|

市場調査レポート

商品コード

1693419

アジア太平洋のシアノアクリレート接着剤- 市場シェア分析、産業動向、成長予測(2025~2030年)Asia-Pacific Cyanoacrylate Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋のシアノアクリレート接着剤- 市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 207 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

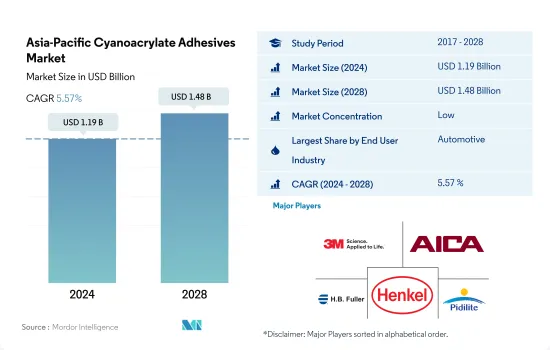

アジア太平洋のシアノアクリレート接着剤市場規模は2024年に11億9,000万米ドルと推定され、2028年には14億8,000万米ドルに達すると予測され、予測期間中(2024~2028年)のCAGRは5.57%で成長する見込みです。

航空宇宙産業や医療産業におけるシアノアクリレート接着剤の用途と需要の高まりが主要成長要因です。

- アジア太平洋のシアノアクリレート接着剤市場は、予測期間を通じてDIYやエレクトロニクスアプリケーションからの需要が急速に増加しているため、他のエンドユーザー産業によって支配される可能性が高いです。シアノアクリレートは、木材、金属、プラスチック、セラミック、エラストマーなどのさまざまな基材と短時間で優れた結合を作成するユニークな特性を持っており、DIYセグメントの専門家が使用するのに適しています。

- シアノアクリレート接着剤の消費量は、産業全体の重要な組立作業のアプリケーションの上昇に起因する自動車のために最近増加しています。シアノアクリレートは、広範囲の熱や温度下で安定した永久接着を記載しています。さらに、自動車メーカーは、安全性を犠牲にすることなく車両全体の重量を減らすために、軽量部品やコンポーネントの製造に取り組んでいます。したがって、自動車産業におけるシアノアクリレート接着剤の消費は、今後数年間で大きな伸びを示すと考えられます。

- 航空宇宙産業は、その不燃性、速硬化能力、機械的と構造的操作における手間のかからないアプリケーションのために、シアノアクリレートの消費の面で最も急成長しているセクタを確認する可能性が高いです。さらに、シアノアクリレートは、従来の縫合プロセスに代わる様々な医療外科用途の組織接着剤として急速に採用されています。さらに、シアノアクリレートの経口用途はここ数年、継続的な改善を示しています。これらの要因が、アジア太平洋におけるシアノアクリレート接着剤の今後の成長を後押しします。

インドネシアの医療産業が牽引するシアノアクリレート接着剤の高成長予測

- アジア太平洋は世界最大のシアノアクリレート接着剤消費地域で、2021年にはシアノアクリレート接着剤総消費量の42.9%を占めます。シアノアクリレート接着剤は、この地域の自動車、医療、DIY、その他の産業で消費される瞬間接着剤です。

- 中国は、この地域と世界におけるシアノアクリレート接着剤の最大消費国です。これらの接着剤は同国の自動車産業と医療産業で主に使用されています。中国の自動車産業は約2万3,036トンのシアノアクリレート接着剤を消費しています。自動車生産台数は、2021年の2,620万台から2025年には3,420万台に達すると予想されています。このような自動車産業からの需要拡大は、同国におけるシアノアクリレート接着剤の需要を牽引すると予想されます。

- 航空宇宙は、この地域でシアノアクリレート接着剤のエンドユーザー産業として最も急成長しており、予測期間2022~2028年には数量ベースでCAGR 6.26%を記録すると予想されています。中国は「メイドイン2025」計画を実施しており、航空機メーカーは航空機の100%を中国で調達・製造することを義務付け、外国企業の参入を制限しています。一方、現地の航空宇宙用接着剤・シーラントメーカーは、この政府計画から恩恵を受けると予想されます。同地域の他の国々が実施している同様の施策は、同地域の航空宇宙産業を後押しすると予想されます。

- インドネシアは、同地域と世界市場において最も急成長している国であり、医療産業の成長により、予測期間2022~2028年のCAGRは7%を記録すると予想されます。インドネシアの医療機器市場は、2027年までに28億3,000万米ドルに達すると予測されています。これらの要因によって、予測期間中にアジア太平洋におけるシアノアクリレート接着剤の需要が高まると予想されます。

アジア太平洋のシアノアクリレート接着剤市場の動向

電気自動車の普及が産業を牽引

- アジア太平洋の自動車産業は、自動車販売台数が大幅に増加していることから、市場を牽引する産業の一つとなっています。中でも中国が最大の自動車生産国であり、同地域の生産量の約57%を占めています。次いで日本が17%、インドが10%、韓国が8%となっています。

- この地域の自動車販売台数は生産台数とともに大きく減少しており、そのために接着剤の利用が影響を受けています。2017~18年の前年比変動は-1.8%であったが、2018~19年はさらに-6.4%減少しました。2019~20年には、地域の生産は再びマイナスの影響を受け、COVID-19の流行により前年比-10.2%を記録しました。製造施設の操業停止とサプライチェーンの混乱による自動車部品の不足が生産水準を制約しました。しかし、2021年には自動車需要が再び増加し、今後も続くと予想されるため、予測期間中は地域全体で接着剤の利用が増加します。

- アジア太平洋のEV市場は、接着剤市場にとってもう一つの成長機会となります。EVとハイブリッド車の生産台数と採用台数の増加が、自動車の電子部品組立用接着剤の使用量を押し上げています。中国はEVの世界最大の生産国であると同時に、この地域全体でも最大の生産国です。2016~2021年にかけて、商用電気自動車の台数は562,603台から1,116,382台に増加し、約98%の成長率を記録しました。これらの要因によって接着剤の需要が増加し、予測期間中の市場成長率が高まると予想されます。

アジア太平洋における家具メーカーの高い存在感が産業を牽引

- アジア太平洋では、中国が最大の家具製造・輸出・消費国です。中国の家具消費量が多いのは、人口が多く、都市部の世帯の可処分所得が増加しているためです。世界の家具貿易の35%以上が中国からもたらされており、世界の金属製家具輸出の40%、布張りの木製と金属製シートの60%以上が中国で生産されています。

- 米国との利害対立にもかかわらず、中国の家具市場は2017年から19年にかけて約18%成長しました。アジア太平洋では、COVID-19パンデミックに起因する操業、貿易、サプライチェーンの制限により、家具産業は2020年に約7%の減少を示しました。しかし、家具産業は中国、インド、日本などの国々からの需要増に伴い、パンデミック以前の水準まで回復しました。2022年、中国は690億米ドル相当の家具を世界に輸出しました。

- インドは世界第5位の家具生産国です。2017~2019年にかけて家具製造業が健全な成長を遂げたのは、インドの家庭における可処分所得の増加、中間所得層の増加、都市化の着実な進展といった要因があるからです。インドの家具製造業は大部分が未組織であり、インド政府はその潜在力を認め、チャンピオンセクタと命名しました。国内家具生産の着実な成長を確保するため、構造的な方法で組織化し、規制する努力がなされています。

- 中国、インド、日本などの国々における木工・建具セクタの著しい成長により、予測期間(2022~2028年)中、同市場は数量ベースで約4.2%のCAGRで推移すると予想されます。

アジア太平洋のシアノアクリレート接着剤産業概要

アジア太平洋のシアノアクリレート接着剤市場はセグメント化されており、上位5社で31.95%を占めています。この市場の主要企業は、3M、Aica Kogyo、H.B. Fuller Company、Henkel AG & Co. KGaA、Pidilite Industries Ltd.などがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- エンドユーザー動向

- 航空宇宙

- 自動車

- 建築・建設

- フットウェア皮革

- 木工・建具

- 規制の枠組み

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- マレーシア

- シンガポール

- 韓国

- タイ

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- エンドユーザー産業

- 航空宇宙

- 自動車

- 建築・建設

- フットウェアと皮革

- 医療

- 木工・建具

- その他

- 技術

- 反応性

- UV硬化型接着剤

- 国名

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- マレーシア

- シンガポール

- 韓国

- タイ

- その他のアジア太平洋

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- 3M

- Aica Kogyo Co..Ltd.

- Arkema Group

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Hubei Huitian New Materials Co. Ltd

- Kangda New Materials(Group)Co., Ltd.

- NANPAO RESINS CHEMICAL GROUP

- Pidilite Industries Ltd.

- ThreeBond Holdings Co., Ltd.

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界の接着剤・シーラント産業概要

- 概要

- ファイブフォース分析フレームワーク(産業魅力度分析)

- 世界のバリューチェーン分析

- 促進要因、抑制要因、機会

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 92478

The Asia-Pacific Cyanoacrylate Adhesives Market size is estimated at 1.19 billion USD in 2024, and is expected to reach 1.48 billion USD by 2028, growing at a CAGR of 5.57% during the forecast period (2024-2028).

The rising applications and demand for cyanoacrylate adhesives across the aerospace and healthcare industries are the major growth factors

- Asia-Pacific's cyanoacrylate adhesives market is likely to dominate by other end-user industries owing to rapidly increasing demand from DIY and electronics applications throughout the projected timeframe. Cyanoacrylates have unique characteristics to create an exceptional bond in a shorter time period with different substrates such as wood, metal, plastics, ceramics, and elastomers, which make them suitable to be used by professionals in the DIY sector.

- Cyanoacrylate adhesive consumption has recently increased for automotive due to rising applications of critical assembly operations across the industry. Cyanoacrylates offer a permanent bond that can be stable under a wide range of heat and temperature. Moreover, automotive manufacturers are engaging themselves in producing lightweight parts and components to reduce the overall vehicle's weight without sacrificing safety. Thus, cyanoacrylate adhesives consumption in the automotive industry will showcase significant growth in the upcoming years.

- The aerospace industry is likely to witness a fastest-growing sector in terms of cyanoacrylate consumption owing to its non-flammable, fast-curing ability, and hassle-free applications in mechanical and structural operations. In addition, cyanoacrylates are rapidly adopted as a tissue adhesive for a variety of medical and surgical applications to replace traditional suturing processes. Furthermore, oral applications of cyanoacrylates have exhibited continuous improvements over the last few years. These factors collectively impetus the growth of cyanoacrylate adhesives across the Asia-Pacific region in the upcoming years.

High value growth forecasted for the cyanoacrylate adhesives led by the Indonesian healthcare industry

- Asia-Pacific is the world's largest regional consumer of cyanoacrylate adhesives, accounting for 42.9% of total cyanoacrylate adhesive consumption in 2021. Cyanoacrylate adhesives are instant adhesives consumed in the region's automotive, healthcare, DIY, and other industries.

- China is the largest consumer of cyanoacrylate adhesives in the region and the world. These adhesives are majorly used in the country's automotive and healthcare industries. The Chinese automotive industry consumes about 23,036 tons of cyanoacrylate adhesives. Automotive production is expected to reach 34.2 million units by 2025 from 26.2 million units in 2021. Such growing demand from the automotive industry is expected to drive the demand for cyanoacrylate adhesives in the country.

- Aerospace is the fastest-growing end-user industry of cyanoacrylate adhesives in the region and is expected to record a CAGR of 6.26% in volume terms during the forecast period 2022-2028. China is implementing the 'Made in 2025' plan, which requires aircraft manufacturers to source and manufacture 100% of aircraft in China, restricting foreign players' entry. On the other hand, the local aerospace adhesives and sealants manufacturers are expected to benefit from this government scheme. Similar policies being implemented by other countries in the region are expected to boost the aerospace industry in the region.

- Indonesia is the fastest-growing country in the region and globally for the market and is expected to record a CAGR of 7% during the forecast period 2022-2028, owing to its growing healthcare industry. The medical device market in Indonesia is expected to reach USD 2.83 billion by 2027. These factors are expected to boost the demand for cyanoacrylate adhesives in the Asia-Pacific region over the forecast period.

Asia-Pacific Cyanoacrylate Adhesives Market Trends

Increasing adoption of electric vehicles to drive the industry

- The Asia-Pacific automotive industry is one of the leading industries in the market, as the sales of automotive vehicles are largely increasing. Among all the countries, China is the largest automotive producer, accounting for about 57% of the regional production, followed by Japan with 17%, India with 10%, and South Korea with 8%.

- Vehicle sales in the region have majorly declined along with production, owing to which the utilization of adhesives has been impacted. While the Y-o-Y variation in 2017-18 was -1.8%, it fell further by -6.4% in 2018-19. In 2019-20, regional production was again impacted negatively and recorded a -10.2% decline from the previous year due to the COVID-19 pandemic. The shutdown of manufacturing facilities and the shortage of vehicle components due to disruptions in the supply chain constrained the production level. However, in 2021, the demand for automobiles rose again and is expected to continue, thereby increasing the utilization of adhesives across the region over the forecast period.

- The EV market in Asia-Pacific offers another opportunity for the adhesives market to grow. The rising production and adoption of EVs and hybrid vehicles are boosting the usage of adhesives for electronic component assembly in vehicles. China is the largest producer of EVs globally as well as across the region. From 2016 to 2021, the volume of commercial electric vehicles increased from 562,603 to 1,116,382 units, recording a growth rate of about 98%. These factors are expected to increase the demand for adhesives and result in the higher market growth over the forecast period.

High presence of furniture manufacturers in the Asia-Pacific region will propel the industry

- In Asia-Pacific, China is the largest furniture manufacturer, exporter, and consumer. China's high furniture consumption is due to its large population and the growing disposable income of urban households. More than 35% of the world's furniture trade originates from China, and 40% of the world's metal furniture exports and over 60% of upholstered wooden and metal seats are produced in China.

- The Chinese furniture market grew by around 18% during 2017-19 despite the conflict of interests with the United States. In Asia-Pacific, the furniture industry witnessed a decline of around 7% in 2020 due to the operational, trade, and supply chain restrictions resulting from the COVID-19 pandemic. However, the furniture industry has bounced back to its pre-pandemic levels in line with the rising demand from countries such as China, India, and Japan. In 2022, China exported USD 69 billion worth of furniture globally.

- India is the fifth largest producer of furniture in the world. The furniture manufacturing industry witnessed healthy growth from 2017 to 2019 because of factors like rising disposable income in Indian households, increasing middle-income families, and steady growth in urbanization. The Indian furniture manufacturing industry is largely unorganized, and the Indian government has recognized its potential and named it a champion sector. Efforts are being made to organize and regulate it in a structured way to ensure steady growth in domestic furniture production.

- Owing to the significant growth in the woodworking and joinery sector in countries like China, India, and Japan, the market is expected to register a CAGR of around 4.2% in terms of volume during the forecast period (2022-2028).

Asia-Pacific Cyanoacrylate Adhesives Industry Overview

The Asia-Pacific Cyanoacrylate Adhesives Market is fragmented, with the top five companies occupying 31.95%. The major players in this market are 3M, Aica Kogyo Co..Ltd., H.B. Fuller Company, Henkel AG & Co. KGaA and Pidilite Industries Ltd. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Footwear and Leather

- 4.1.5 Woodworking and Joinery

- 4.2 Regulatory Framework

- 4.2.1 Australia

- 4.2.2 China

- 4.2.3 India

- 4.2.4 Indonesia

- 4.2.5 Japan

- 4.2.6 Malaysia

- 4.2.7 Singapore

- 4.2.8 South Korea

- 4.2.9 Thailand

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Footwear and Leather

- 5.1.5 Healthcare

- 5.1.6 Woodworking and Joinery

- 5.1.7 Other End-user Industries

- 5.2 Technology

- 5.2.1 Reactive

- 5.2.2 UV Cured Adhesives

- 5.3 Country

- 5.3.1 Australia

- 5.3.2 China

- 5.3.3 India

- 5.3.4 Indonesia

- 5.3.5 Japan

- 5.3.6 Malaysia

- 5.3.7 Singapore

- 5.3.8 South Korea

- 5.3.9 Thailand

- 5.3.10 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 Aica Kogyo Co..Ltd.

- 6.4.3 Arkema Group

- 6.4.4 H.B. Fuller Company

- 6.4.5 Henkel AG & Co. KGaA

- 6.4.6 Hubei Huitian New Materials Co. Ltd

- 6.4.7 Kangda New Materials (Group) Co., Ltd.

- 6.4.8 NANPAO RESINS CHEMICAL GROUP

- 6.4.9 Pidilite Industries Ltd.

- 6.4.10 ThreeBond Holdings Co., Ltd.

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms