|

市場調査レポート

商品コード

1692463

バス用パンタグラフ充電器:市場シェア分析、産業動向・統計、成長予測(2025~2030年)Bus Pantograph Charger - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| バス用パンタグラフ充電器:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 109 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

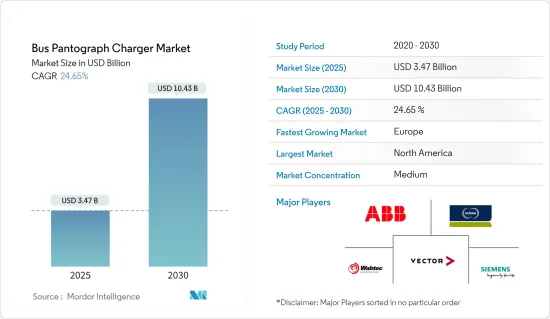

バス用パンタグラフ充電器市場規模は2025年に34億7,000万米ドルと推定・予測され、予測期間(2025年~2030年)のCAGRは24.65%で、2030年には104億3,000万米ドルに達すると予測されています。

COVID-19は、2020年上半期のバス用パンタグラフ充電器市場に深刻な影響を及ぼし、ロックダウンや規制によって輸送機関やその他の関連セクターからの需要が減少しました。さらに、電気バスプロジェクトの遅延やサプライチェーンの混乱が市場の状況を悪化させました。しかし、大半の自動車メーカーとEV充電プロバイダーは、限定的な生産と必要な措置を講じてパンタグラフ式充電器の生産を再開しました。電気バスの販売台数は2020年後半から大きく伸びており、予測期間中も続くとみられます。これが予測期間中の注目市場を牽引すると予想されます。

中期的には、パンタグラフ式充電器の需要は、世界の主要国において、乗り換え用だけでなく、学童輸送用としても電気バスの採用が拡大していることから、持ち直すと予想されます。さらに、政府投資の拡大と充電インフラ整備への注力は、予測期間中の市場の需要を促進すると予想されます。さらに、各社による充電ステーション市場の新たな開拓も成長を後押しすると予想されます。例えば

主なハイライト

- 2021年10月、オーストラリアの大手バスメーカーであるCustom Denning社は、シーメンスを選び、Sicharge UC管理ソリューションと充電ステーションを提供しました。現在試験中のこの技術は、同メーカーの次期電気バスを支援します。最大1,000ボルトで動作し、出力範囲は50~600kWです。

さらに、主要企業からの投資や、充電ソリューション・プロバイダーとバス・メーカー間の戦略的協力関係の拡大は、市場で活動する企業に新たな機会を提供すると予想されます。バッテリーのコスト低下により、電気バス充電システムの利用が急増しています。温室効果ガス(GHG)排出削減への取り組みの高まりは、政府による規制の強化とともに、予測期間中の市場の成長を促進すると思われます。

主なハイライト

- 2022年6月、カナダ太平洋経済開発庁は、ブリティッシュ・コロンビア州の運輸・インフラストラクチャー大臣と共同で、ブリティッシュ・コロンビア州の公共交通サービスを改善するための連邦政府共同資金による3億1,200万米ドルの投資計画を発表しました。このアップグレードには、新しいトランジット・インターチェンジの建設とバス車両の電化が含まれます。

北米地域は、同地域の主要国で電気バスの採用が増加していることから、予測期間中に大きな成長が見込まれています。さらに、中国とインドは、政府、交通機関、その他のグリーンビークルを支援するコミュニティや組織からの強い後押しにより、アジア太平洋地域の成長に貢献すると予想されます。

主なハイライト

- 2021年3月、デリー政府は同市のバス車両を増やすため、新たに300台の低床電気(AC)バスを購入する提案を承認しました。これらのバスはデリー交通公社に受け入れられました。118台のバスの最初のバッチは2021年10月に到着する予定で、さらに100台が11月に続く予定でした。すべての納入は2022年1月までに完了する予定でした。

バス用パンタグラフ充電器の市場動向

環境に優しいバスを重視する政府の増加

ディーゼルバスは今日、世界中で広く使用されています。さらに、これらのバスはほとんどが人口密度の高い都市で使用されており、他の汚染物質によって空気の質がすでに悪化しています。そのため、世界各国の政府は、環境にやさしい輸送を奨励することを目的とした、さまざまな規制と支援政策の開発に力を入れています。

米国のEPAとNHTSAは、2021年から2026年にかけてSAFE(Safer Affordable Fuel-Efficient Vehicles)規則を実施することを提案しました。この規則は、乗用車と商用車の企業平均燃費と温室効果ガス排出基準を定める可能性があります。OEMは、ゼロ・エミッション車(ZEV)計画のもと、一定数のクリーンなゼロ・エミッション車(電気自動車、ハイブリッド車、燃料電池を搭載した商用車および乗用車)を販売することが義務付けられています。同国のZEV計画は、2030年までに1,200万台のZEV(バスを含む)を走らせることを目標としています。

インド政府は、2030年までに自動車販売台数の30%を電動化する意向です。この戦略の一環として、政府は2022年までのFAME(ハイブリッド車・電気自動車の早期導入・製造)プログラムの第2段階に14億米ドルを投資すると発表しました。このフェーズでは、7,090台の電気バスに補助金を支給することで、インドの公共交通機関や共有交通機関の電化に重点を置いています。これにより、車両運行会社は電気バスに切り替えるようになりました。

さらに、公共交通は大気の質を改善することで、密集市街地における都市の持続可能性に貢献し、自家用車で何度も別々に移動する必要性を減らしています。こうした利点から、世界各国の政府は持続可能で効率的な公共バス輸送サービスを積極的に推進しており、市場にプラスの勢いが生まれると期待されています。例えば、

- 2022年11月、ロンドンのバス運行会社メトロライン(Metroline)は、都市間輸送用に39台の電気2階建てバスを購入すると発表しました。これらのバスを調達したのは、北アイルランドのバス・メーカー、ライトビウス社です。これら39台のバスは、ロンドンのブレント、イーリング、ハロー、バーネットの各自治区と、ロンドン北部のハートフォードシャーのワトフォードを297番線と142番線で走行する予定です。このバスは、CCS経由で最大300kW、パンタグラフ経由で最大420kWの充電能力を持っています。

- 2022年3月、イタリアのカリアリで最先端の電気バス・コンセプトが発表され、バス・メーカーのランピーニが受注した7台のうちの最初の1台を納入しました。納入されたのは、パンタグラフを備えた6メートルのバッテリー電気バス6台です。欧州のバスにおけるこの新技術は確認されており、中期的に大きな関心を呼んでいます。

北米が市場で最も急成長する可能性が高い

北米は予測期間中、市場の成長において重要な役割を果たすと予想されます。さらに、米国は、いくつかの政府の取り組みと、全国的な電動スクールバスの人気の高まりにより、この地域の成長に大きく貢献する国のひとつとなる可能性が高いです。北米地域全体の電気バスの需要は、政府、自治体などの採用の増加によってサポートされると予想されます。例えば

- 2021年6月、ニューヨーク電力公社(NYPA)は、市の電気バス車両を充電するため、市内の様々なステーションに67台のパンタグラフ充電器を設置する3,000万米ドルの契約が完了したと発表しました。

- 2021年3月、メリーランド州のモンゴメリー郡公立学校は、ハイランド・エレクトリック・トランスポーテーション社との契約を承認しました。この契約に基づき、ハイランド・エレクトリック・トランスポーテーション社とそのパートナーであるトーマス・ビルト・バス社、プロテラ社、アメリカン・バス社は、モンゴメリー郡公立学校区に属する5つのバス発着所すべてを電気化し、電気バスと充電インフラを供給します。

さらに、電動モビリティへの移行が進む中、カナダ政府も国全体でネット・ゼロ・エミッションの交通産業の構築に取り組んでいます。例えば

- 2021年3月、インフラ・コミュニティ省とイノベーション・科学・産業省は、公共交通システムを改善し、よりクリーンな電力に移行させるため、2021年から5年間で27億5,000万カナダドル(~20億2,000万米ドル)の資金提供を発表し、これにはゼロエミッションの公共交通機関やスクールバスの購入資金も含まれます。

北米地域におけるこのような活発な成長は、いくつかの主要企業や電気バスインフラプロジェクトの企業がパンタグラフを採用することを促しており、したがって予測期間にわたってバスパンタグラフチャージャの需要を促進しています。例えば

- 2022年3月、ABBは米国最大の充電器配備を持つセントルイスの新しい電気バス車両にサービスを提供すると発表しました。ABBの逐次充電システムは、150kWの電力を持つ20台のプラグイン・デポ充電器と3台の追加パンタグラフ充電器で構成されています。

したがって、上記の開発・事例から、北米地域が予測期間中、他の地域と比較して最も速い成長を遂げると推定されます。

バス用パンタグラフ充電器産業の概要

バス用パンタグラフ充電器市場の主要企業には、ABB Ltd.、Wabtec Corporation、Schunk Transit Systems GmBH、BYDなどがあります。バスのパンタグラフ充電器市場は適度に統合されており、いくつかの世界的および地域的な企業が占めています。製品革新、合弁事業、中小企業の買収、製品発売は、主要企業が展開する主要戦略です。さらに、世界中の様々な政府によるイニシアチブも市場の成長を支えています。例えば、

- 2022年6月、カナダ・インフラストラクチャー銀行とダラム地域自治体との間で覚書が締結され、CIBがダラム・リージョン・トランジット(DRT)の購入注文を支援するために最大5,310万米ドルを投資することが結論付けられました。輸送車両の電化イニシアチブは、今後25年間にわたる地域の気候変動公約を達成するための重要なステップです。

- 2021年12月、ベルリン交通局(BVG)の監査役会は、さらに90台の電気バスの購入を承認しました。車両は全長12メートルのバッテリー単機で、車両基地で充電されるため、今後数年間で全国で使用されるパンタグラフ充電システムの需要が高まる。

上記の電気バスの開発は、電気バス用充電ステーションの需要をさらに押し上げる可能性があります。これらの戦略とは別に、バスのパンタグラフ充電器は、市場での地位を強化するために、主要なバスメーカーや充電ステーションプロバイダーと供給契約を結んでいます。例えば

- 2022年12月、Solaris Bus &Coach Sp. z o.o.は、ラトビアの運行会社Rgas Satiksmeに35台のSolaris Urbino 12電気バスを供給することに合意しました。これらのバスには、容量140kWhのソラリス・ハイエナジー・バッテリーが搭載され、プラグイン・コネクターと反転パンタグラフを介して充電される予定です。このバスには、ゼロ・エミッションバス車両を管理するためのeSConnectシステムも搭載されます。ソラリスの専門家が作成したこのソフトウエアは、車両データへのリアルタイム・アクセスを提供するだけでなく、不具合が発生した場合の特定も可能にします。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 市場抑制要因

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 充電タイプ別

- レベル1

- レベル2

- 直流急速充電

- 部品タイプ別

- ハードウェア

- ソフトウェア

- 充電インフラタイプ別

- オフボード・トップダウン・パンタグラフ

- オンボード・ボトムアップ・パンタグラフ

- 地域別

- 北米

- 米国

- カナダ

- その他の北米

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- インド

- 中国

- 韓国

- 日本

- その他のアジア太平洋

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- ABB Ltd

- Schunk Transit Systems GmBH

- Wabtech Corporation

- Siemens Mobility

- Vector Informatik GmbH

- SETEC Power

- SCHUNK GmbH & Co. KG

- Valmont Industries, Inc.

- Comeca Group

第7章 市場機会と今後の動向

The Bus Pantograph Charger Market size is estimated at USD 3.47 billion in 2025, and is expected to reach USD 10.43 billion by 2030, at a CAGR of 24.65% during the forecast period (2025-2030).

COVID-19 has severely affected the bus pantograph charger market for the first half of the year 2020, as lockdowns and restrictions resulted in reduced demand from transportation and other associated sectors. Furthermore, delays in electric bus projects and supply chain disruptions worsened the situation in the market. However, the majority of the automakers and EV charging providers resumed pantograph charger production with limited production and necessary measures. The sales of electric buses witnessed significant growth since the latter half of the year 2020 and are likely to continue during the forecast period. This is anticipated to drive the market in focus during the forecast period.

Over the medium term, the demand for pantograph chargers is expected to be picked up by the growing adoption of electric buses, not only for transit but also for school children's transportation across major countries in the world. Furthermore, growing government investments and their focus on improving charging infrastructure are expected to drive demand in the market during the forecast period. Moreover, a new development in the charging station market by the companies is also expected to support the growth. For instance,

Key Highlights

- In October 2021, Custom Denning, one of Australia's leading bus manufacturers, chose Siemens to provide its Sicharge UC management solution and charging stations. The technology, which is currently being tested, will aid the manufacturer's upcoming electric buses. It can operate at up to 1,000 volts and has a power range of 50 to 600 kW.

In addition, investments from the key players and growing strategic collaborations between charging solution providers and bus manufacturers are anticipated to offer new opportunities for players operating in the market. There is a surge in the utilization of electric bus charging systems owing to the decreasing cost of batteries. The growing efforts to reduce greenhouse gas (GHG) emissions, along with the rise in favorable government regulations, are likely to enhance the growth of the market over the forecast period. For instance,

Key Highlights

- In June 2022, the Pacific Economic Development Agency of Canada, in collaboration with British Columbia's Minister of Transportation and Infrastructure, announced a USD 31,2 million investment plan under their joint federal funding for improving public transportation services in British Columbia. The upgrade includes the construction of new transit interchanges as well as the electrification of the bus fleet.

North American region is expected to grow at a significant rate during the forecast period owing to the rising adoption of electric buses across major countries in the region. Furthermore, China and India are expected to contribute to growth in the Asia-Pacific region owing to strong encouragement from the governments, transit agencies, as well as other green vehicle-supporting communities and organizations.

Key Highlights

- In March 2021, the Delhi government approved a proposal to purchase 300 new low-floor electric (AC) buses to increase the city's bus fleet. These buses have been accepted by the Delhi Transport Corporation. The first batch of 118 buses was scheduled to arrive in October 2021, with another 100 following in November. The entire delivery was supposed to be finished by January 2022.

Pantograph Bus Charger Market Trends

Rising Emphasis of Government on Eco-Friendly Buses

Diesel buses are widely used today all over the world. Furthermore, these buses are mostly used in densely populated cities, where air quality has already been degraded by other pollutants. As a result, governments across the world are focusing on developing a variety of regulations and supportive policies aimed at encouraging environmentally friendly transportation.

The EPA and NHTSA in the United States proposed implementing the Safer Affordable Fuel-Efficient (SAFE) vehicles rule from 2021 to 2026. The rule may establish corporate average fuel economy and greenhouse gas emissions standards for passenger and commercial vehicles. OEMs are required to sell a certain number of clean and zero-emission vehicles (electric, hybrid, and fuel cell-powered commercial and passenger vehicles) under the Zero-emission Vehicles (ZEV) Program. The country's ZEV plan aims to put 12 million ZEVs (including buses) on the road by 2030.

The Indian government intends to electrify 30% of total vehicle sales by 2030. As part of this strategy, the government announced a USD 1.4 billion investment in phase two of the FAME (Faster Adoption and Manufacturing of Hybrid and Electric Vehicles) program through 2022. This phase focuses on electrifying public and shared transportation in India by subsidizing 7090 electric buses. This has prompted fleet operators to switch to electric buses.

Moreover, by improving air quality, public transportation contributes to the sustainability of a city in dense urban areas, reducing the need for multiple separate trips by private vehicle. Because of these advantages, governments around the world are actively promoting sustainable and efficient public bus transportation services, which are expected to create positive momentum in the market. For instance,

- In November 2022, Metroline, a potential London bus operator, announced the purchase of 39 electric double-decker buses for intercity transit. Wrightbius, a Northern Irish bus manufacturer, procured these buses. These 39 buses are expected to travel through the London boroughs of Brent, Ealing, Harrow, and Barnet, as well as Watford in Hertfordshire, north of London, on the 297 and 142 routes. The buses have charging capabilities of up to 300 kW via CCS or 420 kW via pantographs.

- In March 2022, a cutting-edge electric bus concept was unveiled in Cagliari, Italy, where bus manufacturer Rampini delivered the first of seven vehicles ordered. The delivery consists of six 6-meter battery-electric buses with pantographs. This new technology in European buses has been identified, and it has generated a lot of interest in the medium term.

North America Likely to Have Fastest Growth in the Market

North America is expected to play a key role in the growth of the market over the forecast period. Furthermore, the United States is likely to be one of the major contributors to growth in the region, owing to several government initiatives and the growing popularity of electric school buses across the country. The demand for electric buses across the North American region is anticipated to be supported by the growing adoption of governments, municipalities, etc. For instance,

- In June 2021, the New York Power Authority (NYPA) announced the completion of a USD 30 million agreement to install 67 pantograph chargers across various stations in the city to charge the city's electric bus fleet.

- In March 2021, the Montgomery County Public School system in Maryland approved a contract with Highland Electric Transportation to convert its school bus fleet to a fully electric fleet, beginning with converting 326 school buses through 2025. Based on the contract, Highland Electric Transportation and its partners, Thomas Built Buses, Proterra, and American Bus, will electrify all five bus depots belonging to the Montgomery County Public School district and supply electric buses and charging infrastructure.

Moreover, with the increasing transition to electric mobility, the Canadian government is also working to build a net-zero emissions transportation industry across the country. For instance,

- In March 2021, the Infrastructure and Communities Ministry and the Ministry of Innovation, Science, and Industry announced CAD 2.75 billion (~USD 2.02 billion) in funding over five years, beginning in 2021, to improve public transportation systems and transition them to cleaner electrical power, including funding for the purchase of zero-emission public transportation and school buses.

Such active growth in the North American region is encouraging several key players and the players in electric bus infrastructure projects to adopt pantographs, thus driving demand for bus pantograph chargers over the forecast period. For instance,

- In March 2022, ABB announced that it is offering its services to St. Louis's new electric bus fleet with the largest deployment of chargers in the United States. ABB's sequential charging system consists of 20 plug-in depot chargers with 150 kW of power and three additional pantograph chargers.

Therefore, based on the above-mentioned developments and instances, it is estimated that the North American region is likely to have the fastest growth compared to its counterparts over the forecast period.

Pantograph Bus Charger Industry Overview

Some of the leading electric bus charging infrastructure market players are ABB Ltd., Wabtec Corporation, Schunk Transit Systems GmBH, BYD, and others. The bus pantograph charger market is moderately consolidated and accounts for several global and regional players. Product innovation, joint ventures, acquisitions of smaller players, and product launches are the key strategies deployed by the major players. Moreover, initiatives taken by various governments across the world are also supporting the growth of the market. For instance,

- In June 2022, a Memorandum of Understanding was signed between the Canada Infrastructure Bank and the Regional Municipality of Durham, which concluded that CIB would invest up to USD 53.1 million to support Durham Region Transit's (DRT) purchase order, which included 100 battery-electric buses to be delivered to Durham by the end of 2027. The initiative to electrify transit vehicles is a critical step toward meeting the region's climate change commitments over the next 25 years.

- In December 2021, the Berliner Verkehrsbetriebe (BVG) supervisory board approved the purchase of 90 more electric buses. The vehicles are 12-meter-long battery monoplanes that will be charged in the depot, increasing demand for pantograph charging systems to be used across the country in the coming years.

The above-mentioned development in electric buses may further boost the requirement for charging stations for electric buses. Apart from these strategies, bus pantograph chargers are entering into supply agreements with key bus manufacturers and charging station providers to strengthen their position in the market. For instance,

- In December 2022, Solaris Bus & Coach Sp. z o.o. has agreed to supply 35 Solaris Urbino 12 electric buses to Latvian operator Rgas Satiksme. These buses are expected to have Solaris High Energy batteries with a capacity of 140 kWh that will be charged via a plug-in connector as well as an inverted pantograph. The buses will also include an eSConnect system for managing zero-emission bus fleets. This software, created by Solaris experts, provides real-time access to vehicle data as well as the identification of any faults as they occur.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value - USD Million)

- 5.1 By Charging Type

- 5.1.1 Level 1

- 5.1.2 Level 2

- 5.1.3 Direct Current Fast Charging

- 5.2 By Pcomponent Type

- 5.2.1 Hardware

- 5.2.2 Software

- 5.3 By Charging Infrastructure Type

- 5.3.1 Off-board top-down pantograph

- 5.3.2 On-Board Bottom-Up Pantograph

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 India

- 5.4.3.2 China

- 5.4.3.3 South Korea

- 5.4.3.4 Japan

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Aegentina

- 5.4.4.3 Rest of the South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of the Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 ABB Ltd

- 6.2.2 Schunk Transit Systems GmBH

- 6.2.3 Wabtech Corporation

- 6.2.4 Siemens Mobility

- 6.2.5 Vector Informatik GmbH

- 6.2.6 SETEC Power

- 6.2.7 SCHUNK GmbH & Co. KG

- 6.2.8 Valmont Industries, Inc.

- 6.2.9 Comeca Group