|

市場調査レポート

商品コード

1693420

欧州のシアノアクリレート接着剤:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Europe Cyanoacrylate Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州のシアノアクリレート接着剤:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 182 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

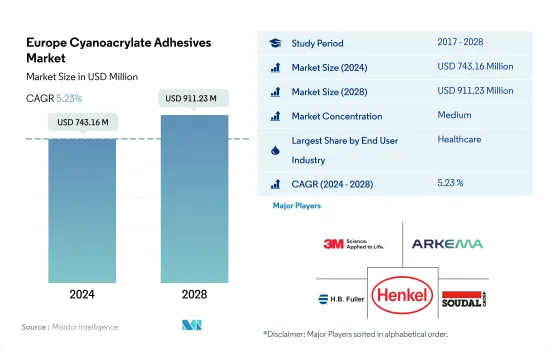

欧州のシアノアクリレート接着剤市場規模は、2024年に7億4,316万米ドルと推定され、2028年には9億1,123万米ドルに達すると予測され、予測期間(2024-2028年)のCAGRは5.23%で成長すると予測されます。

航空宇宙分野での反応技術に基づくシアノアクリレート接着剤需要が欧州の成長率を牽引

- 欧州には大規模な製造拠点があり、輸出ネットワークも確立されています。ヘルスケア、航空宇宙、自動車、建築・建設、海洋は、2017年から2019年にかけてシアノアクリレート接着剤に安定した需要を生み出した、この地域の数少ない確立された産業の一つです。ドイツ、フランス、英国のような国々は、欧州地域からシアノアクリレート接着剤のために生成された需要のより大きなシェアを占めています。

- 2020年、シアノアクリレート接着剤の需要は、COVID-19パンデミックのため、2019年の水準と比較して11.24%減少しました。操業、貿易、サプライチェーンの制限により、自動車、航空宇宙などの産業は減産を余儀なくされています。このことは、この期間の同地域のシアノアクリレート接着剤需要にマイナスの影響を及ぼしています。

- 全地域の中でも、欧州の自動車、航空宇宙、木工・建具、その他の産業は研究開発活動に力を入れています。同地域のすべての産業は、2050年までにネット・ゼロ・エミッションを達成するため、カーボンフットプリントの削減に注力しています。自動車や航空宇宙産業など、燃費効率や軽量化が重要な役割を果たす産業では、予測期間中にシアノアクリレート接着剤の需要が急増する可能性があります。欧州のすべての国の中で、フランスは、予測期間(2022-2028)中に6.27%のCAGRで、シアノアクリレート接着剤の需要が最も高い成長を示すことが期待されています。

- シアノアクリレート接着剤の需要では、用途の多さからヘルスケアが最大のシェアを占めています。しかし、航空宇宙のエンドユーザー産業からの反応性技術によるシアノアクリレート接着剤の需要の伸びは、2022-2028年に6.95%の最も高いCAGRで期待されています。

欧州各国の航空宇宙産業の開発が市場の成長を最も押し上げる

- シアノアクリレート接着剤は、組み立て時間の短縮に役立ち、主にヘルスケア産業で消費されています。ヘルスケア産業は、欧州で接着剤の約3万7,362トンを消費し、2021年に欧州のシアノアクリレート接着剤市場の36.21%を占めました。これらの接着剤は、使い捨て医療機器の製造やその他のヘルスケア用途に使用されています。

- ドイツは欧州におけるシアノアクリレート接着剤の最大消費国です。2021年には、これらの接着剤の約40%がドイツのヘルスケア産業で使用されており、これは世界第3位のヘルスケア産業です。2021年、同国のヘルスケア支出は約7,920億米ドルで、同国のGDPのほぼ12%に寄与しています。同年、同国による医療機器の輸出は11.85%増加しました。同国のヘルスケア産業からのこのような需要の高まりは、今後数年間にわたってシアノアクリレート接着剤の需要を促進すると予想されます。

- 航空宇宙産業は、欧州におけるシアノアクリレート接着剤の消費で最も急成長しているエンドユーザー産業であり、予測期間2022-2028年のCAGRは7.24%を記録すると予想されています。ドイツの航空宇宙産業は技術革新によって牽引されており、2021年には約25億ユーロが研究開発に費やされました。フランスでは、エアバスが生産速度と生産能力を2021年の月産40機から2023年には月産64機、2024年初頭には月産70機にまで引き上げる計画を発表しました。これらの要因により、欧州におけるシアノアクリレート接着剤の需要は今後数年間増加すると予想されます。

- 反応性シアノアクリレート接着剤は主に欧州で消費され、2021年にはシアノアクリレート総需要の75%を占めました。その需要は予測期間中にさらに伸びると予想されます。

欧州のシアノアクリレート接着剤市場動向

電気自動車を推進する政府の積極的な取り組みが業界規模を押し上げる

- 欧州の一人当たりGDPは3万4,230米ドルで、2022年の成長率は前年比1.6%です。自動車産業部門がGDP全体に占める割合は約2%です。2021年の欧州の自動車生産台数は、乗用車81%、商用車17%、その他2%です。

- 2020年には、ドイツ、イタリア、スペイン、ロシア、英国など、多くの欧州諸国がCOVID-19パンデミックの影響を受けました。パンデミックはサプライチェーンの混乱、各国での操業停止、チップ不足をもたらし、欧州の自動車生産に影響を与えました。自動車の生産台数は2019年比で22%も激減しました。

- 米国は欧州から25.3%相当の自動車を輸入しており、2021年にはドイツが10.3%、英国が4.7%を占める主要輸入国のひとつとなりました。2022年初頭、ロシアによるウクライナ侵攻により新車販売が20.5%減少し、それが自動車生産にも反映されました。2022年第1四半期の欧州自動車市場は、前年同期比で10.6%減少しました。

- 自動車生産台数は、多くの欧州諸国が電気自動車に新たな投資を行っているため、期間中(2022~2027年)にCAGR 2.25%で成長する可能性が高いです。例えば、スペインは電気自動車生産に51億米ドルを投資する予定です。

審美的でスマートな家具への需要の高まりが業界の成長を後押しする

- 欧州は世界有数の家具生産国です。この地域は、アジア太平洋地域に次いで、世界の家具生産の30%近くを占めています。ドイツ、イタリア、ロシア、スペインが家具とその製品のトップ生産国です。しかし、この地域は2020年に発生したCOVID-19の影響を受け、数カ国で生産施設の操業停止を余儀なくされました。このため、家具の生産量は前年比7.14%減少しました。

- ドイツは欧州最大の家具生産国です。2021年には3億2,360万個近くを生産し、これは欧州の家具生産量の23%にあたる。ドイツの小売業者は3D製品ビジュアライゼーションや拡張現実アプリの提供を始めており、これが同国のeコマース・ポータルを通じて家具製品の需要を押し上げています。

- イタリアもまた、欧州における家具とその製品の主要生産国であり、イタリア家具が人気の国です。同国は欧州の家具生産の15%を占めています。同国の家具輸出は一定の成長率を記録しており、2018年は約2.7%、2019年は約3%でした。イタリアの木工・建具産業における技術進歩は世界的に採用されています。

- 欧州は家具市場のハイエンドセグメントをリードしています。世界で販売される高級家具製品の3つに2つ近くがEUで生産されていると言われています。欧州の家具メーカーは、パイン材、オーク材、ブナ材など、環境に優しい素材を生産に使用しており、同地域での需要が高まっています。これらの要因によって、今後数年間、欧州での家具生産は増加すると思われます。

欧州のシアノアクリレート接着剤産業の概要

欧州のシアノアクリレート接着剤市場は、上位5社で63.01%を占め、緩やかに統合されています。この市場の主要企業は以下の通り。 3M, Arkema Group, H.B. Fuller Company, Henkel AG & Co. KGaA and Soudal Holding N.V.(アルファベット順)

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- エンドユーザー動向

- 航空宇宙

- 自動車

- 建築・建設

- 履物・皮革

- 木工・建具

- 規制の枠組み

- EU

- ロシア

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- エンドユーザー産業

- 航空宇宙

- 自動車

- 建築・建設

- 履物・皮革

- ヘルスケア

- 木工・建具

- その他のエンドユーザー産業

- テクノロジー

- 反応性

- UV硬化型接着剤

- 国名

- フランス

- ドイツ

- イタリア

- ロシア

- スペイン

- 英国

- その他欧州

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- 3M

- Arkema Group

- DELO Industrie Klebstoffe GmbH & Co. KGaA

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Illinois Tool Works Inc.

- Jowat SE

- Permabond LLC.

- Soudal Holding N.V.

- ThreeBond Holdings Co., Ltd.

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の接着剤とシーラント産業の概要

- 概要

- ファイブフォース分析フレームワーク(産業魅力度分析)

- 世界のバリューチェーン分析

- 促進要因、抑制要因、機会

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 92479

The Europe Cyanoacrylate Adhesives Market size is estimated at 743.16 million USD in 2024, and is expected to reach 911.23 million USD by 2028, growing at a CAGR of 5.23% during the forecast period (2024-2028).

Demand for cyanoacrylate adhesives based on reactive technology in aerospace to lead in growth rate in Europe

- Europe has a large manufacturing base and well-established export networks. Healthcare, aerospace, automotive, building and construction, and marine are among the few well-established industries in the region which have collectively generated steady demand for cyanoacrylate adhesives from 2017 to 2019. Countries like Germany, France, and The United Kingdom have occupied a larger share of the demand generated for cyanoacrylate adhesives from the Europe region.

- In 2020, the demand for cyanoacrylate adhesives declined by 11.24% compared to the 2019 levels because of the covid-19 pandemic. Operational, trade and supply chain restrictions have forced industries like automotive, aerospace, and others to have production cuts. This has negatively affected the demand for cyanoacrylate adhesives from the region during this period.

- Among all regions, European automotive, aerospace and woodworking and joinery, and other industries are heavily engaged in R&D activities. All Industries in the region are focusing on reducing their carbon footprint to achieve a net zero emissions goal by 2050. Industries like automotive and aerospace, where fuel efficiency and weight reduction play an important role, might witness a surge in demand for cyanoacrylate adhesives during the forecast period. Among all countries in Europe, France is expected to witness the highest growth in the demand for cyanoacrylate adhesives, with a CAGR of 6.27% during the forecast period (2022-2028).

- Healthcare occupies the largest share of the demand for cyanoacrylate adhesives because of the large number of applications. However, the growth in demand for cyanoacrylate adhesives with reactive technology from the aerospace end-user industry is expected to be with the highest CAGR of 6.95% in 2022-2028.

Developments in the aerospace industry across the European countries to have boost the market's growth the most

- Cyanoacrylate adhesives help in the reduction of assembly times and are consumed mainly in the healthcare industry. The healthcare industry consumes around 37,362 tons of adhesives in Europe, which accounted for 36.21% of the European cyanoacrylate adhesives market in 2021. These adhesives are used to manufacture disposable medical devices and other healthcare applications.

- Germany is the largest consumer of cyanoacrylate adhesives in Europe. In 2021, around 40% of these adhesives were used in the healthcare industry of Germany, which is the third largest healthcare industry globally. In 2021, the healthcare expenditure in the country was around USD 792 billion and contributed nearly 12% of the country's GDP. In the same year, the exports of medical devices by the country increased by 11.85%. Such rising demand from the healthcare industry in the country is expected to drive the demand for cyanoacrylate adhesives over the coming years.

- Aerospace is the fastest-growing end-user industry in the consumption of cyanoacrylate adhesives in Europe and is expected to record a CAGR of 7.24% during the forecast period 2022-2028. Germany's aerospace industry is driven by technological innovation, and around EUR 2.5 billion was spent on research and development in 2021. In France, Airbus announced plans to increase production speeds and capacity from 40 aircraft per month in 2021 to 64 per month in 2023 and as many as 70 per month by early 2024. These abovementioned factors are expected to boost the demand for cyanoacrylate adhesives over the coming years in Europe.

- Reactive cyanoacrylate adhesives are primarily consumed in Europe and accounted for 75% of the total cyanoacrylate demand in 2021. Their demand is expected to grow further over the forecast period.

Europe Cyanoacrylate Adhesives Market Trends

Supportive government initiatives to promote electric vehicles will raise the industry size

- Europe has a GDP of 34,230 USD per capita with a growth rate of 1.6% y-o-y in 2022. The automotive industry sector contributes a percentage of around 2% of the total GDP. The European vehicle production comprises 81% passenger vehicles, 17% commercial vehicles, and 2% other vehicles in 2021.

- In 2020, many European countries were affected by the COVID-19 pandemic, including Germany, Italy, Spain, Russia, and the United Kingdom. The pandemic resulted in supply chain disruptions, lockdowns in the countries, and chip shortages which affected automotive production in Europe. The production of vehicles sharply declined by 22% compared to 2019.

- The United States imports 25.3% worth of cars from Europe and became one of the leading importers of the United States, where Germany accounted for 10.3% and the United Kingdom for 4.7% of total imports of vehicles in the country in 2021. At the beginning of 2022, the sale of the new vehicle dropped by 20.5% due to the invasion of Ukraine by Russia, which reflected in vehicle production as well. In the first quarter of 2022, the European automotive market was down by 10.6% compared to the same period last year.

- Vehicle production is likely to grow with a CAGR of 2.25% during the period (2022 to 2027) due to the new investments being made in electric vehicles by many European countries. For instance, Spain is going to invest USD 5.1 billion in electric vehicle production.

Rising demand for aesthetic and smart furniture to aid the industry growth

- Europe is one of the largest producers of furniture in the world. The region contributes nearly 30% of global furniture production after the Asia-Pacific region. Germany, Italy, Russia, and Spain are the top producers of furniture and its products. However, the region was impacted by the COVID-19 outbreak in 2020, which resulted in the shutdown of production facilities in several countries. This has reduced their furniture production by 7.14% compared to the previous year.

- Germany is the largest producer of Furniture units in Europe. The country produced nearly 323.6 million units in 2021, which is 23% of Europe's furniture production. German retailers have started offering 3D product visualizations or augmented reality apps which are boosting the demand for furniture products through e-commerce portals in the country.

- Italy is another major producer of furniture and its products in Europe, and the country is popular for Italian Furniture. The country holds 15% of Europe's furniture production. The country's furniture exports recorded a constant growth rate, which was about 2.7% in 2018 and 3% in 2019. The technological advancement in the woodworking and joinery industry of Italy is adopted worldwide.

- Europe is a leader in the high-end segment of the furniture market. It is said that nearly two out of every three high-end furniture products sold in the world are produced in the European Union. The furniture manufacturers in Europe are using eco-friendly materials such as pine wood, oak wood, beech wood, and a few others for production, which is gaining demand in the region. These factors will raise furniture production in the coming years in Europe.

Europe Cyanoacrylate Adhesives Industry Overview

The Europe Cyanoacrylate Adhesives Market is moderately consolidated, with the top five companies occupying 63.01%. The major players in this market are 3M, Arkema Group, H.B. Fuller Company, Henkel AG & Co. KGaA and Soudal Holding N.V. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Footwear and Leather

- 4.1.5 Woodworking and Joinery

- 4.2 Regulatory Framework

- 4.2.1 EU

- 4.2.2 Russia

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Footwear and Leather

- 5.1.5 Healthcare

- 5.1.6 Woodworking and Joinery

- 5.1.7 Other End-user Industries

- 5.2 Technology

- 5.2.1 Reactive

- 5.2.2 UV Cured Adhesives

- 5.3 Country

- 5.3.1 France

- 5.3.2 Germany

- 5.3.3 Italy

- 5.3.4 Russia

- 5.3.5 Spain

- 5.3.6 United Kingdom

- 5.3.7 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 Arkema Group

- 6.4.3 DELO Industrie Klebstoffe GmbH & Co. KGaA

- 6.4.4 H.B. Fuller Company

- 6.4.5 Henkel AG & Co. KGaA

- 6.4.6 Illinois Tool Works Inc.

- 6.4.7 Jowat SE

- 6.4.8 Permabond LLC.

- 6.4.9 Soudal Holding N.V.

- 6.4.10 ThreeBond Holdings Co., Ltd.

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms