|

市場調査レポート

商品コード

1692460

アジア太平洋の電動二輪車市場:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Asia Pacific Electric Two-Wheeler - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋の電動二輪車市場:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

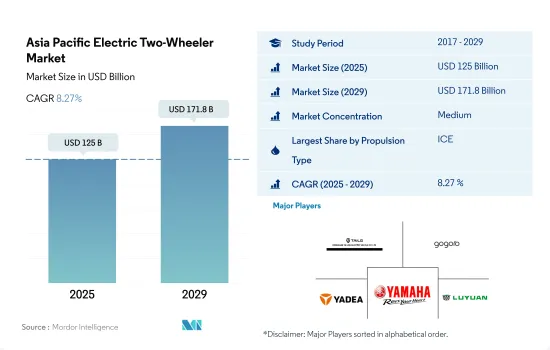

アジア太平洋の電動二輪車市場規模は2025年に1,250億米ドルと推定され、2029年には1,718億米ドルに達すると予測され、予測期間(2025年~2029年)のCAGRは8.27%で成長すると予測されます。

アジア太平洋の二輪車市場は、環境問題、政府支援、技術進歩に後押しされ、電動モビリティへと大きくシフトしています。

- アジア太平洋の環境意識の高まり、補助金や優遇措置といった政府の支援政策、電気自動車の手頃な価格と性能の向上により、電気二輪車はアジア太平洋全域で急速に普及しています。中国は、公害防止と包括的なEVエコシステムの確立を目的とした政府の早期介入により、世界最大のE2W市場を誇り、この牽引役となっています。インドもまた重要な市場として台頭してきており、FAMEインドや州レベルのインセンティブといった政策イニシアチブによって、電気モビリティ導入の野心的な目標に拍車がかかっています。

- これらの国々でのE2Wの人気は、ICE車と比べて環境面でメリットがあり、運用コストが低いことに起因しています。しかし、特に電気インフラがまだ開発途上であったり、E2Wに対する政府のインセンティブがあまり顕著でないアジア太平洋諸国では、ICE二輪車が引き続き市場を独占しています。ベトナム、インドネシア、フィリピンなどの国々では、二輪車の大半がガソリンを燃料としており、その主な理由は、ガソリンが手ごろな価格で入手可能であること、メンテナンスや給油のためのネットワークが確立していることです。

- アジア太平洋における二輪車市場の将来は、バッテリーや充電インフラの技術的進歩、二酸化炭素排出量削減を目指す政府の政策、モビリティや環境持続可能性に対する消費者の意識など、いくつかの要因によって形作られる可能性が高いです。ICE二輪車は当面、特に新興経済圏で引き続き重要な位置を占めると予想されるが、電動モビリティへのシフトは否定できず、アジア太平洋の市場力学を今後も形成し続けると思われます。

アジア太平洋の電動二輪車市場動向

アジア太平洋の急速な電気自動車需要と販売増は、政府のイニシアティブと商用車の電動化が原動力

- アジア太平洋では近年、電気自動車(EV)の需要と販売が急増しています。主要市場である中国は、2022年の電気自動車販売台数が2021年比で2.90%増加し、日本は同期間に11.11%増加しました。この動向を後押ししている要因には、環境問題への関心の高まり、厳しい規制、燃費の良さ、維持費の安さ、二酸化炭素排出ゼロといったEVの利点などがあります。政府の補助金は、アジア諸国におけるEVの採用をさらに後押ししています。

- トラックやバスを代表とする従来型の燃料を使用する商用車は、アジア太平洋諸国の汚染レベル上昇の一因となっています。これに対し、この地域の多くの国々は、二酸化炭素排出量の抑制を目指し、内燃機関(ICE)車を電気自動車に移行させるために多額の投資を行っています。例えば、2020年12月、インドネシアで市営バスを運行するトランスジャカルタは、2030年までに電気バス(Eバス)車両を1万台に拡大するという野心的な計画を発表しました。このような地域全体の取り組みが、商用車の電動化を推進しています。

- アジア太平洋各国の政府機関は、化石燃料自動車を段階的に廃止する措置を積極的に提案しており、この動きは電気商用車市場を強化する構えです。注目すべき開発では、2022年5月、タタ・モーターズがインドで、FAME 2スキームの下で5,450台、5,000カロールインドルピー相当の電気バスを供給する政府契約を獲得しました。さらに同社は、大手eコマース企業6社に小型電気トラック2万台を納入する計画を発表しました。EV分野におけるこうした進歩は、2024年から2030年にかけて、アジア太平洋における電気商用車の需要をさらに促進すると予想されます。

アジア太平洋の電動二輪車産業の概要

アジア太平洋の電動二輪車市場は適度に統合されており、上位5社で50.90%を占めています。この市場の主要企業は以下の通り。 Dongguan Tailing Electric Vehicle, Gogoro Limited, Yadea Group Holdings Ltd., Yamaha Motor Company Limited and Zhejiang Luyuan Electric Vehicle(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 人口

- 一人当たりGDP

- 自動車購入のための消費者支出(cvp)

- インフレ率

- 自動車ローン金利

- 電化の影響

- EV充電ステーション

- バッテリーパック価格

- Xev新モデル発表

- 燃料価格

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 推進タイプ

- ハイブリッド車・電気自動車

- 国名

- 中国

- インド

- 日本

- 韓国

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Ampere Vehicles Private Limited

- Ather Energy Pvt. Ltd.

- Bajaj Auto Ltd.

- Dongguan Tailing Electric Vehicle Co. Ltd.

- Gogoro Limited

- Hero Electric Vehicles Pvt. Ltd.

- NIU Technologies

- Okinawa Autotech Pvt. Ltd.

- Ola Electric Mobility Pvt. Ltd.

- REVOLT Intellicorp Pvt. Ltd.

- TVS Motor Company Limited

- Yadea Group Holdings Ltd.

- Yamaha Motor Company Limited

- Zhejiang Luyuan Electric Vehicle

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The Asia Pacific Electric Two-Wheeler Market size is estimated at 125 billion USD in 2025, and is expected to reach 171.8 billion USD by 2029, growing at a CAGR of 8.27% during the forecast period (2025-2029).

The two-wheeler market in Asia-Pacific is experiencing a significant shift toward electric mobility, fueled by environmental concerns, government support, and technological advancements

- Electric two-wheelers are gaining rapid traction across Asia-Pacific, driven by the region's escalating environmental awareness, supportive government policies in the form of subsidies and incentives, and the increasing affordability and performance of electric vehicles. China leads this charge, boasting the world's largest E2W market due to early government interventions aimed at pollution control and the establishment of a comprehensive EV ecosystem. India is emerging as another significant market, with ambitious targets for electric mobility adoption spurred by policy initiatives like FAME India and state-level incentives.

- The popularity of E2Ws in these countries is attributed to their environmental benefits and lower operational costs compared to ICE vehicles. However, ICE two-wheelers continue to dominate the market in several Asia-Pacific countries, especially where electric infrastructure is still developing or where government incentives for E2Ws are less pronounced. In countries like Vietnam, Indonesia, and the Philippines, the vast majority of two-wheelers run on gasoline, primarily due to their affordability, wide availability, and a well-established network for maintenance and fueling.

- The future of the two-wheeler market in Asia-Pacific is likely to be shaped by several factors, including technological advancements in battery and charging infrastructure, government policies aimed at reducing carbon emissions, and consumer attitudes toward mobility and environmental sustainability. While ICE two-wheelers are expected to remain relevant in the near term, especially in emerging economies, the shift toward electric mobility is undeniable and will continue to reshape the market dynamics in Asia-Pacific.

Asia Pacific Electric Two-Wheeler Market Trends

APAC's rapid electric vehicle demand and sales growth are driven by government initiatives and commercial vehicle electrification

- Electric vehicle (EV) demand and sales have surged in the APAC region in recent years. China, the dominant market, saw a 2.90% rise in electric car sales in 2022 compared to 2021, while Japan experienced an 11.11% increase during the same period. Factors driving this trend include mounting environmental concerns, stringent regulations, and the advantages of EVs, such as fuel efficiency, lower maintenance costs, and zero carbon emissions. Government subsidies further bolster the adoption of EVs in Asian nations.

- Conventional fuel-powered commercial vehicles, notably trucks and buses, are contributing to the escalating pollution levels in several Asia-Pacific countries. In response, many nations in the region are making substantial investments to transition their internal combustion engine (ICE) vehicles to electric ones, aiming to curb carbon emissions. For instance, in December 2020, TransJakarta, a city-owned bus operator in Indonesia, unveiled an ambitious plan to expand its electric bus (e-bus) fleet to 10,000 units by 2030. Such initiatives across the region are propelling the electrification of commercial vehicles.

- Government bodies in various APAC countries are actively proposing measures to phase out fossil fuel vehicles, a move that is poised to bolster the market for electric commercial vehicles. In a notable development, in May 2022, Tata Motors secured a government contract in India to supply 5,450 electric buses worth INR 5,000 crore under the FAME 2 scheme. Additionally, the company announced plans to deliver 20,000 light electric trucks to six major e-commerce players. These advancements in the EV space are anticipated to further fuel the demand for electric commercial vehicles in the APAC region from 2024 to 2030.

Asia Pacific Electric Two-Wheeler Industry Overview

The Asia Pacific Electric Two-Wheeler Market is moderately consolidated, with the top five companies occupying 50.90%. The major players in this market are Dongguan Tailing Electric Vehicle Co. Ltd., Gogoro Limited, Yadea Group Holdings Ltd., Yamaha Motor Company Limited and Zhejiang Luyuan Electric Vehicle (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Population

- 4.2 GDP Per Capita

- 4.3 Consumer Spending For Vehicle Purchase (cvp)

- 4.4 Inflation

- 4.5 Interest Rate For Auto Loans

- 4.6 Impact Of Electrification

- 4.7 EV Charging Station

- 4.8 Battery Pack Price

- 4.9 New Xev Models Announced

- 4.10 Fuel Price

- 4.11 Regulatory Framework

- 4.12 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Propulsion Type

- 5.1.1 Hybrid and Electric Vehicles

- 5.2 Country

- 5.2.1 China

- 5.2.2 India

- 5.2.3 Japan

- 5.2.4 South Korea

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Ampere Vehicles Private Limited

- 6.4.2 Ather Energy Pvt. Ltd.

- 6.4.3 Bajaj Auto Ltd.

- 6.4.4 Dongguan Tailing Electric Vehicle Co. Ltd.

- 6.4.5 Gogoro Limited

- 6.4.6 Hero Electric Vehicles Pvt. Ltd.

- 6.4.7 NIU Technologies

- 6.4.8 Okinawa Autotech Pvt. Ltd.

- 6.4.9 Ola Electric Mobility Pvt. Ltd.

- 6.4.10 REVOLT Intellicorp Pvt. Ltd.

- 6.4.11 TVS Motor Company Limited

- 6.4.12 Yadea Group Holdings Ltd.

- 6.4.13 Yamaha Motor Company Limited

- 6.4.14 Zhejiang Luyuan Electric Vehicle

7 KEY STRATEGIC QUESTIONS FOR VEHICLES CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms