|

|

市場調査レポート

商品コード

1692498

フィリピンのデータセンター:市場シェア分析、産業動向、成長予測(2025年~2030年)Philippines Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| フィリピンのデータセンター:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 178 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

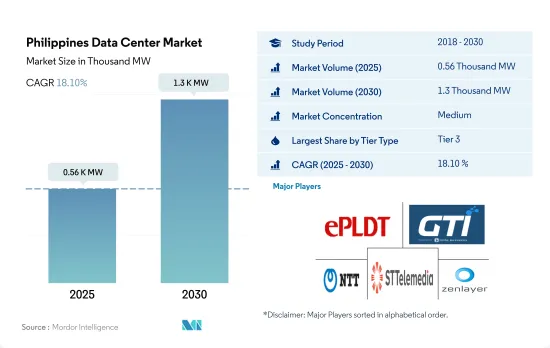

フィリピンのデータセンター市場規模は2025年に560kWと推定され、2030年には1,300kWに達すると予測され、CAGRは18.10%で成長します。

また、2025年には3億9,200万米ドルのコロケーション収益が見込まれ、2030年には11億6,200万米ドルに達すると予測され、予測期間中(2025年~2030年)のCAGRは24.27%です。

2023年にはティア3データセンターが数量ベースで大半のシェアを占めるが、予測期間を通じてティア4が最も急成長しています。

- ティア1セグメントの成長は、施設の信頼性の低さやダウンタイムの長さから停滞が予想されます。ティア2セグメントのIT負荷容量は、CAGR 4.33%で2021年の125.6MWから2029年には172.6MWに増加すると予想されます。これらのデータセンターは、手頃なコストで提供されるパフォーマンスにより、主に中小企業に好まれています。しかし、年間22時間のダウンタイムが発生するため、企業はデータセンターを選択することに消極的で、躊躇することもあります。

- フィリピンのデータセンター市場におけるティア3セグメントのIT負荷容量は、CAGR 25.75%で2021年の78.3MWから2029年には489.3MWに増加すると予想されています。これらのデータセンターは、N+1冗長化により99.98%のアップタイムを提供し、1年間のダウンタイムはわずか1.6時間程度です。これらの利点により、大企業に非常に好まれています。

- 現在、この地域ではティア3データセンターが非常に普及しており、一部の施設では構造やサービスを必要な水準までアップグレードしています。事業者は、新しく建設される施設がティア3やティア4に対応していることを好みます。

- フィリピンのデータセンター市場におけるティア4セグメントのIT負荷容量は、2029年までに70MWに達すると予想されています。これらのデータセンターは2023年に稼働が開始される見込みで、高い信頼性と約26.3分という低いダウンタイムが好まれています。現在、フィリピンにはTier 4認証を受けたコロケーション施設はないです。しかし、ePLDTはサンタロサにある11番目のデータセンターをティア4にし、2023年までに稼働させると発表しました。

- 新しいデータセンターの運営者は、高い信頼性を提供するため、インフラ施設にTier 4グレードの認証を好みます。

フィリピンのデータセンター市場動向

フィリピンの消費者は1日10時間をスマートフォンで過ごし、毎日大量のデータ転送を行う。

- 2022年のフィリピンのスマートフォンユーザー数は約1億100万人で、2029年にはCAGR 8.79%で1億8,100万人に達すると予想されています。

- パンデミック後、スマートフォンはブラウジング、金融取引、オンラインショッピングなどに便利であることが判明したため、需要が大幅に増加しました。人々は都会的なライフスタイルを採用し、家庭内のオートメーション機能、オンラインゲーム、ストリーミングコンテンツ、ニュース閲覧、オンラインショッピングなどにこれらのガジェットを使用しています。ほとんどすべてのことが即座にできる利便性が利用者数を増やし、人口の増加とともに増加すると予想されています。

- フィリピンは世界で唯一、ユーザーが1日平均10時間も電話を使う国です。通信ネットワークが開発され、設備が改善されるにつれて、ユーザーはスマートフォンで良好なモバイルデータ通信速度を達成できるようになり、機能性と体験が向上しました。モバイルのオンラインゲームはその質を向上させ、オンラインゲームが主催するイベントはスマートフォンの需要をさらに高めました。より高いプロセッサー、より良いディスプレイ、バッテリーを搭載した携帯電話が格安価格で入手できるようになったからです。ユーザーの74%がPCやコンソールゲームよりもモバイルゲームを好みます。

DITO、Globe、Smartなどのモバイル事業者による5Gネットワークの拡大がデータセンター市場を後押し

- フィリピンの消費者は現在、4Gと3Gサービスを大きな割合で利用しています。5Gネットワークサービスは2021年末に開始され、2022年第1四半期には顧客による導入が進んでいます。

- フィリピンで5Gサービスを提供している施設は、DITO、Globe、Smartです。これらの企業はネットワーク接続を強化するために拠点を拡大しています。

- 例えば、Smartは5Gネットワークを強化するため、2022年に5G変電所の数を7300に増やしました。

フィリピンのデータセンター産業概要

フィリピンのデータセンター市場は適度に統合されており、上位5社で54.17%を占めています。同市場の主要企業は以下の通り。 ePLDT Inc., GTI Corporation, NTT Ltd, STT GDC Pte Ltd and Zenlayer Inc.(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 市場展望

- 耐荷重

- 床面積

- コロケーション収入

- 設置ラック数

- ラックスペース利用率

- 海底ケーブル

第5章 主要業界動向

- スマートフォンユーザー数

- スマートフォン1台当たりのデータトラフィック

- モバイルデータ速度

- ブロードバンドデータ速度

- 光ファイバー接続ネットワーク

- 規制の枠組み

- フィリピン

- バリューチェーンと流通チャネル分析

第6章 市場セグメンテーション

- ホットスポット

- NCR(メトロマニラ)

- その他の地域

- データセンターの規模

- 大規模

- 大規模

- 中規模

- メガ

- 小規模

- ティアタイプ

- ティア1と2

- ティア3

- ティア4

- 吸収量

- 非利用

- 利用

- コロケーションタイプ別

- ハイパースケール

- リテール

- ホールセール

- エンドユーザー別

- BFSI

- クラウド

- eコマース

- 政府機関

- 製造業

- メディア&エンターテイメント

- テレコム

- その他エンドユーザー

第7章 競合情勢

- 市場シェア分析

- 企業情勢

- 企業プロファイル.

- Bitstop

- Dataone

- ePLDT Inc.

- GTI Corporation

- NTT Ltd

- Space DC Pte Ltd

- STT GDC Pte Ltd

- VSTECS Phils Inc.

- Zenlayer Inc.

- LIST OF COMPANIES STUDIED

第8章 CEOへの主な戦略的質問

第9章 付録

- 世界の概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 世界市場規模とDRO

- 情報源と参考文献

- 図表リスト

- 主要洞察

- データパック

- 用語集

The Philippines Data Center Market size is estimated at 0.56 thousand MW in 2025, and is expected to reach 1.3 thousand MW by 2030, growing at a CAGR of 18.10%. Further, the market is expected to generate colocation revenue of USD 392 Million in 2025 and is projected to reach USD 1,162 Million by 2030, growing at a CAGR of 24.27% during the forecast period (2025-2030).

Tier 3 data center accounted for majority share in terms of volume in 2023, Tier 4 is fastest growing through out the forecasted period

- Growth in the tier 1 segment is expected to be stagnant due to the unreliability and longer downtimes of facilities. The IT load capacity of the tier 2 segment is expected to increase from 125.6 MW in 2021 to 172.6 MW by 2029 at a CAGR of 4.33%. These data centers are preferred mainly by small businesses due to the performance they offer at an affordable cost. However, a downtime of 22 hours annually, at times, makes companies reluctant and hesitant to opt for them.

- The IT load capacity of the tier 3 segment of the data center market in the Philippines is anticipated to increase from 78.3 MW in 2021 to 489.3 MW by 2029 at a CAGR of 25.75%. These data centers offer an uptime of 99.98% with N+1 redundancies, and they only have around 1.6 hours of downtime in a year. These advantages have made them highly preferable by large businesses.

- Currently, tier 3 data centers are highly prevalent in the region, as some facilities have upgraded their structures and services to the required standards. Operators prefer newly constructed facilities to be tier 3 and tier 4 ready.

- The IT load capacity of the tier 4 segment of the data center market in the Philippines is expected to reach 70 MW by 2029. These data centers are expected to be operational in 2023 and are preferred due to their high reliability and lower downtime of around 26.3 minutes. Currently, the Philippines has no colocation facility with Tier 4 certification. However, ePLDT announced that its 11th data center in Santa Rosa would be tier 4 and would be launched by 2023.

- Operators of new data centers prefer Tier 4 grade certifications for their infrastructure facilities due to the high reliability offered.

Philippines Data Center Market Trends

Philippines consumers spends 10hr/day on smartphone, generating huge amount of data transfer daily, this would drive data center market

- The Philippines had around 101 million smartphone users in 2022, which is expected to reach 181 million by 2029 at a CAGR of 8.79%.

- Post-pandemic, the demand for smartphones has significantly increased as they turned out to be useful for browsing, financial transactions, online shopping, and others. People are adopting urban lifestyles and use these gadgets for automation functions in their homes, online gaming, streaming content, browsing news, and online shopping. The convenience of doing almost everything instantly has increased the number of users and is expected to increase with the increasing population.

- The Philippines is the only country in the world where users, on average, spend an average of 10 hours a day on the phone. As the telecom network developed and improved its facilities, users could attain good mobile data speeds on their smartphones which increased their functionality and experience. Online games on mobile have improved their quality, and the events organized by them have furthermore increased the demand for smartphones. As phones with higher processors, better displays, and batteries are available at a budget price. 74% of the users prefer mobile gaming over PC and console gaming.

Expansion of 5G network by mobile operators such as DITO, Globe, and Smart boost the data center market

- Consumers in the Philippines currently use 4G and 3G services in greater proportion. 5G network services were launched at the end of 2021 and were increasingly adopted by customers in the first quarter of 2022.

- Facilities offering 5G services in the Philippines are DITO, Globe, and Smart. These companies are expanding their bases to strengthen their network connectivity.

- For instance, Smart increased the count of its 5G substations to 7300 in 2022 to strengthen its 5G networks.

Philippines Data Center Industry Overview

The Philippines Data Center Market is moderately consolidated, with the top five companies occupying 54.17%. The major players in this market are ePLDT Inc., GTI Corporation, NTT Ltd, STT GDC Pte Ltd and Zenlayer Inc. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 MARKET OUTLOOK

- 4.1 It Load Capacity

- 4.2 Raised Floor Space

- 4.3 Colocation Revenue

- 4.4 Installed Racks

- 4.5 Rack Space Utilization

- 4.6 Submarine Cable

5 Key Industry Trends

- 5.1 Smartphone Users

- 5.2 Data Traffic Per Smartphone

- 5.3 Mobile Data Speed

- 5.4 Broadband Data Speed

- 5.5 Fiber Connectivity Network

- 5.6 Regulatory Framework

- 5.6.1 Philippines

- 5.7 Value Chain & Distribution Channel Analysis

6 MARKET SEGMENTATION (INCLUDES MARKET SIZE IN VOLUME, FORECASTS UP TO 2030 AND ANALYSIS OF GROWTH PROSPECTS)

- 6.1 Hotspot

- 6.1.1 NCR (Metro Manila)

- 6.1.2 Rest of Philippines

- 6.2 Data Center Size

- 6.2.1 Large

- 6.2.2 Massive

- 6.2.3 Medium

- 6.2.4 Mega

- 6.2.5 Small

- 6.3 Tier Type

- 6.3.1 Tier 1 and 2

- 6.3.2 Tier 3

- 6.3.3 Tier 4

- 6.4 Absorption

- 6.4.1 Non-Utilized

- 6.4.2 Utilized

- 6.4.2.1 By Colocation Type

- 6.4.2.1.1 Hyperscale

- 6.4.2.1.2 Retail

- 6.4.2.1.3 Wholesale

- 6.4.2.2 By End User

- 6.4.2.2.1 BFSI

- 6.4.2.2.2 Cloud

- 6.4.2.2.3 E-Commerce

- 6.4.2.2.4 Government

- 6.4.2.2.5 Manufacturing

- 6.4.2.2.6 Media & Entertainment

- 6.4.2.2.7 Telecom

- 6.4.2.2.8 Other End User

7 COMPETITIVE LANDSCAPE

- 7.1 Market Share Analysis

- 7.2 Company Landscape

- 7.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 7.3.1 Bitstop

- 7.3.2 Dataone

- 7.3.3 ePLDT Inc.

- 7.3.4 GTI Corporation

- 7.3.5 NTT Ltd

- 7.3.6 Space DC Pte Ltd

- 7.3.7 STT GDC Pte Ltd

- 7.3.8 VSTECS Phils Inc.

- 7.3.9 Zenlayer Inc.

- 7.4 LIST OF COMPANIES STUDIED

8 KEY STRATEGIC QUESTIONS FOR DATA CENTER CEOS

9 APPENDIX

- 9.1 Global Overview

- 9.1.1 Overview

- 9.1.2 Porter's Five Forces Framework

- 9.1.3 Global Value Chain Analysis

- 9.1.4 Global Market Size and DROs

- 9.2 Sources & References

- 9.3 List of Tables & Figures

- 9.4 Primary Insights

- 9.5 Data Pack

- 9.6 Glossary of Terms