 企業概況

- 企業プロファイル

- Bayer AG

- Syngenta Group

- BASF SE

- Groupe Limagrain

- Rijk Zwaan BV

- Advanta Seeds(UPL Ltd.)

- Sakata Seed Corporation

- East-West Seed

- Enza Zaden Beheer B.V.

- Takii and Company Ltd.

- Yuan Longping High-Tech Agriculture

- Bejo Zaden BV

- VNR Seeds Pvt. Ltd.

- NongWoo Bio Co. Ltd.

- Mahyco