|

市場調査レポート

商品コード

1851037

自律型航空機:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Autonomous Aircraft - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 自律型航空機:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月27日

発行: Mordor Intelligence

ページ情報: 英文 125 Pages

納期: 2~3営業日

|

概要

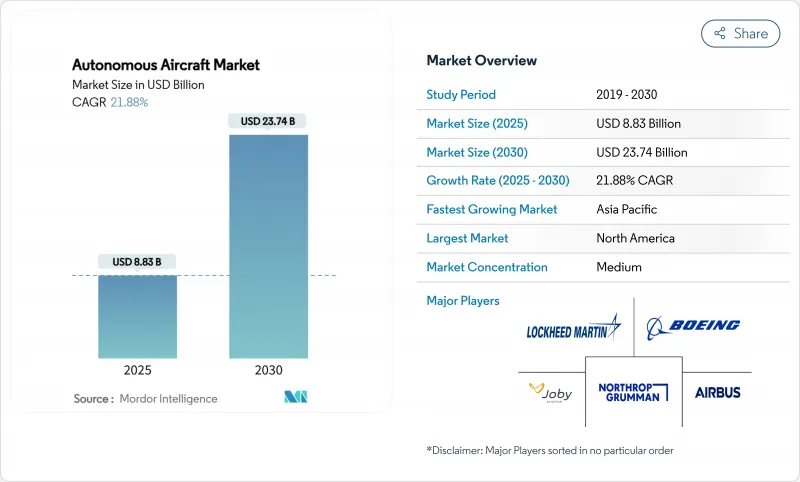

自律型航空機の市場規模は、2025年に88億3,000万米ドル、2030年には237億4,000万米ドルに達すると予測され、CAGRは21.88%と勢いがあります。

国防の近代化、都市移動計画、ロジスティクスの自動化の波が航空経済を再構築し、徐々に自己管理型プラットフォームへの需要を高めています。固定翼機構成が現在の主流を占めているが、航空会社や軍が汎用性の高い中距離のソリューションを選好していることを反映して、ハイブリッド固定翼VTOL機が成長曲線をリードしています。防衛機関による共同戦闘機やISR無人機への急速な投資は、技術の準備態勢を加速させる。同時に、アーバン・エアモビリティ(UAM)プログラムは、視線を超えたコリドーやバーティポートの建設を促進します。AIの統合の深化は、完全な自律運用を可能にし、貨物、旅客、特殊任務の各ユースケースで対応可能な範囲を広げます。従来型のタービン・エンジンは依然として主要な推進基盤であるが、持続可能性の義務付けが強化されるにつれて、水素燃料電池と先進的な電気システムに資本が集まっています。

世界の自律型航空機市場の動向と洞察

AI駆動飛行制御システムの進歩

リアルタイムの機械学習アルゴリズムが、パイロットの介入なしに戦術的操縦、障害物回避、ルート最適化を導きます。サーブの自律型グリペンEの試験では、戦闘機レベルのAIが瞬時の判断を実行し、ルールベースの自動化から適応的認知への移行を検証しています。2024年6月に発表されたFAAのAI安全保証ロードマップは、静的に訓練されたAIと継続的に学習するAIの認証段階を概説しており、民間航空機のための進歩の道を明確にしています。米国空軍の共同戦闘機のようなミリ秒単位の判断ループを要求する戦闘プログラムは、実績のあるアーキテクチャを商用システムに波及させ、貨物オペレーターや新興のエアタクシー・フリートが、ナビゲーション、センス・アンド・アボイド、ヘルス・モニタリング機能のための強化されたAIスタックを継承することを可能にします。

都市部における航空モビリティの急成長とeVTOLの採用

大都市計画担当者は、3次元モビリティを混雑緩和と地域連結性のテコとみなすようになっています。バーティカル・エアロスペース社は、2028年までにVX4の認証取得のためにハネウェル社から10億米ドルのアビオニクス受注を確約しており、これはサプライチェーンに対する信頼の証です。日本初のeVTOL路線は2028年の大阪万博をターゲットとしており、スカイドライブは300機以上の仮受注を獲得し、先進的な航空モビリティに対する国の優先順位を一致させています。アーバンエアポートのようなバーティポート開発業者が、エネルギー、メンテナンス、航空交通サービスをバンドルした200カ所を計画しているため、ネットワーク効果が増幅しています。規制のハードルが緩和される:EASAがVTOLパッケージを発表し、FAAのパワードリフト最終規則がパイロット免許を明確化したことで、滑走路のない航空機はスケールアップしたサービスへと向かっています。改善されたバッテリーと認証された自律性は、時間の節約によって割高な運賃を正当化できる、20~100マイルの都市間を移動するためのビジネスケースを支えます。

認証と空域統合における規制の複雑さ

従来の航空規則は、乗員を乗せない航空機に適合させるのに苦労しています。FAAは、2026年までに包括的なBVLOS規制を発表することを目標としており、現在の免除に基づく運航を日常的な商業レーンにまで拡大します。EASAの認証カテゴリーは、有人機と同様の型式証明と運航承認を要求しており、自律化プログラムを数年のタイムラインに引き延ばします。国境を越えるルートは、ハーモナイゼーションがまだ部分的であるため複雑さを増し、製造業者は並行して認可を追い求めることになります。航空交通の統合はさらに、従来のATCとシームレスにインターフェースしなければならない無人交通管理システムにかかっています。リソースに制約のある新興企業は、認証取得までの長い道のりの資金繰りに苦労することが多く、競争優位は既存の航空宇宙プライムに傾きます。

セグメント分析

2024年の自律型航空機市場の51.08%を固定翼機が占め、長距離ISRや貨物ミッションにおける空力効率と航続距離の優位性が強調されました。General Atomics社のMQ-20 Avengerのアップグレードは、レガシー機体に完全な自律性を持たせる改造が可能であることを証明し、能力を向上させながらライフサイクルコストを低く抑えることができます。しかし、ハイブリッド固定翼VTOLシステムのCAGRは26.89%であり、これは艦隊計画者が巡航性能を維持したまま滑走路に依存しない運用を望んでいることを示しています。都市ネットワークが、垂直上昇しながら200ノットの巡航速度を維持する航空機を要求しているため、ハイブリッドVTOLプラットフォームに付随する自律型航空機の市場規模は急激に拡大します。

ハイブリッドVTOLの成長は、ボーイングのMQ-25スティングレイのような防衛補給コンセプトからももたらされます。回転翼機は、救急救命や消火活動など、ホバリングを多用する作業においてニッチな役割を担っているが、ティルト・ローターやティルト・ウィング・アーキテクチャーは、現在、リーチを拡大しながら同様の垂直方向の器用さを提供しています。設計を組み合わせることで、広大な滑走路と密集した都市中心部のギャップを埋め、インフラの制約を緩和し、ミッションセットを拡大することができます。

2024年には、自律性が高まっていると分類されるプラットフォームが、アクティブな納入機の68.45%を占めるようになり、規制当局やオペレーターが急激な飛躍よりも段階的な機能アップグレードを好むことを反映しています。AeroVironment社のARKのような後付け可能なキットは、既存のフリートに高度な自律性を追加し、オペレータが新タイプの認証を取得せずに利点を収穫することを可能にします。完全自律型システムは、AIの信頼性、センサーフュージョン、クラウド接続が収束するにつれて、CAGR 27.75%で成長しています。

完全自律型船の自律型航空機市場規模は、監視された運用データを通じて規制当局の信頼が高まるにつれて拡大します。オプションで乗員を乗せる設計を採用する軍事プログラムは、知覚スタックに実世界のストレステストを提供し、技術の成熟を加速します。民間では、Joby AviationがXwingの自律性部門を買収したことで、旅客サービス向けのターンキーAIフライトデッキに資本が集まっていることが浮き彫りになりました。予測期間中、人間によるオン・ザ・ループ・ガバナンスは徐々に例外のみの介入に移行し、運航コストの削減と24時間365日稼働の拡大が進むと思われます。

地域分析

北米は2024年の世界売上高の37.23%を占める。米国防総省が戦闘機と高高度ISR無人機の共同開発に資金を提供することが国内需要を下支えする一方、FAAの規制主導がグローバルな認証経路を形成します。ボーイング、ロッキード・マーチン、ノースロップ・グラマンといった大手企業は、AIベンチャー企業と提携してパイロットレス戦闘機や宅配ドローンを開発し、大学からシリコンバレーの研究所に至る人材パイプラインを充実させています。カナダはアビオニクスと複合材製造で供給を強化し、メキシコは国境を越えたプログラムに供給するコスト効率の高い組立ラインを擁しています。自律型航空機の市場規模は、明確化されたBVLOSの枠組みのもとで防衛予算と都市モビリティ・パイロットが成熟するにつれて、さらに拡大し続けると思われます。

アジア太平洋は、2030年までのCAGRが24.37%で最も急成長している分野です。中国の低高度経済計画は、2025年までに1兆5,000億元の航空生産を目標としており、EHang社の合肥工場のようなeVTOL生産拠点に補助金を投入しています。日本では、2028年の大阪万博に合わせて商業用エアタクシーの就航を目指しており、バーティポートのゾーニングや自律飛行試験に関する官民協調にスポットライトが当てられています。韓国の仁川を中心とするバーティポート・グリッドとオーストラリアの電動エアタクシーの実現可能性研究は、地域的な実験を拡大します。インドの防衛研究開発奨励策と衛星接続性の向上は、遠隔地における自律型ISRと貨物輸送の機会を開くものであり、東南アジアは群島的な地形の中で医療補給のためのドローンに注目しています。

欧州は、厳しい安全文化と持続可能性の要請とのバランスを取りながら、戦略的な足場を維持しています。EASAの段階的なVTOL規制は、ドイツ、フランス、英国の都市計画者にとって、世界的なベンチマークを定義し、信頼性を支えるものであり、それぞれボロコプターとバーティカル・エアロスペース社のeVTOLプロトタイプを受け入れています。地域ファンドは、水素推進とリサイクル可能な構造を対象としており、欧州のOEMはエコ中心の入札で優位に立つことができます。イタリアの全国的なヴァーティポート・コリドー計画やスウェーデンの自律型スウォーム試験は、欧州大陸の民間と軍事の二重の推進力を反映しています。同大陸の成長はAPACより遅いが、その政策的影響力と炭素目標は、同大陸を重要な参考市場として位置づけています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- AIによる飛行制御システムの進歩

- アーバンエアモビリティ(UAM)とeVTOLの急速な普及

- 自律型貨物ドローンによる物流のコスト削減インセンティブ

- ISRと戦闘オートメーションへの軍事投資の増加

- BVLOSエアコリドーと無人交通管理(UTM)の展開

- 飛行認証を受けた自律型アビオニクスとセンサー・スイートの利用可能性の増加

- 市場抑制要因

- 認証と空域統合における規制の複雑さ

- 電池技術の限界と高い資本コスト

- サイバー脅威やシステム乗っ取りに対する脆弱性の高まり

- AI処理装置に影響を及ぼす半導体供給の混乱

- バリューチェーン分析

- テクノロジーの展望

- 規制情勢

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力/消費者

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 航空機タイプ別

- 固定翼

- 回転翼

- ハイブリッド(固定翼VTOL)

- オートノミーレベル別

- 自律化が進む

- 完全自律型

- 用途別

- 貨物航空機

- 旅客機

- 特殊任務/ISR

- エアタクシー/UAM

- 推進タイプ別

- 従来型タービン

- 電気

- ハイブリッド・エレクトリック

- 水素燃料電池

- コンポーネント別

- フライトコントロールコンピューター

- センサーとナビゲーション

- 通信とデータリンク

- ソフトウェアとAIアルゴリズム

- 推進システム

- 機体と構造

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- フランス

- ドイツ

- イタリア

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- その他アジア太平洋地域

- 南米

- ブラジル

- その他南米

- 中東・アフリカ

- 中東

- アラブ首長国連邦

- サウジアラビア

- その他中東

- アフリカ

- 南アフリカ

- その他アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Northrop Grumman Corporation

- The Boeing Company

- Lockheed Martin Corporation

- RTX Corporation

- Elbit Systems Ltd.

- AeroVironment, Inc.

- Saab AB

- BAE Systems plc

- Airbus SE

- Textron Inc.

- Israel Aerospace Industries Ltd.

- General Atomics

- Joby Aviation, Inc.

- Volocopter Technologies GmbH

- Guangzhou EHang Intelligent Technology Co. Ltd.

- Archer Aviation Inc.

- Wisk Aero LLC

- Kratos Defense & Security Solutions Inc.

- Kaman Corporation